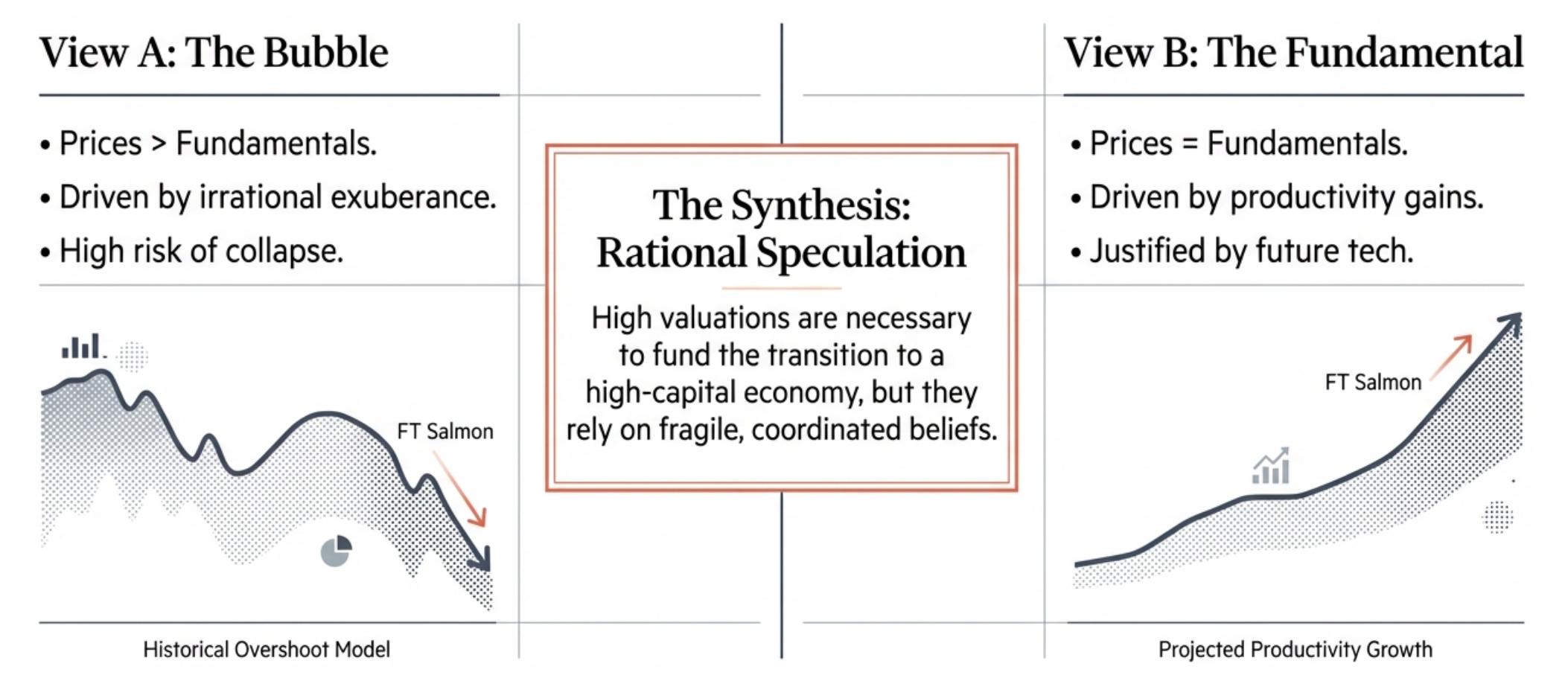

The AI Paradox: Rational Exuberance and the Fragility of Speculative Growth – In the gilded corridors of global finance, the debate surrounding Artificial Intelligence (AI) valuations has largely devolved into a binary polemic. On one side, fundamentalists argue that current market premiums are the logical reflection of a transformative technological paradigm; on the other, skeptics identify the hallmarks of a classic, irrational bubble.

However, Ricardo J. Caballero’s recent thesis offers a sobering riposte to this simplistic dichotomy. By framing the current era as one of “speculative growth,” we find that elevated valuations may be fundamentally justified—indeed, even necessary—to reach a high-growth destination, yet they remain inherently precarious. This duality suggests that the AI era is not a choice between value and delusion, but a fragile equilibrium of coordinated optimism.

The Technology Pillar: AI as “Labor-Like” Capital

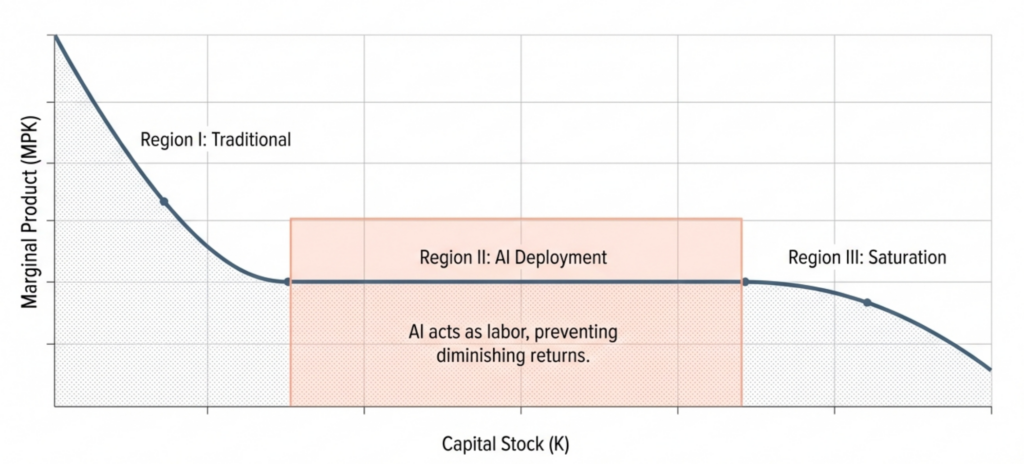

At the core of this macro-financial narrative is a profound shift in the neoclassical production function. Traditional capital is subject to the gravity of diminishing returns: as one adds more machines to a fixed pool of workers, the marginal productivity of those machines inevitably falls. AI breaks this cycle by acting as “labor-like” capital. By substituting for human labor across discrete tasks, AI does not merely augment the workforce; it expands the “effective labor” supply (N).

This expansion creates a unique “Three-Region” Marginal Product of Capital (MPK) schedule. In the crucial deployment phase, AI adds effective labor at a rate that keeps the capital-to-effective-labor ratio stable, thereby forestalling the usual decline in returns.

| Phase | Region | Technological Characteristic | Marginal Product of Capital (MPK) |

|---|---|---|---|

| I. Pre-AI | No AI | Standard capital accumulation | Declining (Diminishing Returns) |

| II. Deployment | The Flat Region | AI expands effective labor (N) | Constant (Returns Stabilized) |

| III. Saturation | Capacity met | AI reaches limits (Ksat) | Resumption of Diminishing Returns |

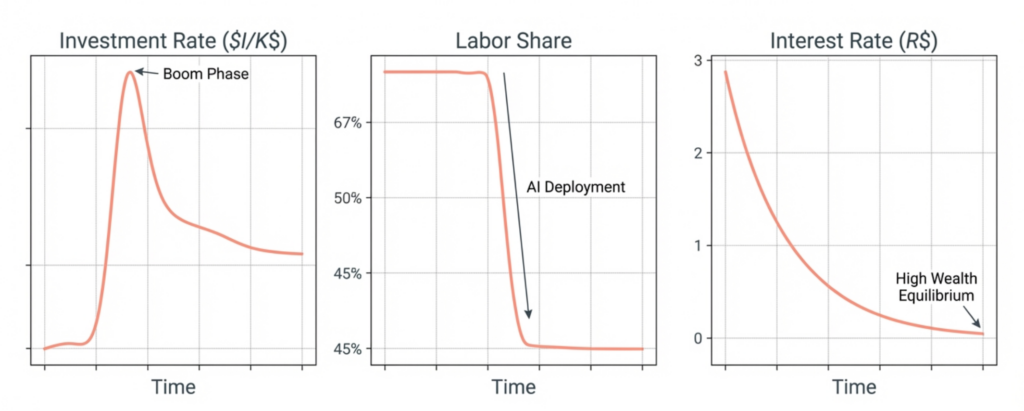

The strategic significance of Region II—the “Flat MPK Region”—cannot be overstated. By preventing the immediate penalty of falling marginal products, it provides the runway necessary for an aggressive expansion of the capital stock. However, for this technological potential to translate into a macroeconomic transition, it requires a specific “Goldilocks” environment of Intermediate Adjustment Costs. If costs are too low, valuations never rise enough to spark a boom; if too high, the required valuations become mathematically implausible. Within the intermediate range (ψ), however, elevated valuations become the essential engine of capital accumulation.

The Funding Feedback: Wealth Concentration as a Feature

The AI transition does more than alter production; it reshapes the flow of global capital through a “Funding Feedback” loop. As AI technology deploys, it generates a sharp Labor Share Compression. According to Caballero’s calibration, the human labor share of income (sL) falls from a baseline of approximately 0.67 to a mere 0.46.

This shift of income toward capitalists activates the mechanism of non-homothetic preferences. As wealth (W) concentrates at the top, the aggregate saving rate rises—wealthier individuals save a larger fraction of their income. This surge in savings systematically drives down the required return (R), creating a virtuous cycle:

1. Capital Concentration: Higher capitalist wealth leads to increased savings.

2. Lower Required Return: Excess savings drive down the required rental rate of capital.

3. Asset Appreciation: A lower R justifies higher asset prices (q), which in turn increases capitalist wealth.

In this regime, wealth concentration is not merely a social byproduct; it is a feature of the financing mechanism that sustains high asset valuations and funds the transition.

The Geometry of Growth: Multiple Equilibria and Tobin’s q

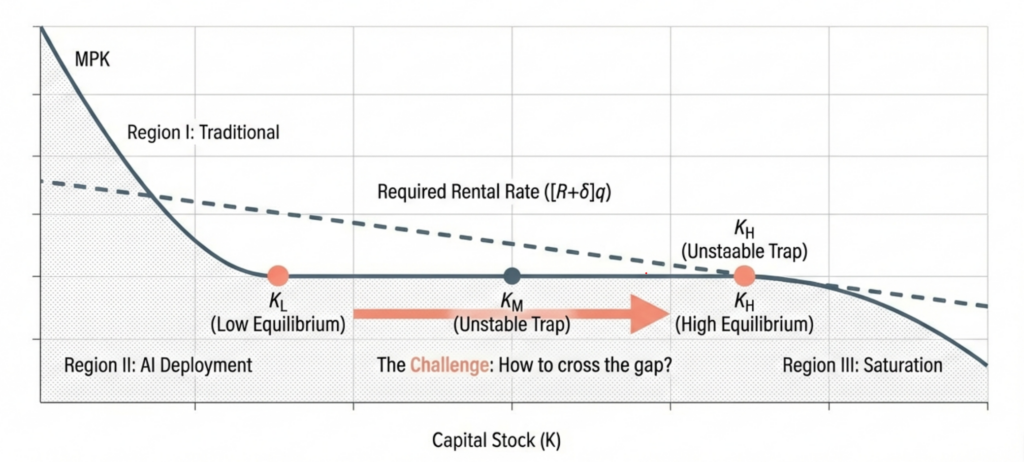

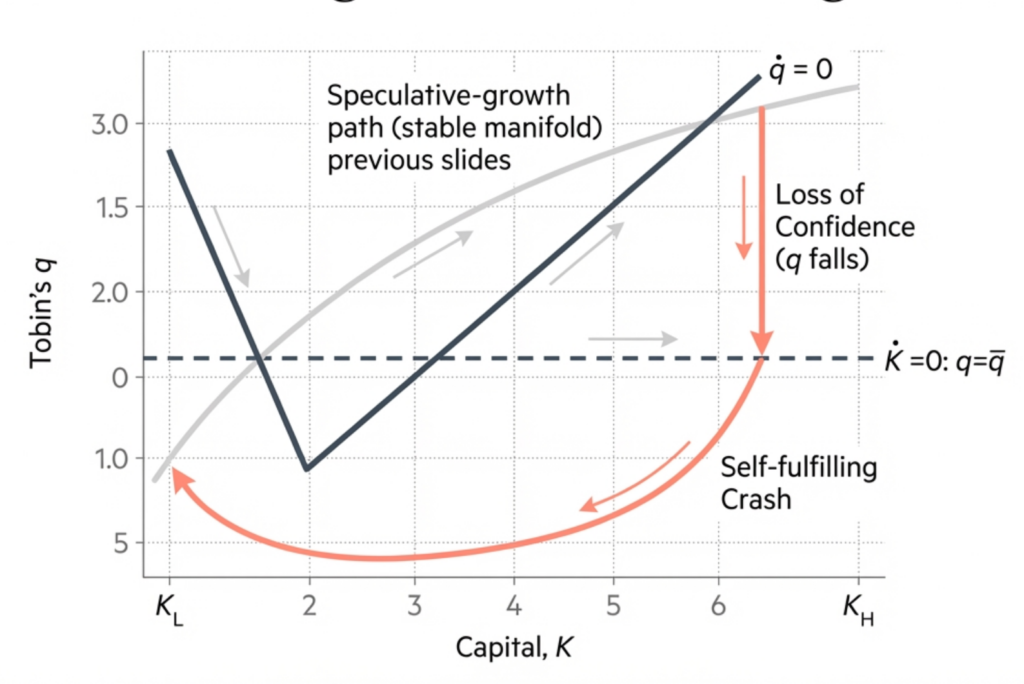

The intersection of the “down-flat-down” MPK curve and the falling required return curve reveals a manifold of multiple potential steady states. The global economy is essentially caught between two stable destinations:

• Low-Capital Equilibrium (KL≈0.224): A state of low AI adoption, high required returns, and lower aggregate wealth.

• High-Capital Equilibrium (KH≈0.790): A state where AI is fully integrated, the capital stock is massive, and required returns are permanently lower.

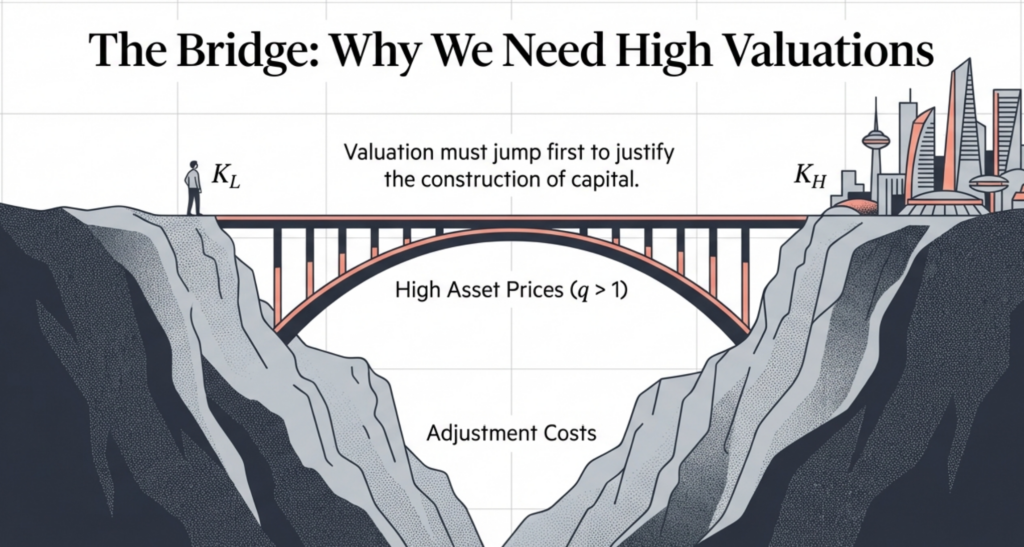

The bridge between these states is Tobin’s q—the ratio of market value to replacement cost. For the economy to escape the KL trap and move toward KH, valuations must jump above the steady-state level of qˉ≈1.0168. High valuations are the equilibrium mechanism; they provide the financial incentive for firms to invest at the breakneck speeds required to reach the high-capital frontier. Without this “speculative” premium, the transition simply never begins.

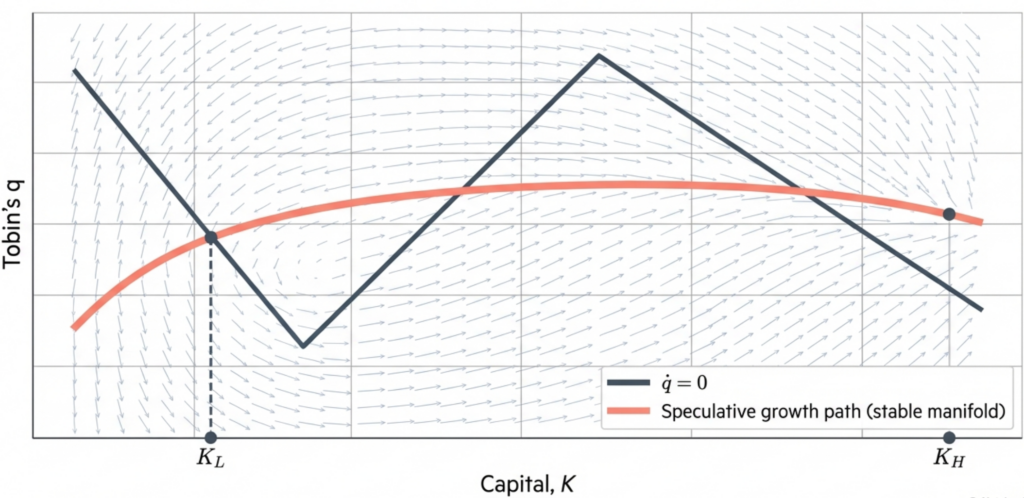

Fragility and the Anatomy of a Self-Fulfilling Crash

While the speculative-growth path is rational, it is profoundly fragile, depending entirely on “coordinated optimism.” Because there is an unstable middle equilibrium (KM), the economy’s destination is path-dependent. If market participants suddenly lose faith—whether due to disappointing data or a simple shift in sentiment—the economy can experience a discrete downward jump in valuations.

This “Crash Path” is a self-fulfilling prophecy. A drop in q removes the incentive to invest, capital accumulation reverses, and the resulting economic slowdown validates the initial pessimism. The transition is marked by three primary risks:

1. Dependence on Sentiment: The high-growth outcome requires the persistent maintenance of optimistic beliefs across the entire transition manifold.

2. Labor Share Compression: While absolute wages eventually grow with capital deepening, the collapse of the labor share (from 0.67 to 0.46) creates significant structural and socio-political drag.

3. Investment Reversal: A downward revision in valuations is not a mere market correction; it is a fundamental shift in the economy’s trajectory back toward the low-capital state.

Strategic Implications for the Professional Investor

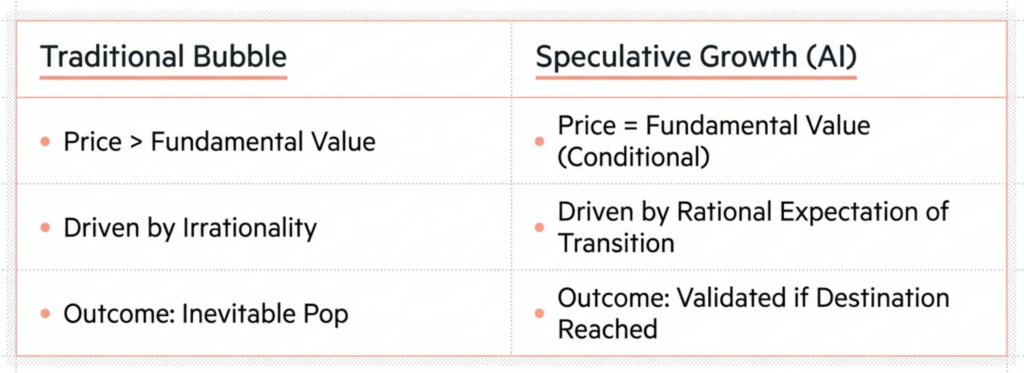

For the institutional allocator, the strategic “So What?” is clear: labeling AI as a bubble is a category error that misses the interdependence of valuation and reality. In a speculative-growth regime, momentum is fundamental. The very “exuberance” that critics decry is the catalyst that lowers the cost of capital and facilitates the leap to a higher productivity steady state.

However, the professional investor must recognize that in this new macroeconomy, the “growth” and the “bubble” are two sides of the same coin. The greatest systemic risk is not that valuations are high relative to historical norms, but that the coordinated optimism required to sustain the transition is inherently volatile. In an AI-driven economy, a valuation-based sell signal is often a regime-collapse signal. We are navigating a path where the destination is magnificent, but the bridge is built of nothing more—and nothing less—than the durability of our collective expectations.

답글 남기기