The New Tariff Trap: Rare Earths, Forced Investment, and the Looming Shadow of Gold – The global trade system finds itself at a perilous crossroads, a situation dramatically worsened by recent aggressive maneuvers from the world’s two largest economies. The U.S.-China relationship, already strained by years of tit-for-tat tariffs, has entered a volatile new phase. This pivotal shift hinges on China’s near-monopoly control over rare earth elements and President Trump’s firm demand for foreign nations to reinvest trade surpluses directly into the U.S. economy.

This is no longer a simple trade dispute over manufactured goods; it represents a profound struggle for control over the critical materials vital for the 21st-century economy and a direct challenge to the very structure of global financial hegemony. The actions taken in October 2025—China’s rare earth export controls and America’s punitive, sweeping tariffs—threaten to halt the recent market rally. They also evoke unsettling historical parallels, chief among them the “Kindleberger Vortex” which famously accelerated the Great Depression.

The stakes extend far beyond immediate market volatility. The core issue is the erosion of trust in the global financial leader, the United States. This forces nations to fundamentally re-evaluate their reliance on the U.S. dollar as a reserve asset, driving them toward the ultimate “hard money”: gold. This report dissects the current “Tariff Trap,” analyzes the geopolitical leverage points, and projects the long-term consequences for global trade, U.S. bond markets, and the future of the dollar’s dominance.

Part I: The Rare Earths Showdown and the Tariff Escalation

The immediate catalyst for the current crisis is China’s strategic weaponization of its dominant position in the global rare earth supply chain. This move significantly impacts critical materials for various industries.

China’s Rare Earth Monopoly: Beyond Reserves to Processing Power

Rare earth elements are indispensable components of modern technology, vital for everything from electric vehicles (EVs) and advanced weaponry to consumer electronics. China’s control over this entire value chain is immense, making it a key player in rare earth supply chain security.

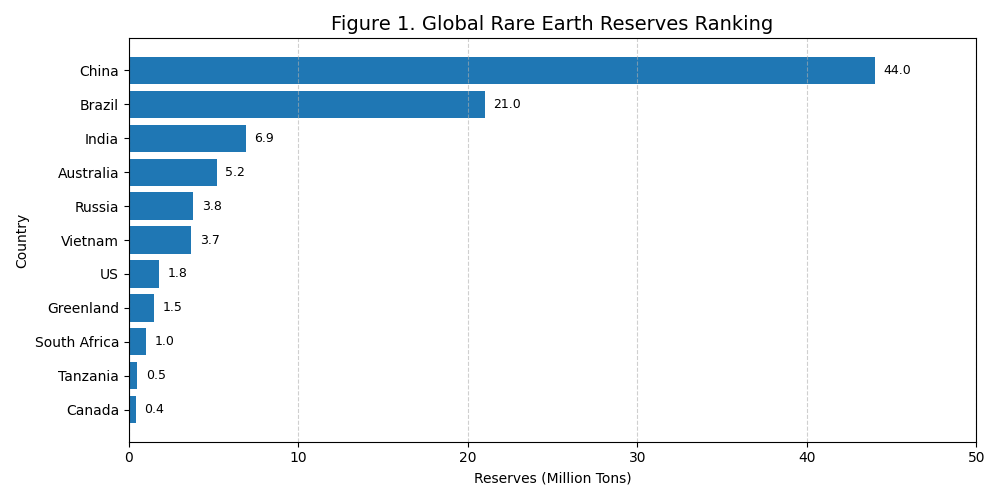

- Dominant Reserves: China holds the world’s largest rare earth reserves, estimated to be about 20 times larger than those in the United States.

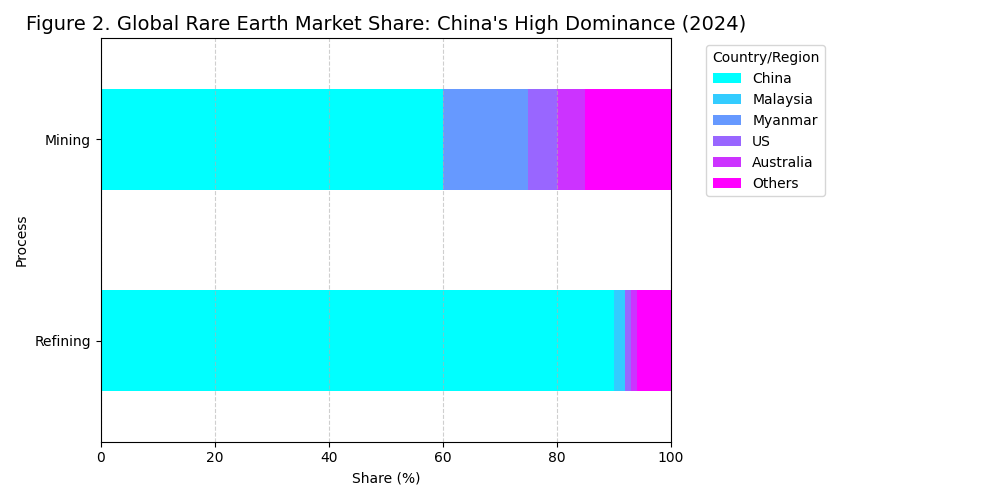

- Processing Dominance: More critically, China controls over 90% of the world’s rare earth refining and processing capacity. This constitutes the most significant choke point, affecting the entire value chain from mining to final use and highlighting the need for diversified rare earth processing.

- Supply Chain Impact: The severity of this supply risk was starkly underscored in May 2025, when Ford was forced to halt production at a factory due to critical rare earth procurement issues.

The recent measure, Ministry of Commerce Notice 2025 No. 61 (announced October 9, 2025), represents Beijing’s most assertive move to date, specifically targeting the global defense and advanced technology sectors.

- The 0.1% Rule: New regulations establish a “0.1 per cent rule,” requiring Chinese government approval for exports of products manufactured abroad that contain Chinese-origin rare earth materials representing more than 0.1% of their total value per independently usable unit.

- Expanded Scope: The controls now cover not only the materials themselves but also upstream and downstream machinery, auxiliary chemicals, and technologies used in processing, refining, and applying rare earths. This move aims to solidify China’s rare earth technological advantage.

Trump’s Response: The Tariff Bomb and Negotiation Stance

In retaliation, President Trump announced massive punitive tariffs, escalating the U.S.-China trade war.

- Tariff Hike: The U.S. will impose an additional 100% tariff on Chinese products. This raises the overall tariff rate on Chinese imports to about 130% starting November 1, 2025, nearly reaching the 145% level mentioned earlier in the year. This represents a significant tariff escalation.

- The Negotiation Window: This aggressive escalation is widely viewed as a power play for dominance ahead of the APEC summit scheduled for October 31st. With the U.S. tariffs taking effect on November 1st and China’s export controls starting November 8th, markets anticipate that a U.S.-China agreement is highly likely either before or during the Gyeongju summit. Trump is under intense pressure to negotiate due to severe rare earth supply issues impacting American industries.

The New Tariff Trap: Rare Earths, Forced Investment, & Gold’s Rise – Global Economic Forecast 2025-2035

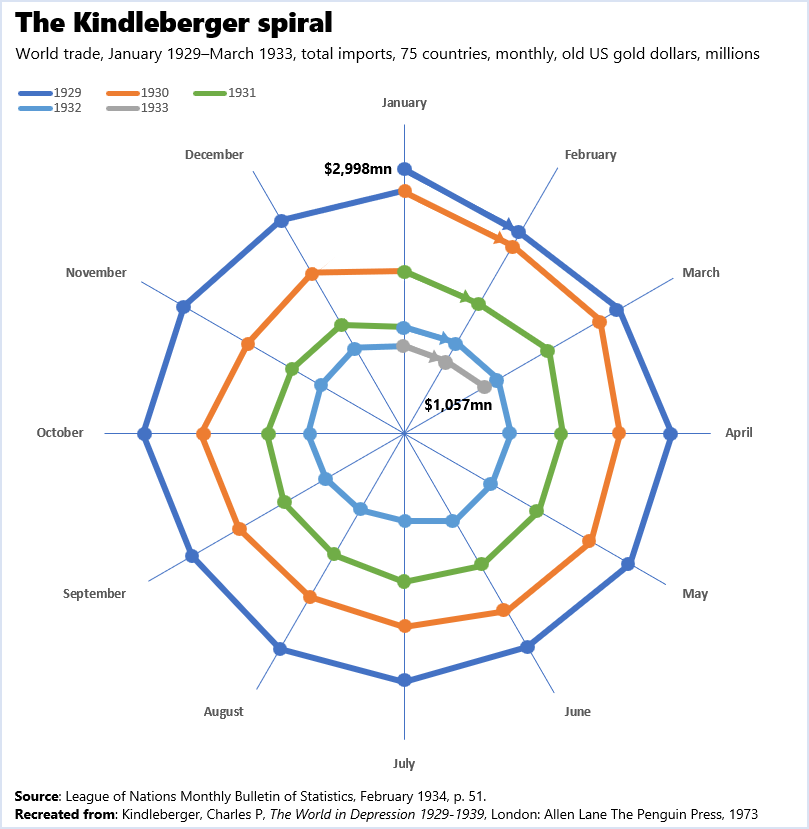

The escalation of these trade disputes raises the unsettling specter of the 1930s, a period famously analyzed by economic historian Charles Kindleberger, warning of a potential global trade collapse.

Historical Parallel: Smoot-Hawley’s Cautionary Lesson

The Smoot-Hawley Tariff Act of 1930 serves as the ultimate cautionary tale in trade policy. Global trade volume, which grew at an average annual rate of 6% in the mid-1920s, plummeted to one-third of its previous level due to multilateral retaliatory tariffs.

- The Trade Spiral: The U.S. average tariff rose from 40% to 60%, triggering widespread European retaliation. The resulting high mutual tariffs severely shrank global trade, which in turn deepened economic slowdown across countries—a phenomenon known as the “Kindleberger Vortex.”

The Current Reality: Stagnation vs. Collapse

Fortunately, the current situation has not yet spiraled into a 1930s-style collapse, offering a glimmer of hope amidst trade protectionism.

- Limited Retaliation: So far, U.S. tariff impositions have not led to a widespread decrease in global trade volume. This is partly because many nations have, to date, largely acceded to U.S. tariffs rather than engaging in a full-blown “chicken game” of reciprocal retaliation.

- The Risk of the Vortex: However, China’s direct and defensive retaliatory export controls pose a significant new threat to global supply chains. If other countries follow suit and the pattern of reciprocal retaliation expands, the result could be a significant decline in global trade and a global growth slowdown.

- Challenge to Hegemony: The aggressive U.S. policy, which now includes demanding direct investment, risks eroding non-U.S. countries’ trust in American leadership. This may encourage challenges to U.S. hegemony, echoing the argument that the Great Depression was fundamentally caused by the absence of effective global economic leadership.

Part III: Trump’s Investment Mandate and the U.S. Bond Paradox

President Trump is exerting pressure on major countries with large trade surpluses to reinvest those profits directly into the American economy. This is his stated strategy to address the trade imbalance and boost U.S. growth, believing it’s more beneficial than simply demanding currency appreciation. This approach creates significant U.S. trade policy risks.

The Forced Investment Mechanism and Ally Exposure

The U.S. is demanding that trade surplus countries invest their dollar proceeds back into the U.S., with 90% of the resulting profits then being mandatorily reinvested in America. This represents a new form of economic leverage.

- Japan’s Pledge: Japan has already agreed to a massive $550 billion investment pledge.

- South Korea’s Dilemma: The U.S. demanded $350 billion from South Korea—a highly problematic figure given South Korea’s total foreign exchange reserves stood at around $422 billion as of September 2025. This implies a demand to liquidate a substantial portion of its reserve assets, posing a significant South Korea FX reserves challenge.

- Taiwan’s Position: While no official public demand was listed in the file, Taiwan’s reserves are approximately $600 billion, placing it in a similar vulnerable position.

- Negotiation Disadvantage: Japan’s compliance has significantly disadvantaged countries like South Korea and Taiwan in subsequent negotiations, forcing them into difficult positions regarding foreign reserve management.

Pressure on the U.S. Bond Market: An Unintended Consequence

The forced investment mandate creates an acute market paradox: Trump’s policies, intended to strengthen the U.S. economy, will ironically lead to upward pressure on U.S. Treasury yields, creating U.S. bond market volatility.

- Reserve Composition: Dollar reserve assets held globally are predominantly invested in U.S. Treasuries (and Mortgage-Backed Securities – MBS), with long-term debt overwhelmingly dominating short-term debt. This highlights the scale of potential Treasury market disruption.

- The Selling Risk: Forcing these countries to liquidate their U.S. Treasury holdings to fund direct investments will trigger significant selling pressure on U.S. Treasuries, leading to weakness in the bond market and potentially higher interest rates.

- The Twin Deficits: The U.S. is attempting to reduce its trade deficit without concurrently reducing its substantial fiscal deficit. This process, coupled with forced disinvestment from Treasuries by surplus countries, makes it harder for other nations to finance the U.S. fiscal deficit. The strength of this upward pressure on U.S. Treasury yields will directly correlate with the aggressiveness of Trump’s enforcement, impacting U.S. fiscal sustainability.

Part IV: The Global Shift to Hard Money – Gold’s Resurgence

The combined effect of aggressive tariffs, demands for “economic capture,” and the resulting upward pressure on U.S. Treasury yields is a sharp decline in global trust in the U.S. dollar (often referred to as “soft money”) as the primary reserve asset. This trend accelerates de-dollarization efforts.

The Rise of Gold (Hard Money) as a Secure Asset

Central banks globally are increasingly seeking a store of value that is not subject to the political whims of the U.S. administration. This fundamental shift unequivocally favors gold (“hard money”) as the preferred safe-haven asset.

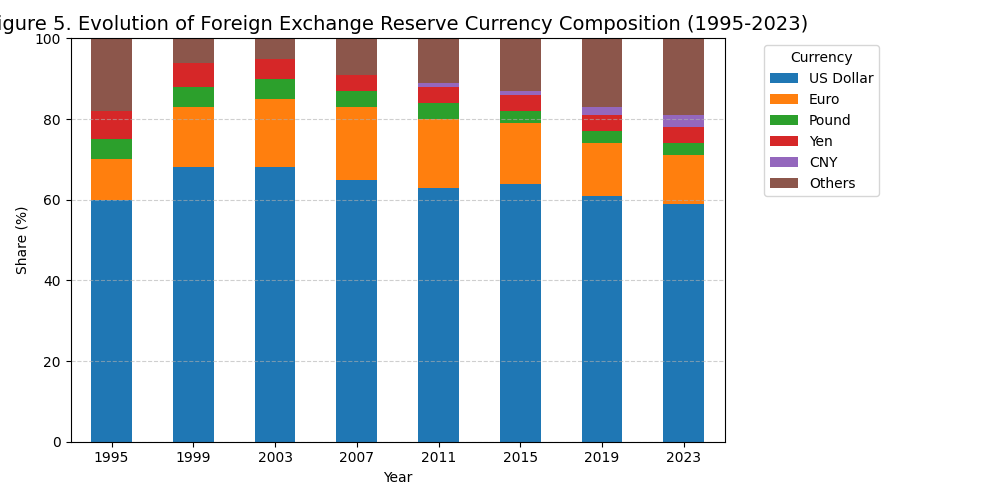

- De-Dollarization Trend: The share of the U.S. dollar in global foreign exchange reserves has been in a gradual, yet persistent, decline since the mid-1990s.

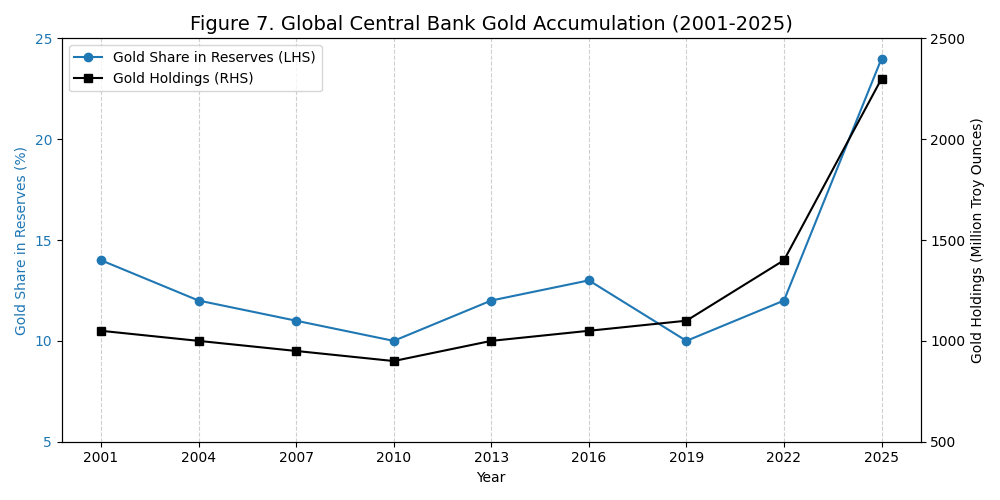

- Central Bank Gold Buying: The gold purchasing trend, notably led by China and other emerging economies, has accelerated significantly since the Russia-Ukraine war. Central bank gold buying in 2025 has remained near record highs, driven by the critical need for sanctions resilience, portfolio diversification, and rising geopolitical uncertainty.

- Increased Holdings: As seen in Figure 7 (referencing the original report), the volume of gold held by central banks (in million troy ounces) has been steadily increasing, and the ratio of gold in total foreign exchange reserves has shown a notable uptick in recent years. Gold is increasingly seen as the best way to store value without being subject to U.S. policy or potential financial weaponization. This underlines the growing importance of central bank gold reserves.

Part V: Futuristic Predictions (2030-2035) – Reshaping Global Finance

The current crisis marks a pivotal moment that will fundamentally define the shape of global finance and trade by the next decade, leading to significant global economic shifts.

Prediction 1: The Bifurcated Trade and Investment Bloc

By 2030, the global economy will have solidified into two primary, loosely coupled trade and investment blocs, fundamentally altering international trade relations.

- The American Bloc (Managed Trade): Trade within this bloc will be increasingly governed by Managed Trade Agreements, demanding local content and mandatory reinvestment. This ensures political compliance but significantly reduces supply chain efficiency, contributing to structural inflation within the U.S. economy. This could define future U.S. trade policy.

- The Eurasian Bloc (Resource/Technology Exchange): Centered around China, this bloc will consolidate its position by leveraging its dominant control over rare earths and critical battery inputs. This bloc will increasingly rely on non-dollar trade settlement (e.g., yuan, commodity-backed currencies) in exchange for cheap infrastructure and technology, further accelerating the de-dollarization of the commodity trade. This highlights China’s economic influence.

Prediction 2: A Persistent U.S. Bond Market Premium

The fundamental trade-off created by the Trump mandate—cutting the trade deficit while refusing to cut the fiscal deficit—will translate into a permanent risk premium on U.S. long-term Treasury yields by 2030. This will result in structurally higher U.S. interest rates.

- Unreliable Foreign Demand: Foreign demand for U.S. debt, once the dependable stabilizer, will become unreliable, forcing domestic institutions to absorb a larger share of the massive U.S. debt load.

- Elevated Yields: U.S. 10-year Treasury yields will trade structurally higher than historical averages, reflecting the geopolitical risk of the “Dollar Trap” and the diminished global trust in U.S. financial integrity. This signifies long-term U.S. debt challenges.

Prediction 3: Gold as the De Facto Neutral Reserve Asset

By 2035, while the dollar will technically remain the most-held reserve currency, its functional dominance in cross-border trade settlement will be severely eroded. This solidifies gold’s role in the global financial system.

- Increased Gold Holdings: Central banks will have collectively increased their gold holdings to well over 20% of total reserves, cementing gold as the true neutral store of value and a vital counterweight to geopolitical risk.

- Non-G7 Gold Usage: Non-G7 countries will increasingly use gold as collateral and settlement for bilateral trade, reflecting the growing desire to reduce dependence on Western currencies amid rising uncertainties.

- Gold Price Surge: The average gold price could approach or exceed $4,000 per ounce by late 2025/2026, driven by this structural institutional demand for gold investment.

https://www.reuters.com/world/china/china-tightens-rare-earth-export-controls-2025-10-09

https://mgiedit.org/obbba-the-us-economys-new-path-in-2025-a-deep-dive/

답글 남기기