Key Takeaways

Sable Offshore (SOC) surged after the company priced a large common stock and convertible senior notes offering.

The move was not driven by a clean earnings beat. It was more likely a high-volatility rebound after financing terms became clearer.

The company is trying to refinance debt tied to Exxon Mobil while restarting production from the Santa Ynez Unit and Santa Ynez Pipeline System.

The bullish case is based on oil production restart, potential cash flow from Santa Ynez, and refinancing progress.

The risk case is significant: large dilution, convertible debt, high leverage, legal challenges, environmental scrutiny, and execution risk remain central to the story.

Why SOC Moved Sharply Higher

Sable Offshore Corp. (NYSE: SOC) is an offshore energy company focused on the Santa Ynez Unit and related pipeline infrastructure in California.

The latest rally was not a traditional earnings-driven move. Instead, it was a financing-driven rebound.

Sable announced the pricing of a major financing package, including the issuance of 32,467,533 shares of common stock at $3.08 per share and $300 million of 6.5% convertible senior notes due 2031.

The convertible notes carry an initial conversion price of approximately $4.00 per share.

The company plans to use the proceeds, together with a new senior secured term loan facility, to repay existing senior secured debt owed to Exxon Mobil.

That is the key reason the stock bounced.

Before the announcement, investors were concerned about refinancing risk, debt pressure, and funding needs. Once the financing terms became clear, the market appeared to treat the event as a partial resolution of near-term liquidity uncertainty.

However, this does not mean the financing is purely positive.

The common stock offering creates major dilution. The convertible notes create future dilution risk if the stock trades above the conversion price. The refinancing may help the company move forward, but it comes at a high cost to existing shareholders.

Therefore, SOC’s rally should be viewed as a high-risk financing relief rally rather than a clean fundamental breakout.

The Core Catalyst: Financing Terms Became Clear

The most important near-term catalyst was the pricing of the financing package.

Sable’s stock had already been under heavy pressure because investors were worried about how the company would handle its debt obligations and restart-related capital needs.

The financing update gave the market more clarity.

The common stock offering price was set at $3.08.

The convertible notes were set at $300 million.

The interest rate was 6.5%.

The maturity was set for 2031.

The initial conversion price was approximately $4.00.

For traders, that $4.00 conversion level became an important reference point.

When SOC moved above $4, the market began to price in the possibility that the company had enough financing visibility to keep pushing forward with the Santa Ynez restart.

Still, clarity does not eliminate risk.

This financing package helps address near-term debt refinancing, but it also confirms that Sable needed significant external capital. That is why the stock’s move is both understandable and risky.

News Sentiment and Information Quality

The information quality behind the rally is high because the financing terms came from an official company announcement.

However, the news sentiment is mixed.

On the positive side, Sable now has a clearer path to refinance existing Exxon-related debt. That reduces one immediate uncertainty.

On the negative side, the financing package is highly dilutive.

Issuing more than 32 million new shares at $3.08 is a major event for existing shareholders. The $300 million convertible note offering adds another layer of future dilution risk.

That means the rally is not based on the idea that the company suddenly became less risky.

It is based on the idea that one major uncertainty became more defined.

This is an important distinction.

Investors should not confuse “funding terms are known” with “the balance sheet is fixed.”

The company still needs to close the refinancing package, stabilize production, manage legal risk, and generate enough cash flow to support its capital structure.

Price Action and Volume Analysis

SOC traded around $4.40 after surging more than 40% in a single session.

That is a very strong short-term move.

However, the price action needs context. This was a rebound after major financing-related pressure, not a simple continuation of a healthy uptrend.

The $4.00 level is especially important because it is close to the initial conversion price of the convertible notes.

If the stock holds above $4, traders may continue to price in financing relief and production restart upside.

If the stock falls back below $4, the market may begin to focus again on dilution, refinancing risk, and legal uncertainty.

The $3.08 offering price is another key level.

If SOC trades back toward the offering price, it may suggest that the financing-driven rebound is losing strength.

On the upside, a move above $5 would suggest that the market is assigning more value to the Santa Ynez restart and refinancing plan.

For now, the move looks powerful but fragile.

Technical Analysis: Strong Rebound, Weak Confirmation

Technically, SOC is in a sharp rebound phase.

A one-day move of more than 40% shows strong short-term demand. It may also reflect short covering after a steep decline.

However, this is not yet a confirmed trend reversal.

The stock remains highly sensitive to financing terms, debt refinancing, production updates, regulatory developments, and court decisions.

Traditional technical indicators are less useful in this type of setup.

The more important levels are event-driven:

$4.00 as the convertible conversion-price reference zone.

$3.08 as the common stock offering price.

$5.00 as a potential recovery threshold if investors begin assigning more value to the Santa Ynez production restart.

If SOC holds above $4 and pushes toward $5, momentum may continue.

If it fails to hold $4, the rally could quickly turn into another high-volatility pullback.

Sector Context: Not a Normal Energy Rally

SOC should not be analyzed like a typical oil and gas stock.

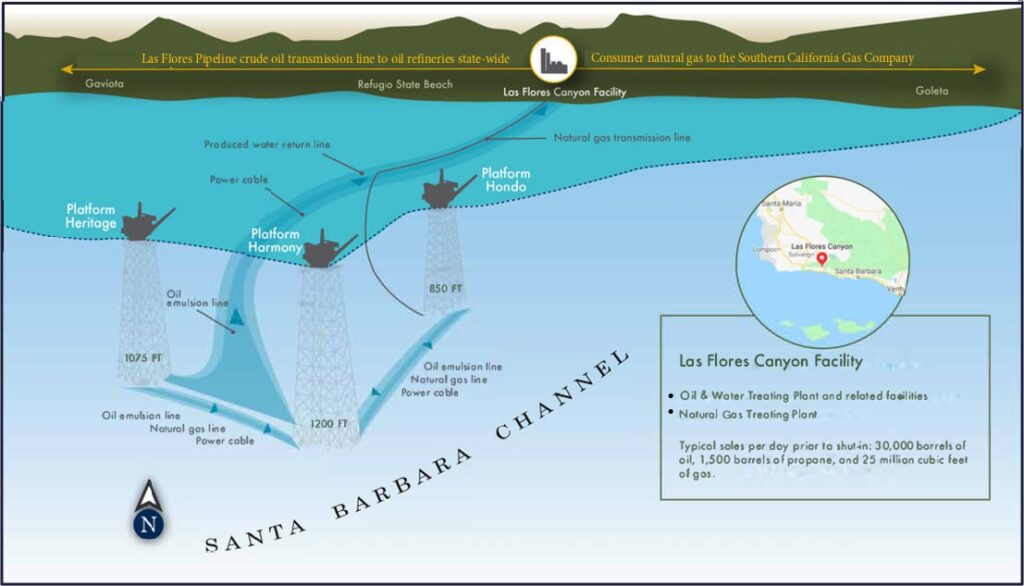

The company is tied to a very specific asset and legal situation: the Santa Ynez Unit and Santa Ynez Pipeline System in California.

Sable has restarted oil sales through the Santa Ynez Pipeline System. The company has also highlighted production from Platform Harmony and restart plans for additional platforms.

That gives the company a potentially meaningful production story.

However, this is not a simple oil-price beta trade.

SOC is exposed to:

California regulatory risk.

Environmental litigation.

Pipeline restart disputes.

Federal and state legal conflict.

Large debt obligations.

Refinancing execution.

Production restart reliability.

Capital expenditure needs.

That makes SOC a special-situation energy stock.

Oil prices matter, but they are not the only driver.

The stock will likely respond more to financing updates, court decisions, pipeline operations, and Santa Ynez production data than to ordinary energy-sector moves.

Fundamental Analysis: Production Potential, Heavy Financial Burden

Sable’s fundamental profile is highly unusual.

On one side, the company owns assets that could produce meaningful oil volumes if operations stabilize.

The Santa Ynez Unit restart is a real operating catalyst. Platform Harmony production and planned restarts at other platforms support the bullish case.

On the other side, the company’s financial position is very strained.

Sable reported a Q1 2026 net loss of $197.0 million.

The company ended the quarter with short-term outstanding debt of $956.3 million, including paid-in-kind interest.

Cash and cash equivalents were only $52.2 million at quarter-end.

That explains why the company needed a large financing package.

The fundamental question is not whether Sable has oil assets. It does.

The question is whether the company can turn those assets into consistent cash flow before dilution, interest expense, capex, and legal risks overwhelm the equity value.

That question remains unresolved.

Operating Efficiency: Too Early to Confirm

From an operating efficiency perspective, SOC is still in a transition phase.

The company has restarted oil sales, and production from the Santa Ynez Unit is a positive step.

However, reliable production and profitable production are not the same thing.

For operating efficiency to improve, Sable needs several things to happen at the same time:

Production must remain stable.

Pipeline transportation must continue without interruption.

Legal challenges must not stop operations.

Capital spending must stay within plan.

Debt refinancing must close.

Interest expense must become manageable.

Oil sales must translate into free cash flow.

At this point, investors do not yet have enough evidence to say that the company has reached stable operating efficiency.

SOC is still a restart-and-refinancing story.

The potential upside is large, but execution risk is also large.

Financial Risk, Dilution, and Legal Risk

Financial risk is the center of the SOC investment case.

The company’s refinancing package may help solve near-term debt pressure, but it also creates major dilution.

The common stock offering adds more than 32 million shares.

The convertible notes add future dilution risk.

The new senior secured financing structure adds continued debt and interest burden.

For existing shareholders, this is a difficult trade-off.

Without financing, the company faces liquidity and refinancing risk.

With financing, the company faces dilution and leverage risk.

Legal and regulatory risk adds another layer.

A U.S. District Court denied a California Department of Parks and Recreation request to block Sable from transporting oil via the pipeline, which was positive for the company. But California-related legal and regulatory challenges remain important.

The Santa Ynez pipeline system has a controversial history after the 2015 oil spill, and any future operational or environmental dispute could affect the stock.

SOC is therefore not just an oil production story.

It is a combined financing, legal, regulatory, environmental, and operational risk story.

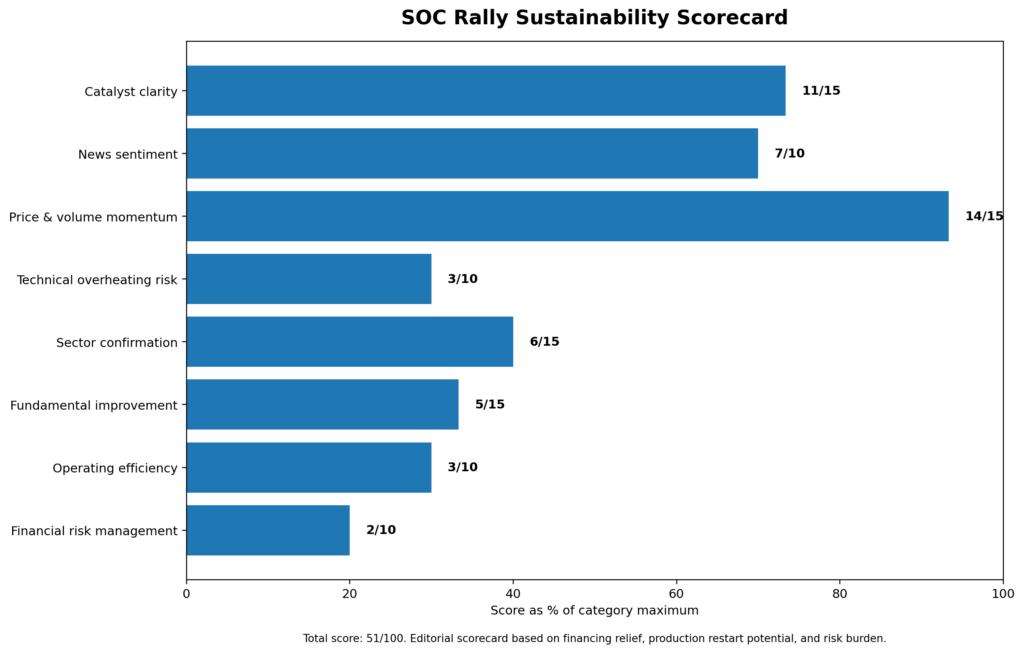

SOC Rally Sustainability Score

Overall Score: 51/100

Rating: Strong short-term rebound, but still a high-risk special situation

Catalyst Clarity: 11/15

The financing terms, $3.08 stock offering, $300 million convertible note deal, and approximately $4.00 initial conversion price provide clear catalysts. However, this is not a clean earnings catalyst.

News Sentiment and Reliability: 7/10

The information comes from official company announcements, but the content itself is mixed because it includes major dilution and refinancing risk.

Price and Volume Momentum: 14/15

A rally of more than 40% shows strong short-term demand and possible short-covering momentum.

Technical Overheating Risk: 3/10

The move is extremely volatile and follows a sharp decline. A break below $4 could quickly weaken the setup.

Sector Confirmation: 6/15

SOC is tied less to the broad energy sector and more to company-specific financing, legal, and Santa Ynez restart events.

Fundamental Improvement: 5/15

Production restart is positive, but Q1 losses, debt, capex needs, and legal risks remain significant.

Operating Efficiency: 3/10

The company has production assets, but stable cash-flow conversion has not yet been proven.

Financial Risk Management: 2/10

The refinancing package may help, but dilution, convertible debt, high leverage, and legal uncertainty remain major risks.

What Investors Should Watch Next

The first factor is whether SOC can hold above $4.00. This level matters because it is close to the initial conversion price of the convertible notes.

The second factor is whether SOC avoids falling back toward the $3.08 common stock offering price. A move back toward that level would suggest that the financing rebound is weakening.

The third factor is whether the refinancing package closes successfully. The equity offering, convertible notes, and new senior secured financing are connected to the company’s broader debt repayment plan.

The fourth factor is whether Sable completes repayment of the Exxon-related senior secured debt.

The fifth factor is whether Santa Ynez production remains stable. Investors should watch updates from Platform Harmony, Platform Heritage, Platform Hondo, and pipeline throughput.

The sixth factor is legal and regulatory progress in California. A favorable court ruling helped, but legal challenges remain a key overhang.

The seventh factor is capex and cash flow. Restarting production requires capital, and investors need to see whether oil sales can generate cash after operating costs, capex, and interest expense.

Bottom Line

Sable Offshore’s latest rally is best understood as a financing-relief rebound, not a clean fundamental breakout.

The company has a real production story through the Santa Ynez Unit and Santa Ynez Pipeline System. Oil sales have resumed, and the production restart gives SOC meaningful upside if operations stabilize.

However, the balance sheet remains highly risky.

The company reported a large Q1 net loss, significant short-term debt, limited cash, and major capital requirements. The newly priced financing package may help repay Exxon-related debt, but it also introduces major dilution and future convertible-note overhang.

Legal and regulatory risk remains another major uncertainty.

SOC is therefore not a typical energy stock and not a simple turnaround.

It is a high-risk special situation where the upside depends on several things going right at the same time: refinancing closing, Santa Ynez production stability, legal risk reduction, capex control, and cash flow generation.

For now, SOC has strong short-term momentum, but the rally remains fragile. Investors should watch the $4 level, the $3.08 offering price, refinancing completion, Santa Ynez production updates, and California legal developments before assuming a durable turnaround.

Related Reading

- https://sableoffshore.com/overview/default.aspx

- https://finance.yahoo.com/quote/SOC/

- https://mgiedit.org/dlo-stock-surge-dlocal-emerging-market-payments-growth/

- https://mgiedit.org/avav-stock-surge-aerovironment-bluehalo-defense-drone/

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, or a recommendation to buy or sell any security. Investors should conduct their own research and consider their risk tolerance before making investment decisions.