Confidence Collapse: U.S. Consumer Confidence Plunges 5.4 Points Under Trump’s Second Term

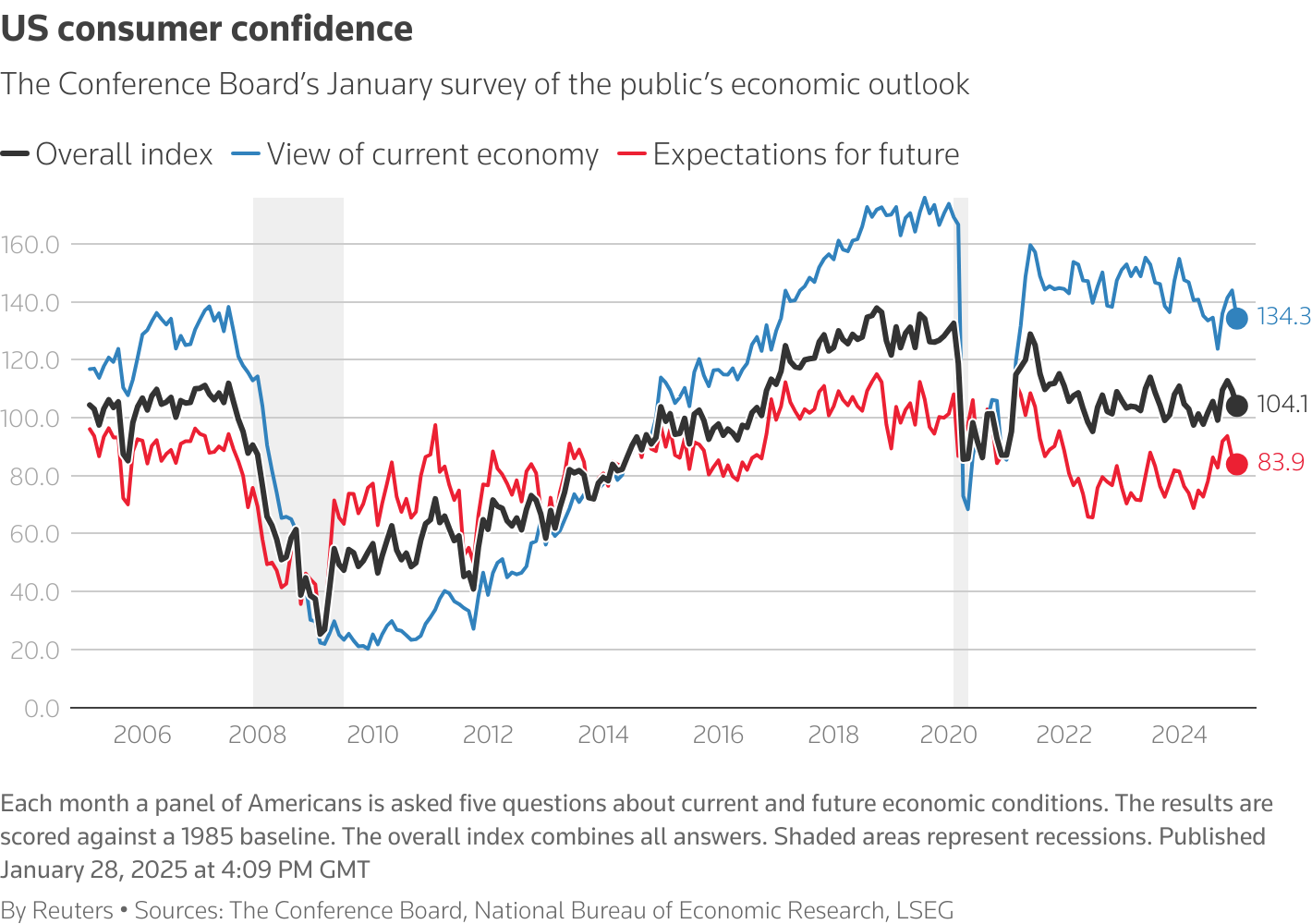

The Conference Board’s Consumer Confidence Index fell sharply to 104.1 in January 2025 (down from 109.5 in December), marking the largest two-month decline since 2022. Key drivers of the 5.4-point slump:

- Plunging Present Sentiment: The Present Situation Index cratered 9.7 points to 134.3, the steepest drop since April 2020, as optimism about jobs and business conditions evaporated.

- Youth Pessimism: Confidence among under-55s fell 8.1 points, while those over 55 saw a marginal 0.9-point gain.

- Wealthy Worries: Households earning over $125K reported a 12.3-point decline, the most of any income group.

Why It Matters: The index has now fallen in 7 of the last 12 months, reflecting persistent inflation, political polarization, and fears of a debt reckoning.

3 Critical Risks Threatening the 2025 Economy

Risk #1: The Inflation-Resurgence Trap

- Consumer Expectations: Year-ahead inflation forecasts rose to 5.3% in January, up from 5.1% in December.

- Policy Risks: Trump’s proposed 10% tariffs on China/Mexico/Canada could add 1.2% to CPI, per Moody’s Analytics.

- Energy Pressures: Gas prices spiked 12% YoY due to Middle East tensions, while electricity costs rose 6.8%.

Expert Warning:

“Tariffs and immigration crackdowns are a stagflation cocktail. Labor shortages in agriculture and construction could push wages—and prices—higher.”

– Mark Zandi, Chief Economist, Moody’s Analytics

Risk #2: The Debt Bomb

- Credit Card Balances: Hit $1.31 trillion in Q4 2024, with 22% of cardholders making only minimum payments (Philadelphia Fed).

- Delinquencies Rising: 90-day+ defaults surged to 3.8% of balances, the highest since 2012.

- Student Loans: Payments resumed in October 2024, draining $8B/month from consumer wallets.

Case Study: A household with $10K in credit card debt at 21% APR would need 26 years to repay by making minimum payments.

Risk #3: Policy Whiplash

- Pro-Business vs. Pro-Consumer:

- Corporate Tax Cuts: Proposed reduction from 21% to 15% could boost S&P 500 earnings by 8% (Goldman Sachs).

- Immigration Crackdown: Removing 3M migrant workers could shrink GDP by 0.7% in 2025 (CBO).

- Bond Market Rebellion: 10-year Treasury yields jumped 1 percentage point since September 2024, defying Fed rate cuts.

The Spending Paradox: Confidence Down, Consumption Up

Despite January’s gloom, consumers fueled a 3.1% Q3 2024 GDP growth—but cracks are emerging:

- Holiday Hangover: December retail sales rose 0.4%, but big-ticket purchase plans fell (e.g., autos, appliances).

- Savings Erosion: The personal savings rate dipped to 3.2%, near historic lows.

- Lipstick Effect: Spending on small luxuries (cosmetics, streaming) rose 4.9%, masking broader caution.

Red Flag: The Fed’s “Beige Book” reports rising loan rejections for low-income borrowers, signaling credit tightening.

Housing Market Split: Coastal Boom vs. Sun Belt Bust

The S&P CoreLogic Case-Shiller Index revealed stark regional divides in November 2024:

| Market | YoY Price Growth | Key Drivers |

| New York | +7.3% | Remote work revival, luxury demand |

| Chicago | +6.2% | Affordable vs. coastal hubs |

| Tampa | +0.4% | Overbuilding, insurance crises |

Takeaway: “Coastal markets defy national trends, but affordability is breaking down,” warns S&P’s Brian D. Luke.

Recession Odds: Why Economists Disagree

- Goldman Sachs: 30% chance, citing strong labor markets (unemployment at 3.7%).

- Deutsche Bank: 60% chance, pointing to inverted yield curve and falling industrial production.

- Wildcard: A 2025 oil shock ($100+/barrel) could tip the scales.

Historical Context: Since 1950, a Present Situation Index below 130 has preceded recessions 83% of the time. January’s reading: 134.3.

Strategic Moves for 2025: Expert Recommendations

- Debt Defense: Refinance credit cards into 0% APR balance transfers or credit union loans (avg. 9.5% APR).

- Inflation Hedge: Allocate 10-15% of portfolios to gold (+18% since 2024) and TIPS.

- Income Boost: Side hustles (e.g., freelance gigs, rental income) now contribute 6.3% of household earnings.

- Homeowner Prep: Lock fixed-rate mortgages before yields climb further; 30-year rates currently at 6.4%.

The Fed’s Tightrope: 2025 Rate Cut Projections

| Scenario | Fed Response | Market Impact |

|---|---|---|

| Inflation Stays Above 4% | Hold rates at 4.75% | Stocks -10%, Bonds +5% |

| Recession Signs Mount | Cut 1.5% by Q4 | Gold +25%, USD -7% |

| Stagflation (GDP -1%, CPI 5%) | No clear path | Volatility spikes |

Key Quote:

“The Fed is out of ammo. They can’t cut rates without reigniting inflation, but hiking would crush consumers.”

– Neil Sutherland, Schroders

The Political Wildcard: Midterms and Market Moves

- Democrat Strategy: Frame economic anxiety as policy failure; target swing districts with inflation relief pledges.

- GOP Counter: Highlight stock market highs (S&P 500 +14% since Trump’s 2024 win) and deregulation wins.

- Investor Playbook: Defense stocks (Lockheed Martin +22% YTD), tariffs beneficiaries (U.S. Steel +18%), and AI tech (Nvidia +34%).

The Bottom Line: Navigating 2025’s Economic Storm

January’s confidence crash is a wake-up call. While the U.S. economy remains resilient, households face a trifecta of inflation, debt, and policy risks. For investors, diversification and defensive positioning are critical. For consumers, emergency savings and debt reduction are non-negotiable.

답글 남기기