Key Takeaways

AeroVironment (AVAV) surged after the company reported a major FY2026 fourth-quarter earnings beat, strong revenue growth, expanded backlog, and meaningful contribution from the BlueHalo acquisition.

The rally was supported by a 133% year-over-year increase in quarterly revenue, stronger-than-expected non-GAAP EPS, and funded backlog of approximately $1.2 billion.

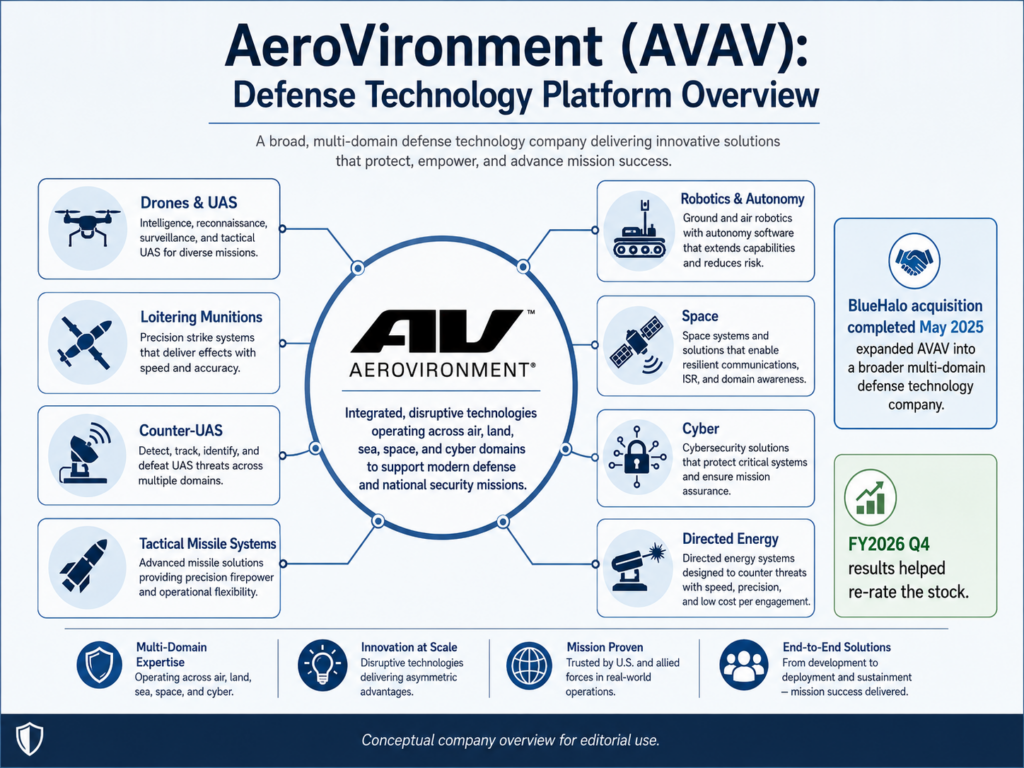

The BlueHalo acquisition has transformed AeroVironment from a primarily unmanned systems company into a broader defense technology platform across air, land, sea, space, cyber, counter-UAS, and directed energy.

However, the stock pulled back sharply from its intraday high, suggesting that investors are also weighing FY2027 guidance, acquisition integration risk, government budget timing, and near-term profit-taking.

The key question is whether AVAV’s strong quarter marks the start of a durable defense technology revaluation or whether the post-earnings rally has already priced in too much optimism.

Why AVAV Moved Sharply Higher

AeroVironment, Inc. (NASDAQ: AVAV) is a defense technology company known for unmanned aircraft systems, loitering munitions, tactical missile systems, robotic systems, and advanced defense solutions.

The stock surged after the company reported strong fiscal 2026 fourth-quarter results.

Quarterly revenue rose to $641.6 million, compared with $275.1 million in the prior-year period. That represented 133% year-over-year growth.

Full-year revenue reached approximately $2.0 billion, marking a major scale-up for the company.

Profitability also came in stronger than expected. Fourth-quarter net income was $63.2 million, diluted EPS was $1.25, and non-GAAP EPS was $1.84, above the reported analyst expectation of $1.46.

The second major driver was the BlueHalo acquisition.

AeroVironment completed the acquisition of BlueHalo in May 2025. The deal expanded the company’s capabilities beyond drones and unmanned systems into counter-UAS, space technologies, cyber, directed energy, electronic warfare, and broader defense technology solutions.

That is why the market reaction was so strong.

Investors are not only reacting to a strong quarter. They are reassessing AVAV as a larger defense technology platform with more revenue scale, more backlog, and a broader set of mission-critical defense capabilities.

BlueHalo: Why the Acquisition Matters

The BlueHalo acquisition is central to the AVAV revaluation story.

Before the transaction, AeroVironment was best known for unmanned aircraft systems, Switchblade loitering munitions, and tactical defense systems.

After the BlueHalo acquisition, the company now has exposure to a much wider defense technology stack.

This includes:

Counter-unmanned aircraft systems.

Directed energy.

Space communications.

Cyber capabilities.

Electronic warfare.

Autonomous systems.

Advanced sensing and mission technologies.

That matters because defense demand is shifting.

Modern military and security priorities increasingly involve drones, drone defense, autonomous systems, electronic warfare, battlefield sensing, space-based systems, and integrated command-and-control technologies.

BlueHalo gives AeroVironment a larger role in that transition.

However, investors should separate acquisition-driven revenue growth from organic growth.

BlueHalo and Empirical Systems Aerospace contributed approximately $282.3 million of fourth-quarter revenue. That means the quarter’s explosive growth was not only from legacy AeroVironment demand. It also reflected the impact of acquired businesses.

This is not necessarily negative. Acquisitions can create real value.

But the next phase depends on integration.

The market will need to see whether BlueHalo improves margins, backlog, cross-selling opportunities, and long-term earnings power after the initial revenue boost.

News Sentiment and Information Quality

News sentiment around AVAV is strongly positive.

The key market phrases are drone defense, loitering munitions, counter-UAS, BlueHalo, directed energy, space, cyber, backlog growth, defense demand, and earnings beat.

These are powerful themes in the current defense technology market.

The information quality is also high because the rally was driven by company-reported earnings, revenue, adjusted EBITDA, backlog, and guidance data.

Fourth-quarter non-GAAP adjusted EBITDA was $140.1 million. Funded backlog increased to approximately $1.2 billion, compared with $726.6 million in the prior-year period.

Those are concrete operating figures, not rumor-based catalysts.

However, the market reaction was not purely positive.

The stock traded as high as $190.88 intraday but later pulled back toward the $160 area. That suggests investors were also reacting to concerns around FY2027 guidance, integration risk, and the size of the initial move.

The company’s FY2027 revenue guidance of $2.13 billion to $2.23 billion points to continued scale, but the adjusted EPS guidance range of $3.02 to $3.34 was reportedly below market expectations.

That likely limited the post-earnings upside.

Price Action and Volume Analysis

AVAV showed very strong but volatile price action.

The stock recently traded around $160.16, up approximately 15.2% on the day. However, the intraday range was wide, from $157.89 to $190.88.

That is an important detail.

The initial reaction to the earnings report was extremely strong, but the stock gave back a significant portion of its intraday gains.

Volume was also elevated at approximately 4.66 million shares, showing that market attention increased sharply.

This type of price action suggests two forces were working at the same time.

First, the earnings report triggered real buying interest.

Second, the large intraday spike attracted profit-taking.

For short-term investors, the $160 area is now important. If AVAV can hold near this level, the market may continue to support the earnings-based revaluation.

The $175 to $190 range is the next major resistance zone. A move back into that area with strong volume would suggest that buyers are willing to look past guidance concerns and focus on the long-term defense technology story.

If the stock fails to hold $160, the rally could shift into a post-earnings digestion phase.

Technical Analysis: Strong Event Rally, but Not a Clean Breakout Yet

Technically, AVAV is in an event-driven breakout attempt.

The earnings reaction was strong, and the volume response confirms that investors paid attention. However, the sharp rejection from the $190.88 intraday high makes the chart more complicated.

This does not look like a simple straight-line breakout.

Instead, it looks like a stock undergoing rapid price discovery after a major earnings report.

The $160 area is the first support level to watch.

If AVAV holds this zone, the earnings beat and backlog expansion may support a new base.

If the stock falls below $160, traders may interpret the intraday rejection as a sign that the rally moved too far too quickly.

The $175 to $190 area is the key resistance zone.

A recovery into that range would indicate renewed confidence. A failure to reclaim it could suggest that investors want more evidence before assigning a higher valuation.

Because the move is tied to earnings and acquisition-driven scale, technical analysis should be combined with fundamental confirmation.

Sector Context: Defense Drones, Counter-UAS, and Modern Warfare

AVAV operates in one of the most important areas of the defense market: unmanned systems and drone warfare.

Demand for drones, loitering munitions, counter-UAS systems, robotic platforms, and battlefield autonomy has increased as military strategy shifts toward lower-cost, distributed, and autonomous defense capabilities.

AeroVironment is directly exposed to this trend.

The company’s products and technologies are tied to U.S. military customers, international defense customers, government agencies, and allied defense programs.

The BlueHalo acquisition broadens that exposure even further.

AVAV is no longer only a drone company. It is increasingly a multi-domain defense technology company.

That includes air, land, sea, space, cyber, autonomy, directed energy, and counter-drone capabilities.

This sector positioning is one reason investors responded strongly to the earnings report.

However, defense stocks are not risk-free.

They depend on government budgets, procurement timing, contract awards, geopolitical demand, and program execution.

A strong backlog is helpful, but future growth still depends on converting demand into funded contracts and revenue.

Fundamental Analysis: Strong Quarter, but Acquisition Effects Matter

AVAV’s latest quarter showed major fundamental improvement.

Fourth-quarter revenue was $641.6 million, up 133% from the prior-year period. Full-year revenue reached approximately $2.0 billion.

Gross margin also improved in dollar terms. Fourth-quarter gross margin was $202.6 million, compared with $100.3 million in the prior-year period, representing 102% growth.

Non-GAAP adjusted EBITDA was $140.1 million, showing that the company produced strong operating profitability on an adjusted basis.

Funded backlog increased to approximately $1.2 billion, up from $726.6 million a year earlier.

These numbers support the bullish argument.

AeroVironment is not moving only because of a vague drone theme. The company reported real revenue growth, real earnings strength, and real backlog expansion.

However, investors should be careful with the composition of growth.

BlueHalo and Empirical Systems Aerospace contributed $282.3 million of fourth-quarter revenue. That means acquisitions played a major role in the headline growth rate.

The company also recorded acquisition-related intangible amortization and non-cash purchase accounting expenses that affected GAAP results.

Therefore, investors should analyze both GAAP and non-GAAP figures.

The fundamental picture is positive, but the next step is to prove that acquired revenue can translate into durable earnings, cash flow, and margin improvement.

Operating Efficiency: Improving, but Integration Risk Remains

From an operating efficiency perspective, AeroVironment improved meaningfully.

Revenue more than doubled.

Gross margin increased.

Adjusted EBITDA expanded.

Backlog improved.

Those are all positive signals.

However, the operating story is not simple because acquisitions changed the company’s structure.

BlueHalo significantly expanded AeroVironment’s scale and technology portfolio, but it also introduced integration complexity. The company now needs to manage a broader defense technology platform, more employees, more cost centers, new accounting effects, and broader program execution responsibilities.

Acquisition-related costs, intangible amortization, purchase accounting expenses, and goodwill impairment risk can all affect reported results.

That is why investors should not look only at adjusted EBITDA.

Adjusted numbers are useful, but GAAP results still matter.

The most important operating question is whether AeroVironment can turn the BlueHalo acquisition into sustainable operating leverage.

The market wants to see:

Cross-selling opportunities.

Margin stability.

Cost discipline.

Backlog conversion.

Strong bookings.

Lower integration noise.

If those trends improve, the revaluation becomes more durable.

Financial Risk and Guidance Risk

AVAV’s risk profile is different from speculative small-cap technology stocks.

The company has real revenue, real defense customers, real backlog, and a stronger strategic position after BlueHalo.

The main risks are not survival risk. They are expectation risk, integration risk, government budget risk, and guidance risk.

The first issue is FY2027 guidance.

While revenue guidance of $2.13 billion to $2.23 billion suggests continued scale, the adjusted EPS outlook of $3.02 to $3.34 was reportedly below analyst expectations.

That matters because a stock can beat earnings and still pull back from its high if forward guidance disappoints.

The second issue is government budget timing.

Defense contractors can face delays in budget approvals, contract awards, procurement schedules, and international order timing.

The third issue is BlueHalo integration.

The acquisition expanded AVAV’s strategic opportunity, but integration costs and accounting effects may create earnings volatility.

The fourth issue is valuation.

After a strong earnings-driven rally, investors will expect continued execution. If backlog growth slows, margin pressure increases, or guidance does not improve, the stock could remain volatile.

AVAV Rally Sustainability Score

Overall Score: 78/100

Rating: Strong earnings-backed defense technology story, but better after confirmation or pullback

Catalyst Clarity: 15/15

The catalyst is very clear: FY2026 fourth-quarter revenue growth, EPS beat, adjusted EBITDA strength, funded backlog expansion, and BlueHalo integration.

News Sentiment and Reliability: 9/10

The rally was driven by official company earnings data and specific financial metrics. Information quality is high.

Price and Volume Momentum: 14/15

The stock rose sharply with elevated volume, but the large pullback from the intraday high reduces the score slightly.

Technical Overheating Risk: 4/10

The intraday move to $190.88 followed by a pullback toward the $160 area suggests significant chase risk.

Sector Confirmation: 13/15

Defense drones, loitering munitions, counter-UAS, military robotics, directed energy, cyber defense, and space defense themes all support the broader story.

Fundamental Improvement: 11/15

Revenue, adjusted EBITDA, gross margin, and backlog improved meaningfully. However, acquisition effects and GAAP costs must be separated.

Operating Efficiency: 7/10

Adjusted performance improved, but integration costs, amortization, purchase accounting, and broader operating complexity remain important.

Financial Risk Management: 5/10

The company is not distressed, but FY2027 guidance, budget timing, acquisition integration, and goodwill impairment risk are relevant.

What Investors Should Watch Next

The first factor is whether AVAV holds the $160 area. This level matters because the stock pulled back sharply from the intraday high.

The second factor is whether AVAV can reclaim the $175 to $190 range. That zone represents the area where profit-taking appeared after the earnings spike.

The third factor is FY2027 guidance. Investors will want to see whether bookings, backlog conversion, and defense demand eventually support guidance upside.

The fourth factor is BlueHalo integration. The acquisition needs to produce more than revenue scale. It must also support margin improvement, cross-selling, and long-term earnings power.

The fifth factor is funded backlog. Backlog increased to approximately $1.2 billion, but investors need to see continued bookings momentum.

The sixth factor is government budget timing. Defense demand is strong, but procurement delays can affect revenue recognition and guidance.

The seventh factor is GAAP profitability. Non-GAAP results were strong, but acquisition-related amortization, purchase accounting, and impairment risks still matter.

Bottom Line

AeroVironment’s latest surge is more than a simple drone-stock rally.

The company delivered a strong FY2026 fourth quarter, with revenue up 133%, stronger-than-expected non-GAAP EPS, expanded adjusted EBITDA, and funded backlog rising to approximately $1.2 billion.

The BlueHalo acquisition also changed the investment story. AeroVironment is now a broader defense technology platform with exposure to drones, loitering munitions, counter-UAS, space, cyber, directed energy, autonomy, and multi-domain defense systems.

That makes AVAV one of the more substantial defense technology growth stories in the market.

However, the stock’s sharp pullback from its intraday high shows that investors are not ignoring the risks.

FY2027 EPS guidance was reportedly below expectations, acquisition integration risk remains, and government budget timing could affect future results.

The best interpretation is that AVAV is a real earnings-backed defense technology revaluation story, not a low-quality momentum spike.

But after a sharp move, investors should watch the $160 support area, the $175 to $190 resistance zone, BlueHalo integration progress, backlog conversion, and potential guidance revisions.

For now, AVAV looks fundamentally stronger than many speculative rally stocks, but the post-earnings move still requires confirmation.

Related Reading

- https://www.avinc.com/

- https://finance.yahoo.com/markets/stocks/articles/avav-stock-skyrockets-track-best-151321131.html

- https://mgiedit.org/ped-stock-surge-earnings-revaluation-or-low-float-energy-momentum/

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, or a recommendation to buy or sell any security. Investors should conduct their own research and consider their risk tolerance before making investment decisions.