Wild Market Swings: A Look Inside the Week That Shook Investors – The financial markets just weathered one of the most chaotic weeks in recent memory, a period marked by dramatic reversals and head-spinning volatility. Despite the nail-biting ride, which included the biggest single-day rally since the 2008 financial crisis, the most intense volatility since the Covid-19 pandemic’s onset, a rapid selloff in bonds causing yields to spike, a sharp decline in the U.S. dollar’s value, and a rush to the safe haven of gold pushing it to record highs, the week concluded with all three major U.S. stock indexes registering gains of 5% or more.

For those on Wall Street, the week felt like a prolonged boxing match. Seasoned traders described an atmosphere thick with tension, where the lightning-fast ascents and equally precipitous drops in asset prices made it incredibly difficult to establish fair value. The sheer force and speed of these market movements left many feeling utterly exhausted, bracing for the possibility of continued instability.

As the Dow Jones Industrial Average capped off the week with a robust gain of over 600 points on Friday, market sentiment appeared to have stabilized somewhat. However, portfolio manager Jed Ellerbroek of Argent Capital Management in St. Louis offered a more cautious outlook. He noted that the significant declines witnessed earlier in the week, and in the week prior, had triggered numerous calls from clients contemplating whether to increase their equity holdings. Simultaneously, Ellerbroek expressed his concern about the increasing number of individual investors allocating larger-than-usual sums to broad stock market funds.

Ellerbroek suggested that these individual investors might be anticipating a swift recovery akin to the one that followed the initial shock of the 2020 Covid-19 pandemic, a downturn that proved to be relatively short-lived and was followed by a substantial market rally. However, he cautioned against overlooking the lessons of the 2008 financial crisis, during which stock prices plummeted by more than 50% and took several years to fully recover to their pre-crisis levels.

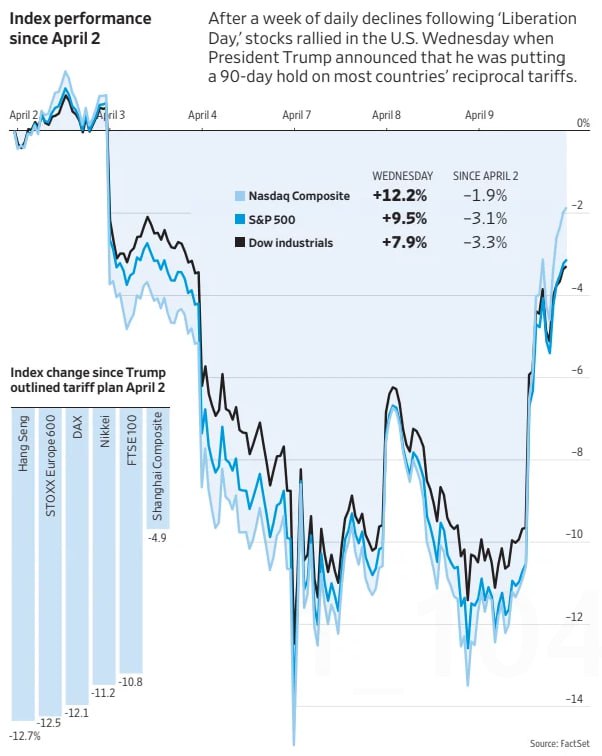

The S&P 500 index saw a gain of 1.8% on Friday, ultimately finishing the week with an impressive 5.7% increase. The technology-heavy Nasdaq Composite performed even stronger, rising by 2.1% on Friday and achieving a substantial weekly gain of 7.3%. The blue-chip Dow Jones Industrial Average added 1.6% on Friday, bringing its total weekly rise to a solid 5%.

Despite these positive weekly returns, it’s crucial to note that all three major indexes remain below the levels they were trading at when President Trump initiated his widely anticipated tariff increases from the White House Rose Garden in the previous week. Furthermore, all three indexes are still in negative territory for the year, highlighting the significant ground that needs to be recovered.

The heightened volatility that characterized the week had its roots in President Trump’s tariff announcements. These tariffs, broader and steeper than most investors, economists, business leaders, and trade partners had anticipated, sent shockwaves through the markets, triggering a four-day selloff. The peak of this tumultuous ride occurred on Wednesday.

Leading up to the market open on Wednesday, a rapid ascent in Treasury yields was already causing unease among investors. This anxiety was seemingly amplified when President Trump used social media to declare that it was “a great time to buy.” However, by the close of trading that day, U.S. stocks had executed a remarkable and historic rally. This dramatic turnaround was largely attributed to another online communication from the President, announcing a 90-day suspension of certain tariffs and signaling a potential shift towards a more conciliatory stance on trade negotiations.

The resulting market surge was described by investors as extreme, echoing past instances where stocks experienced sharp rallies during times of significant stress, only to subsequently fall to even greater lows. This phenomenon underscores the fragile nature of market confidence during periods of heightened uncertainty.

The Nasdaq Composite soared by over 12% on Wednesday, its largest single-day percentage gain since January 2001, during a brief recovery attempt amidst the bursting of the dot-com bubble. The S&P 500 added an impressive 9.5%, marking its best day since October 2008, at the height of the global financial crisis. The Dow Jones Industrial Average also participated in the rally, climbing by 7.9%, its biggest daily percentage increase since March 2020, when traders bought up shares in anticipation of a market collapse the following April.

However, the optimism generated on Wednesday proved to be short-lived. Much of these gains were reversed on Thursday as President Trump intensified the economic conflict with China, making it clear to investors on Wall Street that the trade war was far from a resolution. This renewed escalation of trade tensions quickly eroded the positive sentiment that had briefly taken hold.

Friday morning began on a negative note as well, following the release of the University of Michigan’s closely watched index of consumer sentiment. The index revealed a significant drop from the previous month, reaching one of the lowest levels in the past decade. This decline was primarily attributed to growing anxieties surrounding the ongoing trade disputes, as well as concerns about the outlook for employment and the potential for rising inflation.

Despite this initial downward pressure, the market’s resilience once again came to the fore. Strong first-quarter earnings reports from several major financial institutions, including Morgan Stanley, JPMorgan Chase, and BlackRock, provided a significant boost to investor confidence. This positive news from the financial sector helped to counteract the negative sentiment stemming from the consumer confidence data, even as the executives of these firms cautioned that President Trump’s trade restrictions posed a considerable risk to the overall health of the economy.

Shares of JPMorgan Chase experienced a notable 4% increase on Friday. BlackRock saw its shares rise by 2.3%, and Morgan Stanley’s stock price gained 1.4%. The strong performance of these financial giants played a crucial role in the market’s positive close to the week.

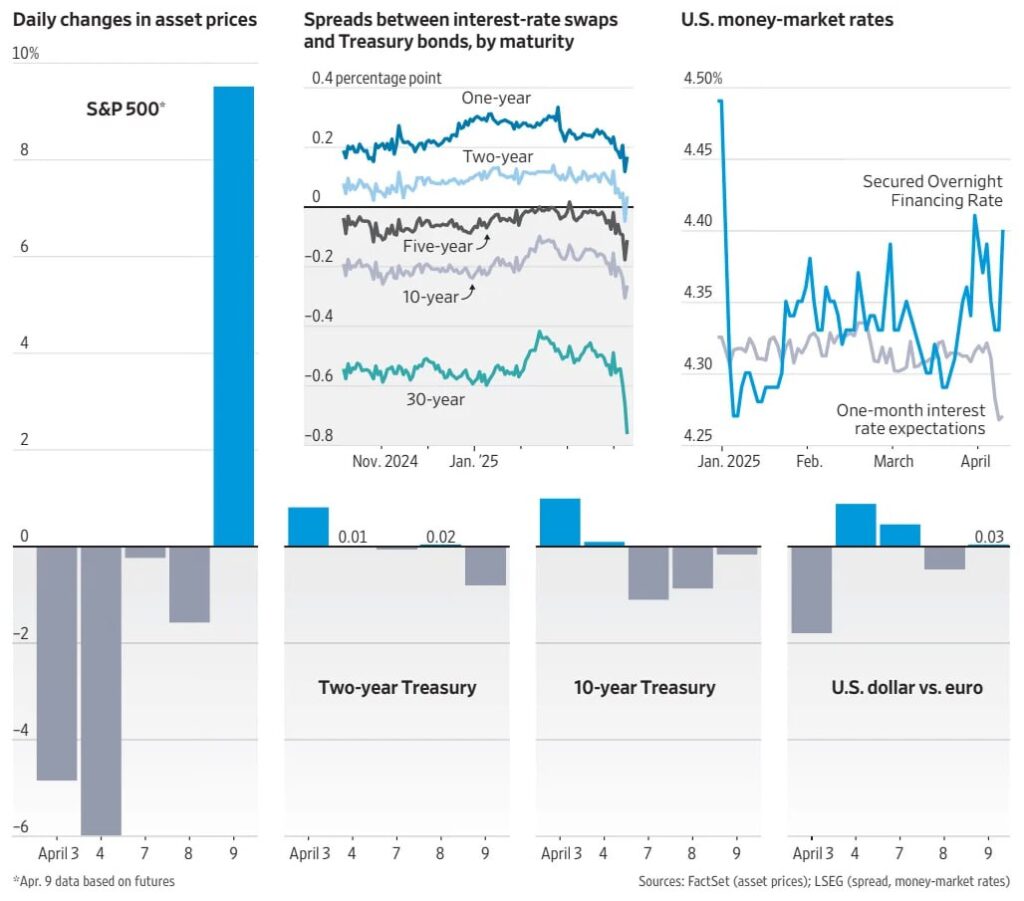

Adding to the market’s complexities, rising bond yields created fresh concerns among investors about the United States’ substantial federal budget deficit, its reliance on foreign investment to finance that deficit, and the increasing involvement of hedge funds in the U.S. Treasury market. These hedge funds often utilize significant amounts of borrowed money to purchase U.S. Treasurys, raising concerns about potential instability in the market. These factors collectively contributed to a significant selloff in Treasury bonds, a trend that only slightly moderated after President Trump’s tariff pause announcement.

The yield on the 10-year Treasury note, a key benchmark for setting borrowing costs throughout the economy, experienced its most significant one-week jump since November 2001, climbing by half a percentage point to just under 4.5%. The yield on the 30-year Treasury bond saw its most substantial weekly increase since April 1987, ending Friday at 4.873%.

The unusual phenomenon of both stock and bond prices falling sharply at the same time deeply unsettled many investors. This simultaneous decline raised fears of a potential disruption in the normal functioning of the Treasury market, which typically acts as a safe haven for investors during periods of stock market volatility.

As Treasury prices plummeted, the value of the U.S. dollar also declined, with traders showing a preference for other currencies like the euro. Foreign central banks hold U.S. dollars partly because of the ease and security associated with investing in U.S. Treasurys, which are generally more liquid and easier to trade than the bonds issued by other governments.

In response to the market turmoil, many investors sought refuge in gold, a traditional safe-haven asset. Gold futures surged by 2.1% to settle at a new record high of $3,222.20 a troy ounce, providing a boost to the stocks of gold mining companies. Shares of Freeport-McMoRan rose by 6.4%, while Newmont Corporation climbed by 7.9% on Friday, resulting in an impressive weekly gain of 24% for the company.

Prices for other commodities, including oil and copper, also saw gains on Friday, although their price movements have been as erratic as those of stocks in recent weeks. Benchmark U.S. oil futures added $1.43 per barrel on Friday, closing at $61.50. This represented a weekly decrease of 0.8%, and a more significant drop of 14% for the month.

These lower oil prices pose a potential threat to the profitability of the domestic oil industry’s ability to invest in and drill new oil wells. However, the decline in crude oil prices, along with those of diesel and gasoline, has prompted major fuel consumers, such as fishing fleets and trucking firms, to rush to lock in their future fuel costs using futures contracts, according to Charlie Macnamara, head of commodities at U.S. Bank.

Looking ahead, the market’s direction remains uncertain. While the week concluded with significant gains, the fundamental issues that triggered the volatility, particularly the ongoing trade disputes and their potential economic consequences, have not been resolved. The unexpected policy shifts from the Trump administration and the resulting market whiplash serve as a stark reminder of the fragility of investor confidence in the face of geopolitical and economic uncertainty. The interplay between trade policy, interest rates, and investor sentiment will likely continue to shape market movements in the weeks and months ahead.

https://mgiedit.org/2025-market-turbulence/

https://www.reuters.com/markets/how-china-went-courting-trump-never-yield-tariff-defiance-2025-04-13

답글 남기기