In the analytical rigor of global finance, we frequently obsess over the sweeping trajectories of GDP, fiscal deficits, and corporate earnings. Yet, the most diagnostic leading indicator of a nation’s systemic resilience is found far from the trading floor, residing instead in the granular, often painstaking bookkeeping of its citizens. The Household’s Total Income and Expenditure is not merely a record of domestic utility bills; it is the existential equivalent of a corporate Profit and Loss (P&L) statement for the private individual.

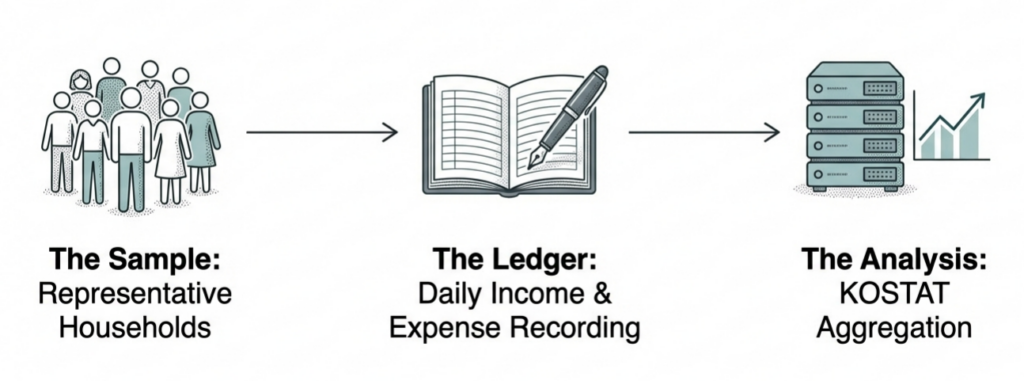

The methodology behind these figures warrants a level of institutional respect often reserved for central bank balance sheets. In jurisdictions like South Korea, the National Statistical Office (KOSTAT) meticulously distributes physical and digital “household ledgers” to a representative sample of the population. This “boots-on-the-ground” data collection—requiring households to manually record every inflow and outflow—lays bare the actual financial state of the nation. For the institutional investor, these ledgers provide a “health check-up” that predicts the vitality of the internal consumption engine. To ignore the micro-solvency of the household is to ignore the primary source of liquidity and the ultimate destination of all economic shocks.

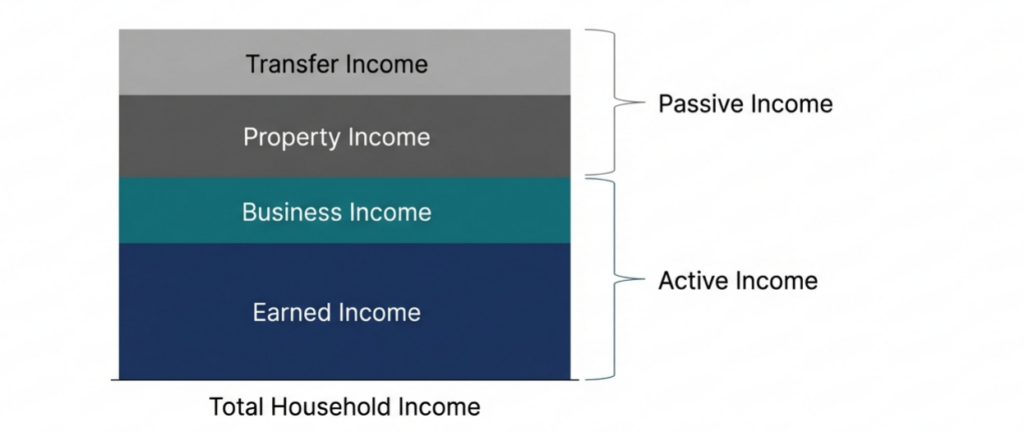

The Four Pillars of Revenue: Deconstructing Household Income Streams

The stability of a nation’s social contract is dictated not by the nominal volume of income, but by its structural composition. Economic volatility does not strike all revenues equally; therefore, we must evaluate the “Macro Sensitivity” of the four revenue pillars that sustain the modern household.

• Earned Income (Labor-Derived Yields): Comprising wages and bonuses, this is the primary liquidity source for the majority. It is the most sensitive to labor market tightening and the broader corporate credit cycle.

• Business Income: This encompasses profits from self-employment and independent contracting. Crucially, as the source context highlights, this includes primary industries such as agriculture and forestry. A contraction here often signals a shift from traditional industrial structures toward a more precarious gig economy.

• Property Income (Capital Asset Returns): Including interest, dividends, and rental yields, this pillar links the household directly to capital market performance. In an era of high volatility, it represents the household’s exposure to the “wealth effect” or its absence.

• Transfer Income: To understand a household’s true resilience, we must distinguish between Unrequited Public Transfers (state-funded pensions, child allowances, and social subsidies) and Private Transfers (inter-generational support, such as children providing for elderly parents). While the former reflects fiscal health and the robustness of the social safety net, the latter reveals the informal economic buffers within a culture.

A shift in the ratio between these pillars—for instance, a rising reliance on public transfers—can signal a demographic calcification or a labor market in distress, long before such trends manifest in headline GDP.

The Expenditure Architecture: Analyzing Essential Outlays and Inflationary Pressure

Expenditure patterns reveal the true “inflationary tax” levied on the middle class. When non-discretionary costs rise, they do not merely increase the cost of living; they erode the household’s ability to participate in the broader economy, triggering a classic “Income Effect” where total consumption must contract to accommodate essential survival.

| Expenditure Category | Classification | Macro-Economic Trigger |

|---|---|---|

| Food & Groceries | Non-Discretionary | Commodity Price Indices (CRB) |

| Housing (Rent/Maintenance) | Non-Discretionary | Yield Curve Movements & Real Estate Volatility |

| Utilities (Water, Light, Heat) | Non-Discretionary | Global Energy Volatility & Imported Inflation |

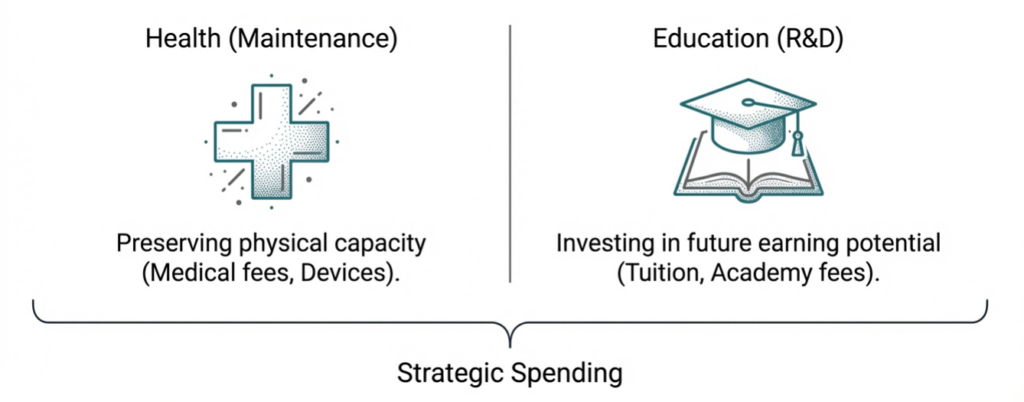

| Health (Medical/Medicine) | Essential Maintenance | Silver Economy Demographics & Policy Shifts |

| Education (Tuition/Academies) | Human Capital Investment | Wage Polarization & Credential Inflation |

The surge in Utilities, often driven by global energy supply chain disruptions, acts as a de facto regressive tax. Furthermore, while Education is categorized here as a “Human Capital Investment,” its rising cost in competitive markets represents a significant drain on short-term liquidity, potentially trading future productivity for current financial fragility.

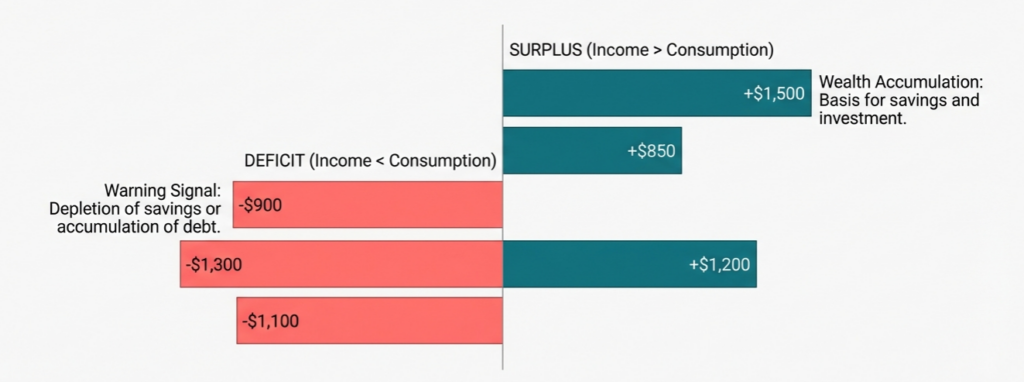

The Surplus-Deficit Binary: Systemic Implications of Household Solvency

The subtraction of expenditures from income results in a binary state that dictates the national credit cycle: the surplus or the deficit.

• The Household Surplus: This is the prerequisite for financial stability. These “surplus funds” are the primary source of liquidity for the banking system. They fuel the deposit base and the equity markets. When surpluses are robust, the domestic investment pool is deep.

• The Household Deficit: A persistent deficit signals that a household is liquidating assets or, more dangerously, engaging in debt-financed consumption.

From a systemic perspective, a widening household deficit is the harbinger of a “deleveraging cycle.” When high macro interest rates intersect with a deficit-ridden populace, the risk of Non-Performing Loans (NPLs) escalates. For the banking sector, this threatens CET1 ratios and creates a feedback loop where credit tightening further suffocates the household, leading to a paralysis of the domestic credit market.

Macro-Geopolitical Convergence: The Global Impact on the Kitchen Table

The household ledger is the final destination for every geopolitical tremor. Global supply chain disruptions do not remain abstract concepts; they manifest as “imported inflation,” directly spiking the Utility and Food costs recorded in the physical ledgers of representative households.

The feedback loop is most visible in monetary policy. When the US Federal Reserve aggressively hikes rates, the resulting interest rate differentials often force domestic central banks to follow suit to protect the currency. This immediately dictates the Property Income (yields) and the Housing/Interest costs of the local household. Consequently, a decision made in Washington D.C. can be the direct catalyst that tips a household in Seoul or London from a state of surplus into a systemic deficit.

Conclusion: Outlook and Strategic Imperatives for Investors

The household ledger is a mirror reflecting the current financial state of the nation. As we navigate an era of persistent inflationary pressure and geopolitical fragmentation, the ability of the household to maintain its “surplus” will be the ultimate determinant of market stability. Investors should monitor the quarterly releases from the National Statistical Office with the same intensity usually reserved for earnings season.

Investor Takeaways:

• Monitor Solvency and NPL Risk: A narrowing household surplus (잉여 자금) is a leading indicator for rising equity risk premiums and potential instability in the banking sector’s asset quality.

• The Consumption Pivot: Rising costs in non-discretionary categories—specifically Utilities and Housing—act as an early warning for a sharp contraction in consumer discretionary valuations.

• Income Structural Analysis: Evaluate the ratio of Earned to Transfer income; an increasing reliance on public transfers signals a fragility in the labor market that may necessitate fiscal intervention, impacting national sovereign risk.

In the sophisticated world of macro-investing, “Micro-Awareness” is not an elective; it is a prerequisite. The household ledger is the bedrock upon which the entire edifice of national economic health is built.

답글 남기기