The Fed’s Pause: Why Traders Are Betting on a Longer Wait for Rate Cuts – In the wake of a surprisingly robust January jobs report, Wall Street traders are recalibrating their expectations about the Federal Reserve’s next moves. What once seemed like a clear path to multiple rate cuts in 2025 is now looking more uncertain. The possibility of an extended pause—or at least a much slower pace of easing—has gained traction among market participants.

But what does this mean for the economy, inflation, and investors? Let’s break it down.

Why Did the Fed Hit Pause?

To understand why traders are betting on a prolonged pause, we need to rewind to September 2024. At that time, two pressing concerns drove the Fed’s decision to slash interest rates by half a percentage point:

- Elevated Interest Rates: With the benchmark rate sitting between 5% and 5.5%, many believed the Fed was still stifling economic growth.

- Labor Market Weakness: A string of lackluster job reports during the summer months raised fears of a rapid slowdown in hiring.

Fast forward to today, and those worries have largely dissipated. The labor market remains resilient, with January’s jobs report showing steady gains despite falling slightly short of forecasts. Wage growth continues to hold firm, long-term unemployment has moderated, and revisions to prior months revealed stronger-than-expected hiring.

With these developments, the urgency to cut rates has faded. As Don Rissmiller of Strategas put it, “You still talk about it as a rate-cut cycle, but as the Fed’s target gets closer to 4%, it starts to feel like you can pause for a long time.” This sentiment reflects growing confidence that the economy is stable enough to withstand higher borrowing costs for longer.

What Does the Jobs Report Tell Us?

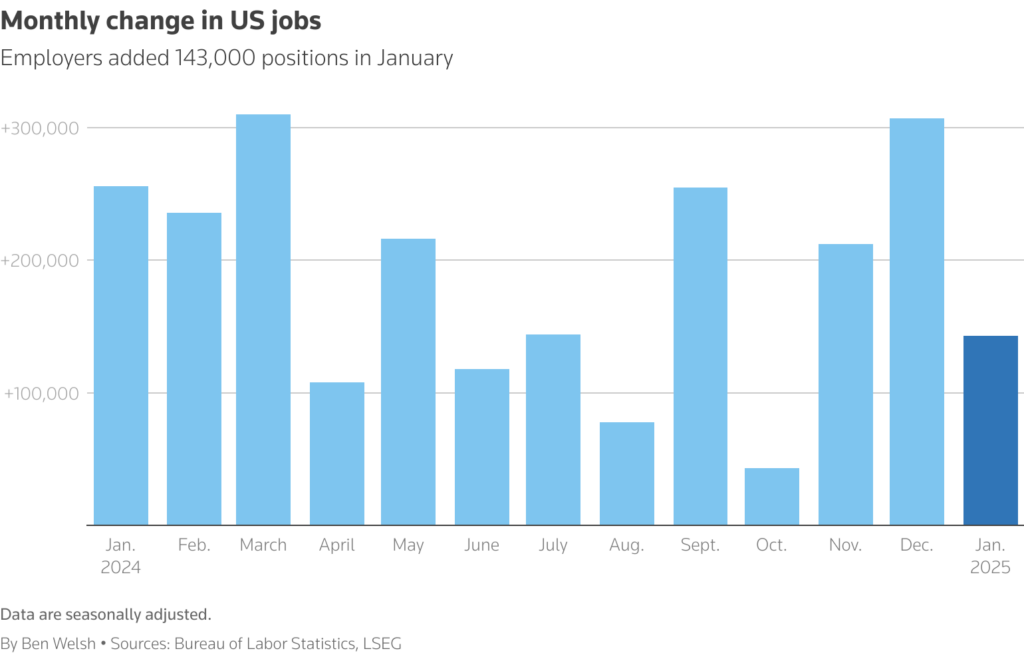

While January’s headline figure of 143,000 new jobs came in below the 169,000 predicted by economists, the details paint a brighter picture:

- Revisions Matter: November and December saw upward revisions totaling 100,000 jobs, suggesting the labor market is healthier than initially thought.

- Wage Growth Holds Steady: Average hourly earnings rose by 4.1% over the past year—a level consistent with inflation above the Fed’s 2% target.

- Unemployment Dips: The jobless rate ticked down to 4%, reversing its earlier uptrend.

These trends suggest that last summer’s gloomy predictions about the labor market were premature. Instead, the U.S. economy appears to be finding a balance between strength and sustainability.

Inflation: Still a Wild Card

Although the labor market looks solid, inflation remains a wildcard. The Fed’s preferred gauge—the core Personal Consumption Expenditures (PCE) index—currently stands at 2.6%, above the central bank’s 2% goal. For some economists, this raises red flags.

Steven Ricchiuto of Mizuho Securities USA warns against complacency. “We don’t believe in this Goldilocks scenario,” he says. “We’ve always been in the camp that inflation would be higher than expected.” His concern centers on wage growth, which suggests underlying inflationary pressures may persist. If wages continue climbing at their current pace, they could push prices higher, forcing the Fed to reconsider its dovish stance.

On the other hand, recent declines in goods prices excluding food and energy have provided some relief. According to Michael Reid of RBC Capital Markets, these categories have been instrumental in bringing inflation closer to the Fed’s target. However, potential policy changes—such as tariffs or tighter immigration rules—could reverse this progress. Tariffs, in particular, tend to drive up prices for imported goods, while reduced immigration could tighten the labor supply and exacerbate cost pressures.

Will the Fed Resume Cutting Rates?

Even if inflation ticks up, most analysts agree that outright rate hikes are unlikely—at least for now. After last year’s cuts, the Fed’s policy remains restrictive, albeit less so than in mid-2024. This gives policymakers room to sit tight and monitor incoming data before making further adjustments.

However, upcoming CPI data will be critical. Wednesday’s consumer price index release could either reinforce the case for patience or reignite calls for action. A surprise uptick in inflation might prompt the Fed to reassess its trajectory, while continued moderation could validate the current wait-and-see approach.

Policy Risks Lurking in the Background

One complicating factor is Washington’s role in shaping the economic landscape. Potential measures such as tax cuts, tariffs, and stricter immigration policies all carry inflationary risks. Economists warn that these initiatives could offset the Fed’s efforts to keep prices under control.

For instance:

- Tariffs: By increasing the cost of imports, tariffs directly impact consumer prices. Goods categories that have recently shown deflationary trends could see renewed pressure.

- Immigration Restrictions: Limiting the flow of workers into the U.S. could exacerbate labor shortages, driving up wages and production costs across industries.

If these effects materialize, the Fed will face a difficult choice: determine whether the inflationary impulses are temporary blips or signs of a structural shift requiring intervention.

Investor Takeaways

So, where does this leave investors? Here are three key considerations:

- Stay Flexible: Given the uncertainty surrounding both monetary policy and fiscal actions, maintaining a diversified portfolio is crucial. Bonds may offer some protection if inflation stays low, but equities remain attractive for those betting on sustained economic resilience.

- Monitor Inflation Data: Keep a close eye on upcoming CPI releases and wage trends. These indicators will shape the Fed’s decisions and, consequently, market sentiment.

- Prepare for Volatility: Political developments—whether from the White House, Congress, or global trade partners—could inject volatility into markets. Staying informed and nimble will help navigate potential turbulence.

Final Thoughts: Is Patience the New Strategy?

The Fed’s willingness to extend its pause underscores a broader theme: patience is becoming the cornerstone of monetary policy. Rather than rushing to stimulate or tighten, central bankers seem content to let the economy find its footing naturally.

But patience doesn’t mean passivity. The Fed remains vigilant, ready to act if inflation accelerates or the labor market falters. For now, though, the message is clear: stability trumps haste.

As Steven Ricchiuto aptly noted, “I think the Fed will have to take [inflation] on board.” Whether that means resuming rate cuts or holding steady depends on how the data unfolds—and how effectively policymakers manage external risks.

Related articles

https://www.reuters.com/markets/us/us-job-growth-misses-expectations-january-unemployment-rate-40-2025-02-07/

https://mgiedit.org/the-ai-paradox-how-automation/

답글 남기기