The Trump Era’s Economic Report Card: Early Shocks and Future Outlook

The initial phase of any new presidential administration brings a flurry of policy changes, each with the potential to reshape the economic landscape. As we cross the 100-day mark under President Trump’s current term, the first concrete economic indicators are beginning to emerge, offering a glimpse into the early impacts of his policies. While initial sentiment indicators had already shown some shifts, the true test lies in the real economic data. The recently released first-quarter GDP figures for the United States provide a critical, albeit early, look at how the world’s largest economy is faring.

This analysis, drawing on recent economic data and expert commentary, delves into the performance of the US economy in early 2025, examining the factors contributing to the unexpected contraction in GDP, the resilience of domestic demand, the significant impact of trade policies, and the evolving picture of the labor market. We will also explore the implications for monetary policy and venture into potential futuristic predictions based on current trends and policy trajectories.

A Deeper Look at the Q1 2025 GDP Contraction

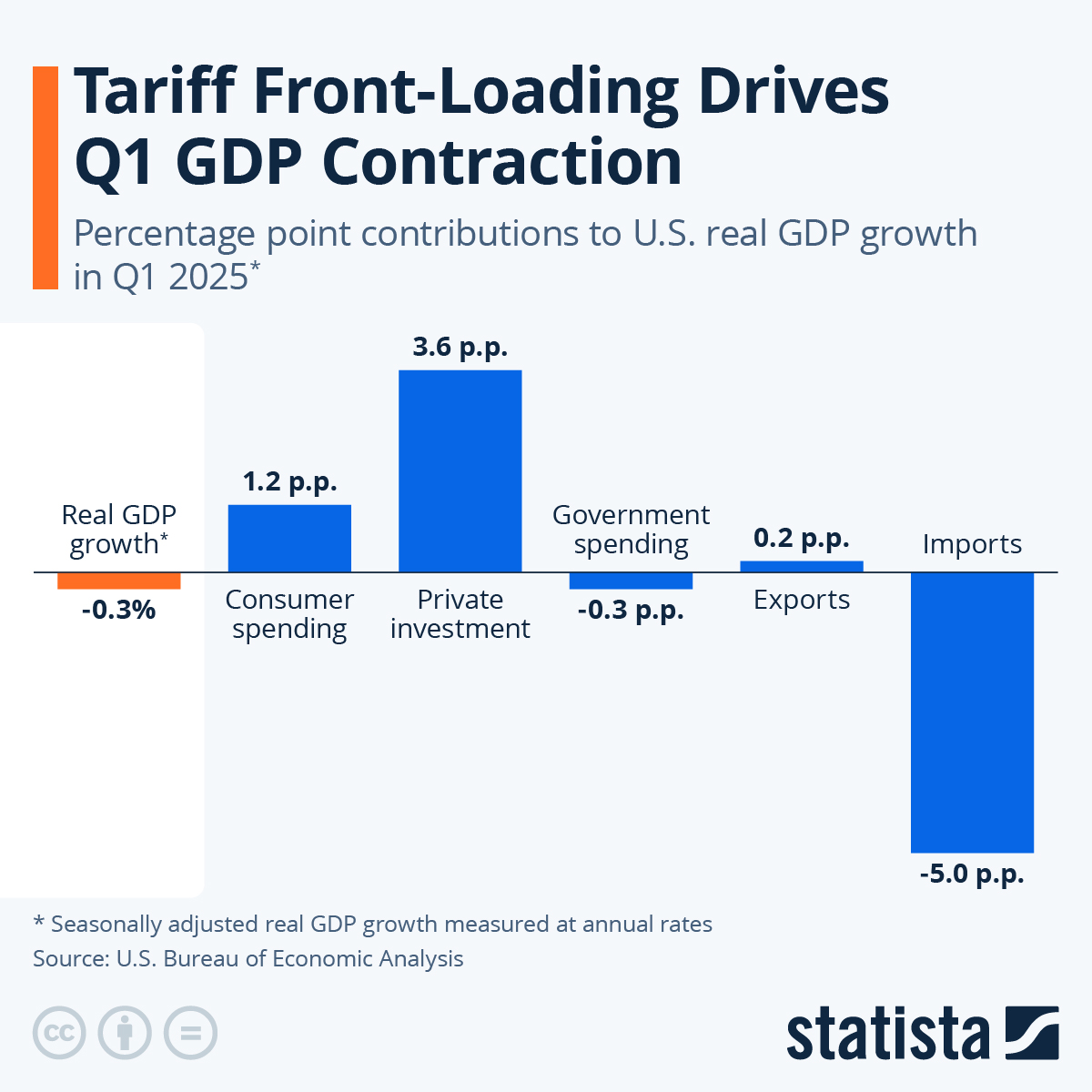

The headline figure for the US economy in the first quarter of 2025 was a surprising annualized contraction of 0.3%. This marks the lowest growth rate since the first quarter of 2022 and stands in stark contrast to the average quarterly growth rate of 2.5% observed in the previous year. This downturn signals a potential slowdown in the US’s economic momentum.

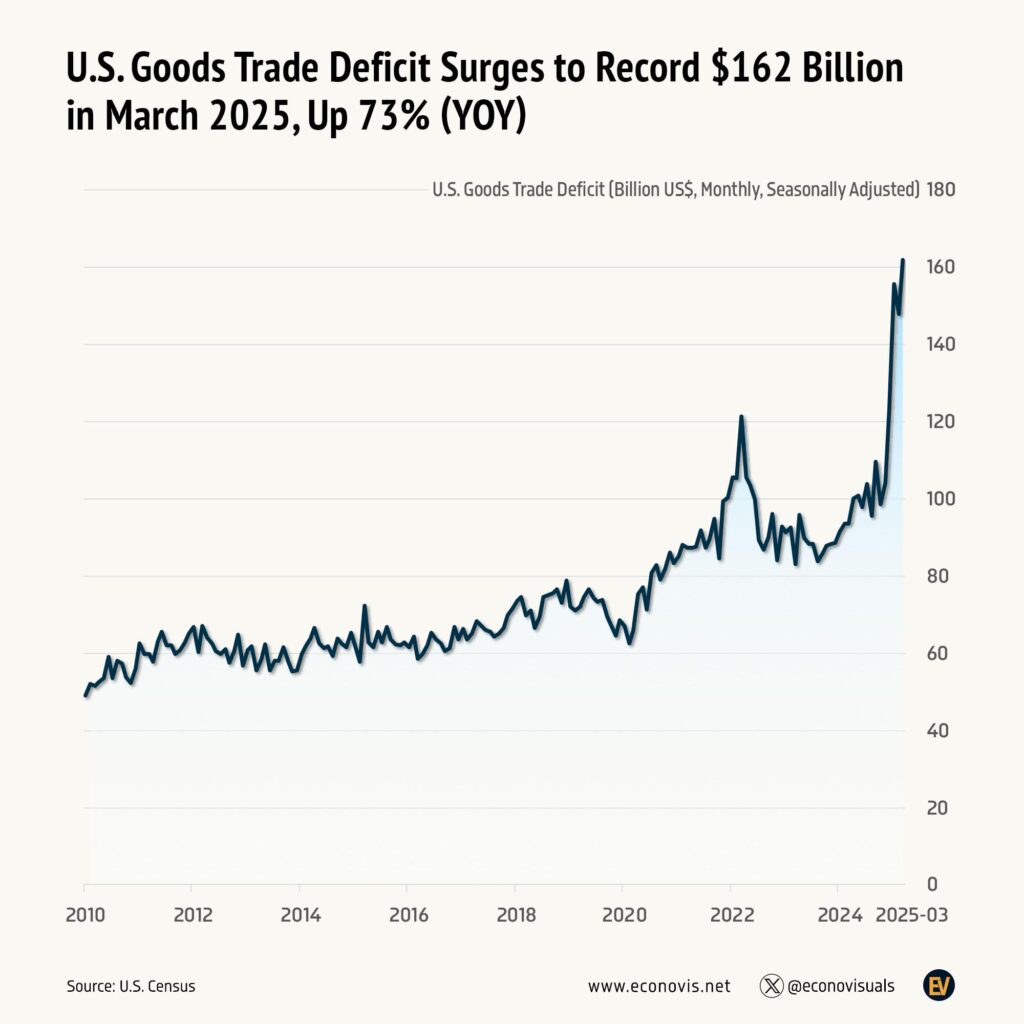

While the negative GDP figure might seem alarming at first glance, a deeper dive into the components reveals a more nuanced picture. Domestic demand, surprisingly, remained robust during this period. The primary driver of the sharp decline in GDP was a significant drop in net exports, which subtracted a substantial 4.8 percentage points from the growth rate. This precipitous fall in net exports was largely anticipated, given the surge in import volumes that occurred before the full implementation of the Trump administration’s tariff policies. This pre-emptive increase in imports led to a sharp widening of the US trade deficit.

It is also important to consider the nature of the increased imports in the first quarter. A significant portion of this increase was likely driven by businesses stocking up on goods in anticipation of rising costs due to tariffs. This is reflected in the strong contribution of inventory investment to the Q1 GDP, which added 2.3 percentage points. Therefore, the negative impact on growth from the surge in imports might be temporary.

Despite the contraction in headline GDP, personal consumption and fixed investment showed relative strength, contributing 1.2 and 1.3 percentage points to growth, respectively. This suggests that domestic fundamentals were not as weak as the headline figure might imply.

Table 1: Contribution to US GDP Growth by Component (Q1 2025, Annualized % Change)

| Component | Contribution (%p) |

| Personal Consumption | +1.2 |

| Fixed Investment | +1.3 |

| Inventory Investment | +2.3 |

| Net Exports | -4.8 |

| GDP Growth | -0.3 |

The Resilience (and Potential Softening) of Consumer Spending

With the external sector facing uncertainty due to tariff policies, the focus shifts to the resilience of domestic demand, particularly household consumption. While consumer sentiment has fallen sharply due to concerns about the future economic outlook, this has not yet translated into a significant decline in actual spending.

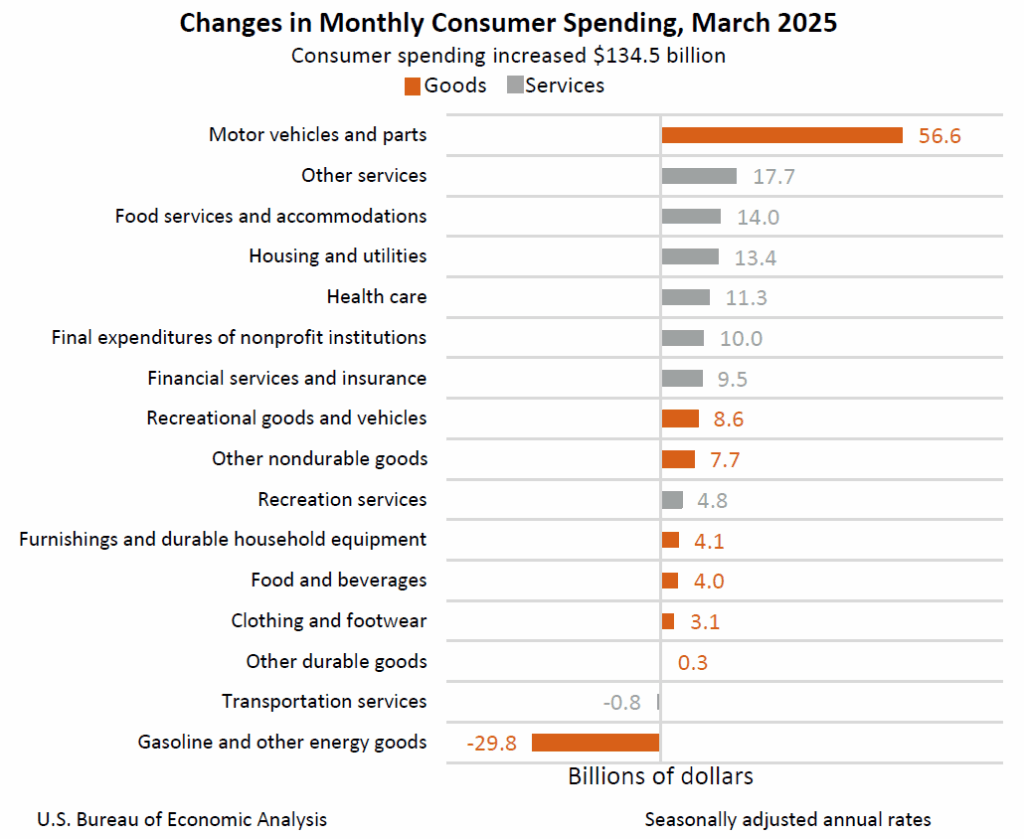

Recent data for March 2025 showed a 0.5% increase in personal income and a 0.7% increase in personal consumption compared to the previous month. However, it’s possible that some of this spending was accelerated by consumers looking to purchase goods before potential price increases resulting from tariffs. This suggests a potential moderation in demand in the latter half of the year.

An examination of consumer spending by category in March 2025 reveals that motor vehicles and parts were the largest contributors to the increase in personal consumption. This could be particularly sensitive to tariff impacts. However, spending also increased in service sectors less directly exposed to tariffs, such as dining out, housing, and healthcare.

Despite growing concerns about a potential recession, the household saving rate, as a percentage of disposable income, was 3.9% in March, slightly lower than the 4.1% in the previous month. Typically, households tend to save more when recession fears rise. The current lower saving rate might indicate that while sentiment is weak, actual financial behavior has not yet fully reflected this pessimism.

There appears to be a time lag between the increase in tariffs, the resulting rise in consumer prices, and the eventual impact on household consumption through a reduction in real income. This suggests that the full effect of tariff-induced price increases on consumer spending may yet to be seen.

Table 2: Changes in Monthly Consumer Spending, March 2025 (Billions of Dollars)

| Category | Change ($ Billions) |

| Motor vehicles and parts | 56.6 |

| Other services | 17.7 |

| Food services and accommodations | 14.0 |

| Housing and utilities | 13.4 |

| Health care | 11.3 |

| Final expenditures of nonprofit institutions | 10.0 |

| Financial services and insurance | 9.5 |

| Recreational goods and vehicles | 8.6 |

| Other nondurable goods | 7.7 |

| Furnishings and durable household equipment | 4.8 |

| Recreation services | 4.1 |

| Food and beverages | 4.0 |

| Clothing and footwear | 3.1 |

| Other durable goods | 0.3 |

| Transportation services | -0.8 |

| Gasoline and other energy goods | -29.8 |

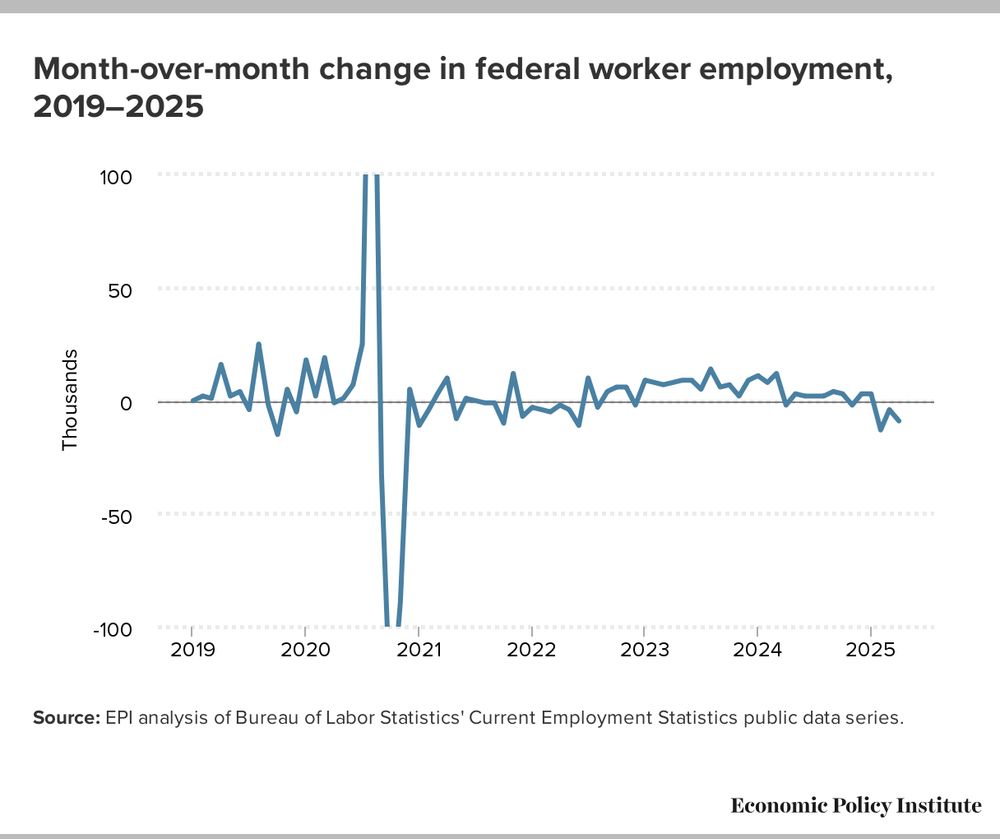

The Evolving Labor Market Picture

While the weakness in Q1 GDP might be partially attributed to temporary factors related to trade, the softening in the labor market points towards a more definitive slowdown in the US economy’s trajectory.

Data indicates a rapid decline in job openings by businesses. In March, the number of job openings fell to 109,000, suggesting the labor market is moving closer to equilibrium. Furthermore, the ADP’s measure of private sector employment showed a significant slowdown in hiring in April, with only 62,000 new jobs added, considerably below the expected 115,000.

A weakening labor market could provide further justification for the US Federal Reserve to consider interest rate cuts.

Monetary Policy Implications

The softening economic data, particularly in the labor market and the potential for tariff impacts to eventually weigh on consumer spending, strengthens the case for the Federal Reserve to consider easing monetary policy. The prevailing view is that the Fed will assess whether the inflationary pressures stemming from tariffs are temporary before making any moves.

The expectation is that the Federal Reserve will maintain its current stance of two interest rate cuts within the year, with the first potentially occurring in June. However, the March FOMC minutes revealed that some members were concerned about the potential for tariff-induced price increases to be more persistent, which could make the case for rate cuts less compelling. Despite this, the market’s expectation of 3-4 rate cuts within the year might be overly optimistic.

The Bank of England is also expected to cut its benchmark interest rate by 25 basis points in May, bringing it to 4.25%. This decision is anticipated despite consumer price inflation exceeding the BOE’s target, particularly in the services sector. The increasing downside risks to the economy due to uncertainty surrounding US tariff policies are likely to outweigh the concerns about inflation in the BOE’s decision-making.

Global Economic Sentiment and Trade Impacts

The economic slowdown is not limited to the United States. Business sentiment in the Eurozone’s service sector is also expected to weaken, nearing a contractionary phase. The uncertainty surrounding US tariffs on goods from the EU is a significant factor contributing to this weakening sentiment. The service sector PMIs in Germany and France, two of the Eurozone’s largest economies, have already seen significant declines, entering contractionary territory and pulling down the overall Eurozone index.

China’s export sector is also facing significant challenges due to the imposition of US tariffs. This is likely to have a substantial negative impact on China’s export performance. While there are some signs that the US’s hardline stance on tariffs might be softening, a prolonged and difficult negotiation process between the US and China could limit the potential for a rebound in China’s export economy.

The slowdown in exports is expected to contribute to continued deflationary pressures in China. Weak domestic demand is already keeping a lid on demand-side inflation, and falling food prices, particularly for beef, are further contributing to the decline in consumer prices. The sharp decline in exports to the US is likely to exacerbate the issue of domestic oversupply, intensifying the downward pressure on prices.

Futuristic Predictions: Navigating a Fragmented Global Economy

Looking ahead, the current economic climate suggests a period of increased volatility and uncertainty. The interplay between protectionist trade policies, evolving monetary stances by major central banks, and shifts in labor market dynamics will shape the global economic trajectory.

Prediction 1: Persistent Trade Tensions and Supply Chain Realignment

While there might be periods of negotiation and potential de-escalation, the underlying structural factors driving protectionist tendencies are likely to persist. This will continue to create uncertainty for businesses and necessitate a significant realignment of global supply chains. Companies will prioritize resilience and geographical diversification over pure cost optimization, leading to increased near-shoring or friend-shoring of production. This shift will have long-term implications for global trade flows and investment patterns. We could see the emergence of more regional trade blocs and a less interconnected global economy than we have become accustomed to. This fragmentation could lead to higher production costs and potentially contribute to persistent, albeit perhaps lower, levels of inflation compared to the pre-tariff era.

Prediction 2: Divergent Monetary Policy Paths and Currency Volatility

Major central banks will likely navigate increasingly divergent paths based on their domestic economic conditions and the specific impacts of trade policies and other global shocks. While the US Federal Reserve may proceed with gradual rate cuts, the pace and extent will be highly dependent on the inflation outlook and labor market health. Other central banks may be forced to ease more aggressively to counteract the negative impacts of trade wars and weakening global demand. This divergence in monetary policies will likely lead to increased volatility in currency markets, creating additional challenges for international businesses and investors. The US dollar’s strength could fluctuate significantly depending on the relative pace of economic recovery and monetary policy adjustments globally.

Prediction 3: Technology and Automation as Mitigating Factors (and Job Disruptors)

In response to rising labor costs and supply chain uncertainties, businesses will accelerate the adoption of automation and advanced technologies. This could partially mitigate the inflationary pressures from trade barriers and labor shortages in certain sectors. However, it will also accelerate the transformation of the labor market, potentially leading to job displacement in some industries and a higher demand for skills in technology and automation. Governments will face increasing pressure to implement policies that support workforce training and adaptation to this evolving landscape.

Prediction 4: Increased Fiscal Policy Activism

With monetary policy space potentially limited by inflation concerns or already low interest rates, governments may increasingly turn to fiscal policy to stimulate economic growth and address the negative impacts of trade policies. This could involve targeted tax cuts, infrastructure spending, or subsidies for specific industries deemed strategically important. However, increased fiscal activism could also lead to rising government debt levels, creating long-term fiscal challenges.

Prediction 5: The Growing Importance of Intangible Assets

In a more fragmented and uncertain global economy, the value of intangible assets such as intellectual property, data, and strong brand recognition will become even more critical for business success. Companies with unique technologies or strong customer loyalty will be better positioned to navigate trade barriers and supply chain disruptions. Investment in research and development and data analytics will be key differentiators.

Prediction 6: Geopolitical Factors Intertwined with Economic Policy

Economic policy, particularly trade policy, will remain deeply intertwined with geopolitical considerations. Trade relationships will increasingly be viewed through a national security lens, leading to potential further restrictions on technology transfers and foreign investment in sensitive sectors. This complex interplay between economics and geopolitics will add another layer of uncertainty for businesses operating on a global scale.

Conclusion

The first quarter 2025 GDP data for the US, while impacted by temporary trade-related factors, serves as a crucial warning signal. The underlying trends in the labor market and the potential for delayed impacts of tariffs on consumer spending suggest that the US economy is likely entering a period of slower growth. The global economic outlook is similarly challenged by trade tensions and divergent monetary policy paths.

Navigating this complex environment will require careful policy responses from governments and adaptability from businesses. The future economic landscape will likely be characterized by ongoing shifts in trade patterns, technological acceleration, and a closer link between economic policy and geopolitical considerations. While challenges abound, these shifts also present opportunities for innovation and strategic repositioning. The coming quarters will be critical in determining whether the current headwinds lead to a more significant downturn or a recalibration towards a new, perhaps more regionalized, form of global economic engagement.

This analysis suggests that the “America First” approach, while intended to bolster the domestic economy, carries significant risks of disrupting global trade and impacting economies worldwide. The coming months will provide more clarity on the extent of these impacts and the ability of policymakers to navigate the complex economic and geopolitical challenges ahead. The world watches keenly to see how these early tremors will shape the economic landscape for the remainder of the decade and beyond.

https://www.reuters.com/business/us-goods-trade-deficit-widens-sharply-march-2025-04-29/

https://mgiedit.org/americas-ambition-to-reclaim-maritime-might/

답글 남기기