The Architecture of Hegemony: Why Currency Dominance Defies Global Volatility – The history of international trade is a chronicle of successive currency hegemonies, a relay race where the baton of global liquidity passes from the Dutch florin to the British pound sterling, and eventually to the U.S. dollar. In the contemporary era, the greenback occupies what Abadi et al. (2026) define as a unipolar equilibrium—a state where a single medium of exchange dominates the global landscape. While the Bretton Woods agreement is often cited as the dollar’s birth certificate as a hegemon, such diplomatic arrangements are merely the surface of a much deeper economic sea.

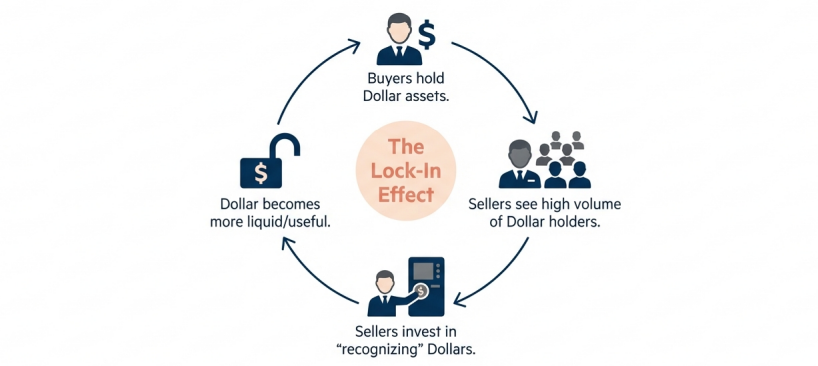

The reality of International Currency Dominance is that it is driven by profound strategic complementarities and economic fundamentals that create immense structural inertia. Dominance is not a fragile consensus easily shattered by a single election or a localized crisis; it is an equilibrium maintained by the collective expectations of millions of disparate agents. Once a standard is established, it is exceptionally difficult to dethrone, persisting through decades of volatility due to the self-reinforcing nature of global liquidity.

The Micro-Foundations of Liquidity: Why Sellers Accept the Greenback

To understand why the dollar persists, one must look at the decentralized market where buyers and sellers meet. Here, terms of trade are determined through a Nash bargaining protocol, where the relative value of a currency is weighed against the seller’s cost of production. A seller’s willingness to accept a foreign currency is not a political statement but a calculation of future utility. This creates a two-way complementarity: buyers hold a currency because they expect sellers to accept it, and sellers accept it because they know buyers hold it.

Central to this calculus is the liquidity premium—the convenience yield agents pay for holding a liquid asset instead of an illiquid debt. In the current market, research by Diamond and van Tassel (2025) suggests this yield sits at approximately 30bp for dollar-denominated assets. The demand for such a currency is distilled into three primary drivers:

• Country Size: Larger economies enjoy a natural advantage. Foreign agents anticipate a higher frequency of trade with a large domestic market, which mechanically increases the utility of holding that country’s debt.

• Monetary Policy Credibility: For a currency to remain attractive, a government must possess the fiscal capacity to back its debt with taxes rather than relying on seigniorage. When a state prints money to cover its interest bill, it erodes the real return, destroying the liquidity premium.

• Network Externalities (Acceptability): As a currency’s recognizability grows, its marginal benefit as a settlement tool increases exponentially, reinforcing its status as the default option.

Even the smallest frictions, such as the Administrative Cost (kappa), play a pivotal role. These costs—representing the overhead of hiring staff to manage currency exposures, compliance costs, and legal tender restrictions—are remarkably small, often just a few basis points. However, even these minute costs are enough to prevent the emergence of a “classical” diversified regime. Agents would rather settle in a single, well-understood currency than incur the overhead of managing a basket of foreign alternatives.

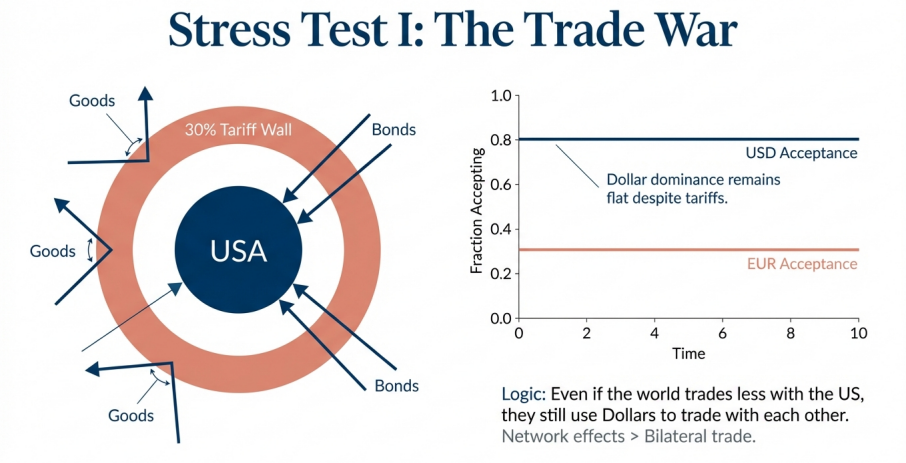

Resilience Under Fire: The Trade War Counterfactual

A persistent fear in international political economy is that trade protectionism will inevitably lead to the decline of the dollar. However, a general equilibrium simulation of a permanent “Trade War”—calibrated with a 30% tariff on U.S. imports and reciprocal retaliation—suggests that the dollar’s status is far more resilient than commonly assumed.

| Traditional Assumptions | Model Findings |

|---|---|

| Trade protectionism weakens currency status by reducing the U.S. share of global transaction volume. | Network externalities allow the dollar to persist as a settlement tool between third-party regions (e.g., Europe and the Rest of the World) even as direct trade with the U.S. declines. |

| Reduced economic integration leads to immediate multipolarity. | History dependence and the established payment infrastructure ensure that the dollar remains the “least-cost” settlement tool despite macro-shocks. |

This resilience is bolstered by the exorbitant privilege of the dominant issuer. While this privilege allows a large economy to sustain trade deficits by capturing seigniorage and liquidity premia from foreign agents, it is not an unlimited check. The model estimates this benefit is capped at approximately 0.25% of GDP. Curiously, the research indicates that even if the dollar were to lose its dominance, the real effects on global trade would be remarkably modest, suggesting the system is optimized for stability over sensitivity to the hegemon’s trade balance.

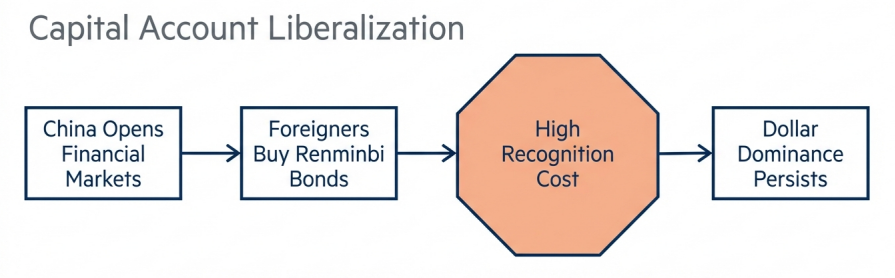

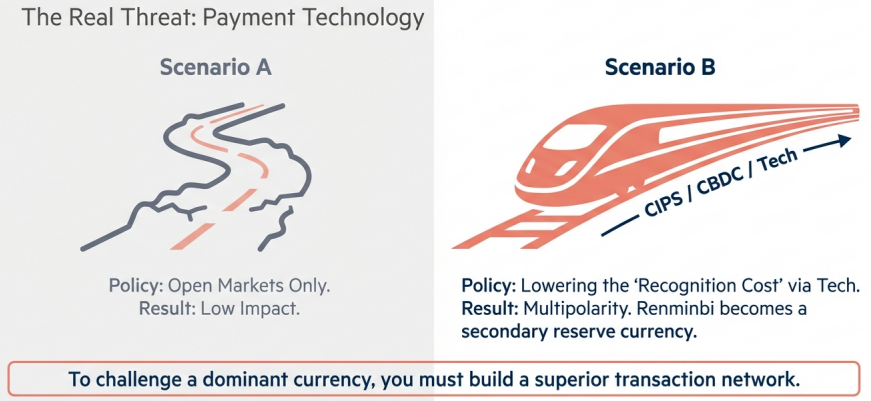

The Challenger’s Playbook: Can the Renminbi Disrupt the Status Quo?

The “Fiscal version of the Triffin Dilemma” poses a long-term threat: as the global economy grows, the U.S. may eventually lack the fiscal capacity to supply enough safe, liquid assets to satisfy global demand. This creates an opening for a challenger, but the path to disruption is steep. For a currency like the renminbi, two distinct strategies emerge:

Strategy A: Expanding Payment Networks (Matching Technology). This involves the development of infrastructure like the Cross-Border Interbank Payment System (CIPS). While improving matching technology increases the renminbi’s utility in trade settlement, the model suggests this only cements its status as a secondary international currency. It becomes a tool for specific corridors, but fails to rival the dollar’s global reserve share.

Strategy B: Shifting the Bond Supply Curve. To truly rival the dollar, a challenger must compete in the bond market. This requires halving the liquidity premium and massively expanding the supply of high-quality sovereign debt. This is significantly more difficult than building payment rails; it requires a massive expansion of fiscal capacity and the ability to tax domestic agents to support the interest burden—a high bar for any emerging economy.

Conclusion: Strategic Implications for Global Investors

The international monetary system is characterized by a high degree of history dependence. Transitions between hegemonies are not instantaneous; they have a half-life of about 7 years, meaning that even after the fundamental drivers of a shift are in place, the old standard lingers. For institutional investors and policymakers, the implications are clear:

1. Inertia is the Baseline: The dollar-based settlement system is not a house of cards. Dominant-currency equilibria are fundamentally stable and resistant to anything short of a massive, structural fiscal shock.

2. The Dominance of Scale: Large economies maintain a natural advantage in the liquidity race. Their sheer volume of trade creates a gravitational pull that can overcome even a relatively high liquidity premium on their debt.

3. Portfolio Stickiness: Portfolio allocations in international reserves are unlikely to shift based on marginal changes in U.S. interest rates. The “stickiness” of the dollar is a product of a global coordination game where the cost of switching is nearly always higher than the cost of remaining.

Ultimately, the architecture of hegemony is built on the fact that currency dominance is a self-fulfilling prophecy. As long as the U.S. maintains its monetary policy credibility and its scale, the greenback will remain the bedrock of global finance, defying the volatility of trade wars and shifting geopolitical winds.

https://mgiedit.org/the-warsh-shock-and-the-re-rating-of-market-risk/

https://www.sciencedirect.com/science/article/pii/S2667111525000210

답글 남기기