The Warsh Shock and the Re-rating of Market Risk

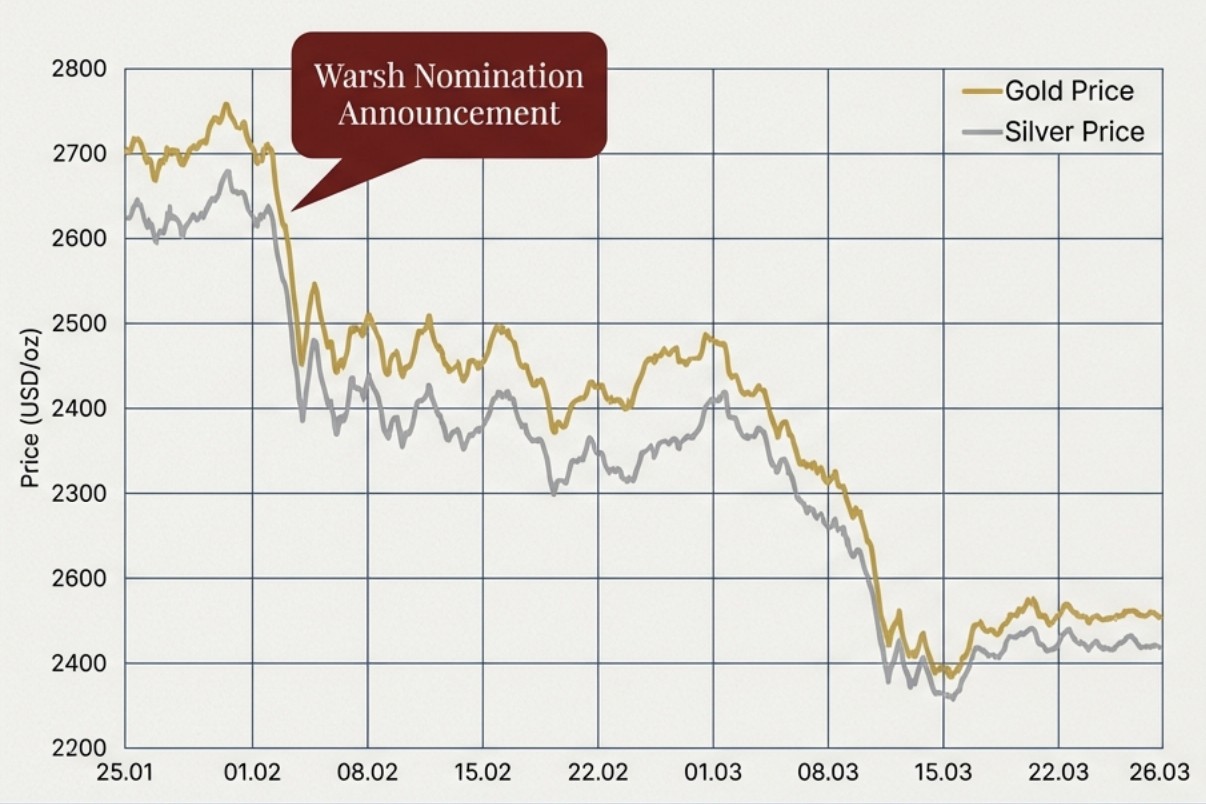

The nomination of Kevin Warsh as the next Chair of the Federal Reserve has triggered a violent re-anchoring of the term premium. This is not merely a personnel transition; it is an aggressive pivot away from the “Powell Era” and toward a paradigm of “regime change” that seeks to dismantle the QE-dependence of the last two decades. The immediate market response in early February 2026 was visceral: “safe-haven” assets faced a brutal liquidation, with gold and silver prices experiencing a precipitous decline as the prospect of a less interventionist Fed took hold. Simultaneously, the U.S. dollar index (DXY) saw its losses narrow sharply, signaling a pivot away from the expectation of sustained fiscal dominance.

However, from a strategic perspective, the “Warsh Shock” was as much a technical event as an ideological one. As noted in recent iM Securities analysis, the volatility served as a convenient pretext for profit-taking in asset classes that were already overextended. While the USD/KRW exchange rate briefly tested the 1,420 level on hopes of a more dovish transition, the nomination of a “policy disruptor” has forced a recalibration. We are now entering a period where the market must price in a leader who views the current Fed framework as fundamentally “broken,” shifting the focus from the visceral shock of the nomination to the ideological history of the man himself.

The Ideological Evolution: From Crisis Hawk to AI Pragmatist

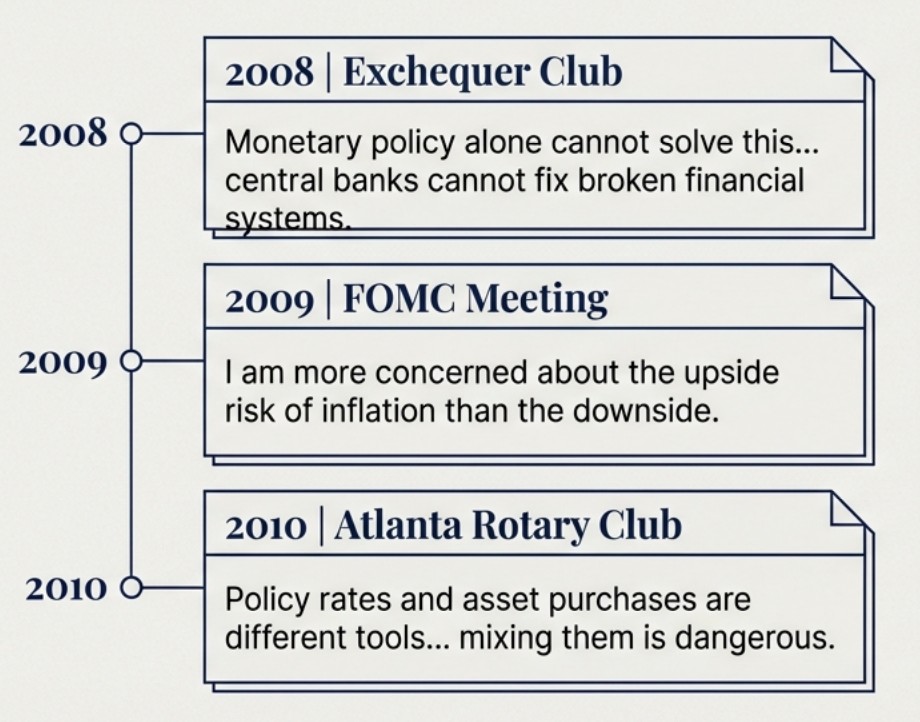

Kevin Warsh’s record is the primary lens through which the market is currently pricing future risk. His evolution from a 2008-era critic of “central bank overreach” to a 2026 “AI Pragmatist” represents a sophisticated shift in how the Fed may balance growth and inflation.

• The 2008-2011 “Hawk”: During his previous tenure, Warsh emerged as a leading skeptic of Quantitative Easing (QE), arguing that asset purchases were emergency measures that had morphed into permanent market distortions. He famously cautioned that the Fed’s balance sheet expansion was eroding policy flexibility and pushing the central bank into the dangerous territory of fiscal policy.

• The 2025-2026 “Pragmatist”: In his recent communications, most notably his 2025 Wall Street Journal op-ed, “The Federal Reserve’s Broken Leadership,” Warsh has signaled a shift toward productivity-driven disinflation. He argues that the AI revolution is a secular force that naturally suppresses inflation, providing the Fed with the cover to support aggressive rate cuts while simultaneously aggressive in its institutional downsizing.

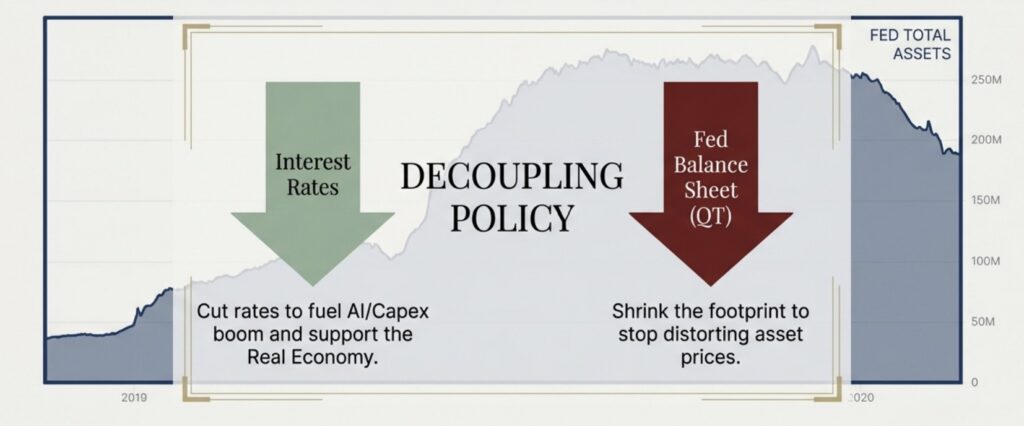

This synthesis forms the “Warsh Doctrine”: Low Rates + Small Balance Sheet. By decoupling the price of money (interest rates) from the quantity of money (the balance sheet), Warsh intends to shift liquidity from “Wall Street to Main Street”—a move that increases the policy error risk premium as the Fed moves from being a “reactive” data-dependent body to an “ideological” one.

The “Small Fed” Alliance: Warsh, Bessent, and the White House Vision

The Warsh nomination cements a powerful “Small Fed” alliance with Treasury Secretary Scott Bessent. Both leaders share a visceral disdain for the Fed’s “institutional obesity” and the mission creep that has seen the central bank become a primary manager of the national debt. Bessent has been clear that bond purchases during non-crisis periods create profound economic distortions, a sentiment Warsh echoed in his critique of the Fed’s over-reliance on government data and economic forecasting.

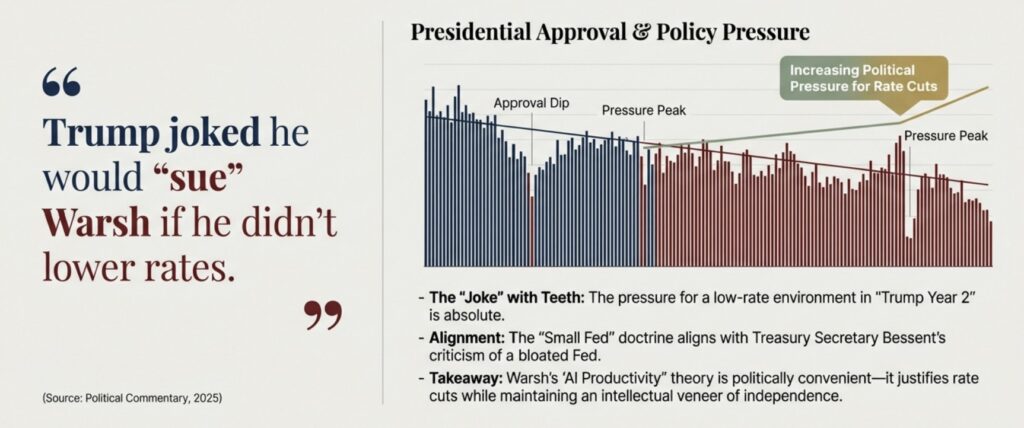

This alliance marks a departure from traditional “hawk vs. dove” binaries. Warsh is a “policy disruptor” who may be more “dovish” on rates than Powell, provided he can aggressively curtail the Fed’s footprint in the Treasury market. However, the political reality is fraught. President Trump’s recent “joke”—suggesting he would sue Warsh if he failed to cut rates—highlights the intense pressure the new Chair will face. This lack of perceived independence, combined with a shift toward “regime change” policy, suggests that while the “Small Fed” vision is clear, its implementation will be a primary source of market friction.

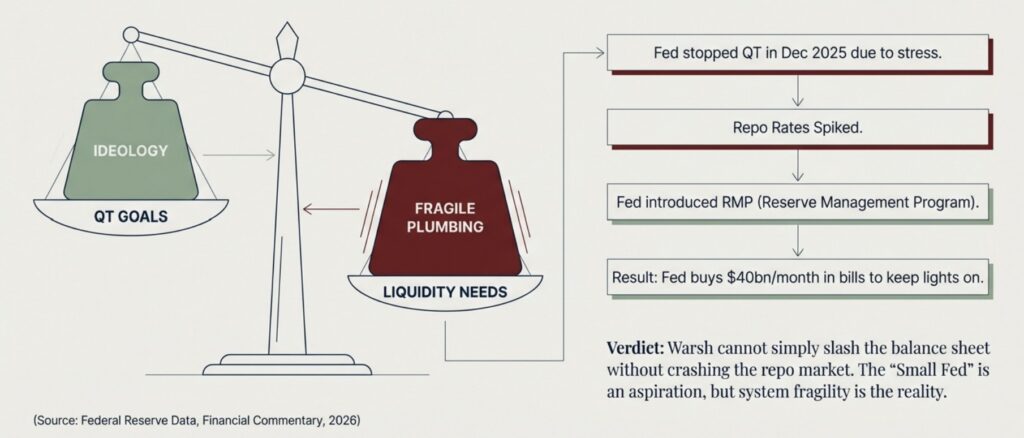

The QT Reality Check: Structural Constraints on De-leveraging

Despite the ideological commitment to a “Small Fed,” the technical plumbing of the short-term funding markets acts as a natural brake on Warsh’s agenda. The Fed cannot unilaterally shrink the balance sheet without risking the “monetary accidents” that led to the halt of Quantitative Tightening (QT) in late 2025.

The strategic friction is best illustrated by the Reserve Management Program (RMP). Launched on December 12, this program involves $40 billion in monthly short-term Treasury purchases to ensure the banking system maintains “ample reserves.” This “hidden” form of liquidity support directly contradicts the Warsh ideology of a smaller Fed footprint. As Kiwoom Securities notes, the necessity of maintaining system stability in a high-deficit environment makes a return to aggressive QT technically perilous. Warsh will be forced to balance his desire to de-lever the Fed against the reality of a repo market that remains sensitive to reserve levels, likely leading to a more cautious, “collective decision-making” approach within the FOMC than his rhetoric suggests.

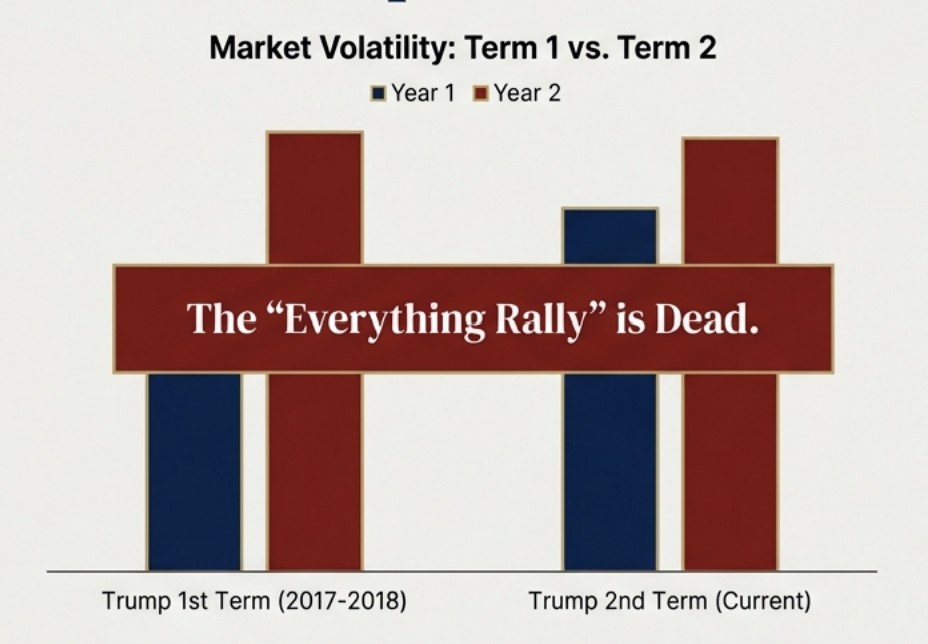

Strategic Outlook: Volatility in the “Trump 2nd-Year Jinx”

As we navigate 2026, the macro environment is entering the “Trump 2nd-year jinx,” characterized by geopolitical flashpoints—most notably Iran—and the return of domestic fiscal hurdles like government shutdowns. The “Everything Rally” has officially fragmented into a bifurcated market, where liquidity is no longer a rising tide for all boats.

• FX & Rates: The USD/KRW is now locked in a high-volatility corridor between 1,420 and 1,460. While the “Warsh Doctrine” favors lower short-term rates, the end of the “Fed put” for bonds will maintain upward pressure on long-term yields.

• Equity & Commodities: The fragility of this transition is already evident in specific asset classes. We have recently witnessed a 25% intraday crash in Natural Gas and a sharp correction in the Indonesian stock market, serving as a warning that global liquidity is being re-routed. While the Mag-7 (M7) may find support in the AI productivity narrative, the broader market is vulnerable to the withdrawal of “Wall Street liquidity.”

The final strategic takeaway is clear: the “Warsh Doctrine” guarantees a higher volatility regime. Investors must recognize that the era of suppressed long-term rate volatility is over. Success in 2026 will depend on navigating the friction between a “Small Fed” ideology and the cold, hard requirements of global financial stability. Success for Warsh himself will be measured by whether he can shrink the institution without breaking the markets it supports.

답글 남기기