Key Takeaways

dLocal (DLO) surged as investors reacted to strong Q1 2026 growth in total payment volume, revenue, and gross profit.

The company reported TPV growth of 73% year over year, revenue growth of 55%, and gross profit growth of 40%, reinforcing its position as a high-growth emerging market payments infrastructure company.

The bullish case is based on cross-border payments, local payment methods, global merchant expansion, stablecoin payment infrastructure, and BNPL growth in emerging markets.

However, DLO is not risk-free. Gross profit margin declined, gross profit over TPV fell, and adjusted free cash flow dropped sharply in Q1.

The key question is whether dLocal can convert rapid TPV growth into durable gross profit, operating leverage, and free cash flow recovery.

Why DLO Moved Higher

dLocal Limited (NASDAQ: DLO) is a cross-border payments infrastructure company focused on emerging markets.

The company helps global merchants accept payments, make payouts, settle funds, and connect with local payment methods across Latin America, Africa, Asia, the Middle East, and other emerging regions.

Its core model is built around “One dLocal,” a single API, single platform, and single contract structure that allows global companies to access multiple local payment networks without building separate country-by-country infrastructure.

That model is valuable because emerging markets are fragmented.

Payment methods, banking systems, currencies, tax rules, regulation, settlement processes, and consumer preferences vary widely by country. dLocal’s platform helps global merchants simplify that complexity.

The latest rally was driven mainly by strong Q1 2026 results.

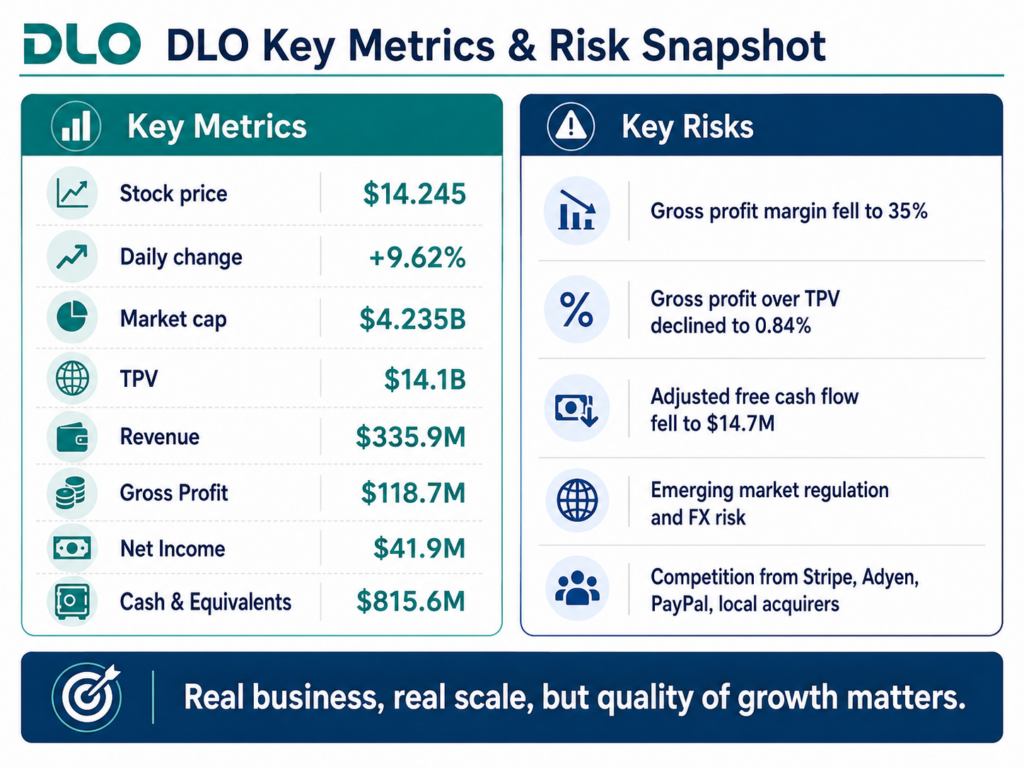

Total payment volume reached $14.1 billion, up 73% year over year. Revenue increased 55% to $335.9 million. Gross profit rose 40% to $118.7 million, reaching a record level.

Those numbers show that dLocal’s emerging market payments network is still scaling quickly.

This is why DLO’s move looks more like a fintech growth-stock revaluation than a low-float speculative spike.

The Core Growth Story: Emerging Market Payments Infrastructure

dLocal’s business sits at the intersection of several powerful themes.

The first is cross-border commerce. Global merchants increasingly want to sell into emerging markets, but payment localization remains difficult.

The second is local payment adoption. Many consumers in emerging markets do not use the same credit card or banking systems common in developed markets. Local payment methods, bank transfers, wallets, cash-linked systems, and alternative payment rails matter.

The third is merchant expansion. dLocal connects large global companies to local buyers and sellers across many countries through one infrastructure layer.

The fourth is fintech product expansion. dLocal is now also positioning around stablecoin payments, BNPL, local acquiring, payout infrastructure, and treasury tools.

This gives DLO a larger story than basic payment processing.

The company is trying to become an operating layer for global merchants entering complex, high-growth emerging markets.

That is why investors responded positively to the Q1 results.

The business is not just growing because of one country or one payment method. It is benefiting from a broader shift toward localized payment infrastructure in emerging economies.

News Sentiment and Information Quality

News sentiment around DLO is positive.

The strongest market keywords are TPV growth, revenue growth, record gross profit, emerging market payments, stablecoins, BNPL, local payment methods, and global merchant expansion.

These are attractive themes for fintech investors.

Information quality is also relatively strong because the main catalyst comes from company-reported Q1 2026 financial results.

However, the news is not purely positive.

The most important negative detail is margin compression.

Gross profit margin declined from 39% in Q1 2025 to 35% in Q1 2026. Gross profit over TPV also fell from 1.05% to 0.84%.

That means dLocal processed much more payment volume, but it earned less gross profit per dollar of TPV.

Management may view this as a natural result of larger merchant mix, new payment methods, and geographic expansion. However, investors still need to monitor the trend carefully.

For payment companies, growth quality matters.

A company can grow TPV very quickly, but if take rates and gross profit per transaction decline too much, valuation can become more difficult to justify.

The current news backdrop is positive, but profitability quality remains the key watch item.

Price Action and Volume Analysis

DLO traded around $14.245, up approximately 9.6% on the day.

The intraday range was $13.26 to $14.46, and volume was approximately 1.21 million shares.

This is a strong move, but it is not the kind of extreme low-float spike seen in some micro-cap stocks.

DLO has a market capitalization above $4 billion, so the move appears more connected to earnings quality, fintech sentiment, and growth-stock reassessment.

The stock closed near its intraday high area, which is constructive for short-term momentum.

The key level to watch is $14.50.

If DLO breaks above $14.50 with volume, momentum could extend as investors price in continued Q2 growth.

If the stock fails near that area, short-term profit-taking may appear.

The $14 area is also important as a support zone. Holding above $14 would suggest that the market is accepting the Q1 growth story.

Technical Analysis: Strong Rebound, but Confirmation Needed

Technically, DLO is in a strong rebound phase.

A near-10% daily gain shows renewed investor interest, especially because the move is supported by strong Q1 financial metrics.

However, this is not yet a fully confirmed long-term breakout.

The next technical test is whether DLO can hold above $14 and break above the $14.50 area.

If the stock clears $14.50 with strong volume, the market may be signaling that the Q1 growth story deserves a higher valuation range.

If it cannot break that level, the move may remain a short-term fintech rebound.

Because DLO is a growth-oriented fintech stock, technicals should be analyzed together with fundamentals.

The chart may show momentum, but the next real confirmation will come from Q2 results, margin trends, and free cash flow recovery.

Sector Context: Cross-Border Payments, Stablecoins, and BNPL

dLocal belongs to several overlapping fintech themes.

These include emerging market payments, cross-border payments, local acquiring, merchant payments, payout infrastructure, stablecoin payments, BNPL, gaming payments, subscription payments, retail payments, and mobility-related commerce.

The company serves global merchants that need access to fragmented local payment rails.

That makes dLocal different from payment companies that primarily operate in developed markets.

The emerging market opportunity is large, but it is also more complex.

Countries can differ widely in payment behavior, foreign exchange rules, capital controls, tax treatment, licensing requirements, and consumer financing regulation.

dLocal’s advantage is its local connectivity and single-platform model.

The company has also been expanding into newer fintech areas. Stablecoin infrastructure may help merchants accept, convert, settle, or manage treasury operations in emerging markets. BNPL expansion may help merchants offer more flexible financing to buyers in regions where traditional credit access can be limited.

These product extensions strengthen the growth story.

However, competition is intense.

dLocal competes with global payment companies, local acquirers, fintech infrastructure providers, stablecoin-native payment firms, and regional payment processors.

The company’s long-term value depends on whether it can maintain local expertise, merchant relationships, and compliance capabilities while scaling profitably.

Fundamental Analysis: Strong Growth, Margin Pressure

DLO’s Q1 2026 fundamentals were strong from a growth perspective.

Total payment volume was $14.055 billion, up 73% year over year.

Revenue was $335.9 million, up 55% year over year.

Gross profit was $118.7 million, up 40% year over year.

Operating profit was $52.8 million.

These figures show that dLocal is not just a concept story. It is processing significant payment volume and generating meaningful revenue and profit.

However, the margin picture is more mixed.

Gross profit margin declined to 35%, compared with 39% in the prior-year period.

Gross profit over TPV declined to 0.84%, compared with 1.05% in the prior-year period.

This means the company is scaling, but unit economics are under pressure.

Net income was $41.9 million, down 10% year over year. Excluding a prior-period tax adjustment, management indicated that net income would have been $51.6 million and diluted EPS would have been $0.17, up 11% year over year.

The adjusted view looks better than the headline net income figure, but investors still need to monitor profitability quality.

Cash is a strength.

As of March 31, 2026, cash and cash equivalents were $815.6 million, while corporate cash and cash equivalents were $451.8 million.

That gives dLocal financial flexibility.

The main weakness is adjusted free cash flow, which fell to $14.7 million, down 63% year over year. The company attributed this to working capital timing, tax credit netting, and advancement operations-related receivables.

That explanation may be reasonable, but investors need to see normalization in future quarters.

Operating Efficiency: Scale Is Improving, Unit Economics Are Under Pressure

From an operating efficiency perspective, dLocal is in a mixed but promising phase.

The company is clearly scaling.

TPV grew 73%. Revenue grew 55%. Gross profit grew 40%.

This is strong expansion.

However, the growth rates also reveal a key issue.

TPV grew faster than revenue, and revenue grew faster than gross profit.

That means the company’s monetization per dollar of TPV is declining.

This can happen for several reasons:

Larger merchants may have lower pricing.

New payment methods may carry different economics.

New geographies may have lower take rates.

FX spreads may compress.

Product mix may shift.

Competitive pricing may increase.

This does not mean the business model is broken. It means investors need to watch gross profit over TPV closely.

The company’s long-term operating leverage depends on whether gross profit continues rising fast enough to cover operating expenses and expand margins.

Management has indicated that operating leverage may improve in the second half of 2026.

That will be a key test.

If dLocal can grow TPV while stabilizing gross profit over TPV and improving free cash flow, the stock could earn a higher valuation.

If unit economics keep compressing, the market may discount the growth.

Financial Risk and Emerging Market Risk

DLO’s financial risk is not the same as an unprofitable fintech startup.

The company is profitable, has a large cash position, and operates at significant scale.

Q1 total assets were $1.826 billion, total liabilities were $1.272 billion, and total equity was $553.3 million.

That is a stronger balance sheet profile than many high-growth fintech companies.

However, several risks remain.

The first risk is margin compression. Declining gross profit margin and gross profit over TPV are the most important financial signals to monitor.

The second risk is free cash flow volatility. Adjusted free cash flow fell sharply in Q1, and investors need evidence that this was temporary.

The third risk is emerging market regulation. dLocal operates across many countries with different financial rules, tax systems, FX controls, and licensing requirements.

The fourth risk is currency volatility. FX movements can affect payment volumes, merchant behavior, settlement dynamics, and reported results.

The fifth risk is competition. Global payment firms, local acquirers, regional fintechs, and stablecoin-native payment providers all want access to the same emerging market commerce opportunity.

DLO’s growth story remains attractive, but it requires disciplined risk management.

DLO Rally Sustainability Score

Overall Score: 71/100

Rating: Strong growth story, but better after margin and free cash flow confirmation

Catalyst Clarity: 11/15

The rally is supported by Q1 growth, emerging market payment volume, stablecoin infrastructure, BNPL expansion, and local payments momentum. However, it is not a single major one-day acquisition or earnings-shock catalyst.

News Sentiment and Reliability: 8/10

The main data comes from official Q1 results, and growth metrics are strong.

Price and Volume Momentum: 12/15

A near-10% move with a strong intraday close shows positive momentum, but this is not an extreme breakout.

Technical Overheating Risk: 6/10

The move is meaningful but not excessive for a growth fintech stock. The main risk is failure near the $14.50 resistance area.

Sector Confirmation: 10/15

DLO is aligned with fintech, emerging market payments, stablecoins, BNPL, and global merchant infrastructure.

Fundamental Improvement: 11/15

TPV, revenue, and gross profit all grew strongly. However, net income and free cash flow require closer review.

Operating Efficiency: 6/10

Scale is improving, but gross profit over TPV declined and operating leverage still needs confirmation.

Financial Risk Management: 7/10

The company has cash and profitability, but margin pressure, working capital volatility, regulation, FX, and competition remain important risks.

What Investors Should Watch Next

The first factor is whether DLO can break above $14.50. The stock’s intraday high was near $14.46, so this level is the next short-term momentum test.

The second factor is whether DLO can hold above $14. If the stock holds this area, the market may be accepting the Q1 growth story.

The third factor is Q2 2026 results. Investors need to see whether TPV and revenue growth remain strong.

The fourth factor is gross profit over TPV. This fell to 0.84% in Q1 from 1.05% a year earlier. Stabilization or improvement would be positive.

The fifth factor is adjusted free cash flow. Q1 adjusted free cash flow declined sharply, and investors need evidence that working capital pressure normalizes.

The sixth factor is stablecoin adoption. Stablecoin Full could become an important product, but investors need to see real merchant usage and economic contribution.

The seventh factor is BNPL Fuse adoption. BNPL may help expand payment options in emerging markets, but the model must be managed carefully to avoid credit and regulatory risk.

The eighth factor is regulatory and FX exposure. Emerging market payments are attractive, but country-level risks can change quickly.

Bottom Line

dLocal’s latest rise is best understood as a growth-stock revaluation in emerging market payments.

The company delivered strong Q1 2026 results, with TPV up 73%, revenue up 55%, and gross profit up 40%. That confirms that the company’s payment infrastructure is scaling quickly across emerging markets.

The broader story is also attractive.

dLocal sits at the intersection of cross-border payments, local payment methods, global merchant expansion, stablecoins, BNPL, and emerging market digital commerce.

However, investors should not ignore the risks.

Gross profit margin declined. Gross profit over TPV fell. Adjusted free cash flow dropped sharply in Q1. Emerging market regulation, FX volatility, and competition remain ongoing risks.

DLO is not a low-quality speculative spike. It is a real fintech infrastructure company with scale, profitability, and cash.

But for the rally to become durable, the company needs to show that TPV growth can convert into stable gross profit, operating leverage, and stronger free cash flow.

For now, DLO looks like a high-growth fintech rebound with improving fundamentals, but investors should watch $14.50, Q2 results, margin stabilization, and FCF recovery before assuming a sustained breakout.

Related Reading

- https://www.dlocal.com/

- https://mgiedit.org/avav-stock-surge-aerovironment-bluehalo-defense-drone/

- https://mgiedit.org/irdm-stock-surge-rocket-lab-acquisition-satellite-infrastructure/

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, or a recommendation to buy or sell any security. Investors should conduct their own research and consider their risk tolerance before making investment decisions.