Takaichi’s Win: Will the New Abenomics Break the Yen Carry Trade? (Inflation & Debt Risk) – The unexpected election of Takaichi Sanae as the new president of Japan’s ruling Liberal Democratic Party (LDP) has sent a palpable tremor across global financial markets. Markets, braced for a more moderate outcome, have instead been confronted with the prospect of a political figure deeply committed to the principles of Abenomics, the large-scale economic stimulus program initiated by the late Prime Minister Shinzo Abe. Takaichi, considered the most conservative candidate among the contenders, is widely expected to secure the position of Prime Minister in the upcoming Diet vote. Her commitment to a bold economic policy—dubbed the “three arrows” of daring monetary policy, swift fiscal policy, and a new growth strategy—signals an impending large-scale economic stimulus package.

This political surprise has not merely caused a ripple; it has created a surge of market volatility. Immediately following the election, Japanese stock prices surged, the yen depreciated rapidly, and Japanese government bond (JGB) yields rose significantly, particularly on long-term bonds. Crucially, the Dollar-Yen exchange rate surged to its highest level in eight months, reaching the ¥152 per dollar mark, which is a key trigger for speculation about a revived Yen Carry Trade. The market is now anticipating that Japan will once again become a major supplier of global liquidity, leveraging its weak yen and continued ultra-low interest rate policy.

However, this rush of enthusiasm, this return to a familiar narrative of “easy yen” funding, must be approached with caution. The economic landscape Takaichi inherits is fundamentally different from the one that greeted Abe in 2012. Two powerful and interlinked factors—high inflation and the chilling reality of an expanded government debt—now act as significant constraints on the unchecked flow of the Yen Carry Trade. This report delves into the details of Takaichi’s policy inheritance, analyzes the new constraints on the Yen Carry Trade, and projects the long-term implications for the Japanese economy and global financial stability.

The Abenomics Inheritance: A Commitment to Stimulus and a Low-Rate Pledge

Takaichi Sanae’s political ascendancy marks a definitive return to the reflationary doctrine of Abenomics. The core of this doctrine is the relentless pursuit of growth and the escape from decades of deflationary stagnation through aggressive intervention. Her promise to implement the “three arrows” suggests that the government will continue to exert political pressure on the Bank of Japan (BoJ) to maintain its ultra-accommodative monetary policy.

The Daring Arrow: Monetary Policy and the BoJ

The expectation of a continued weak yen and low-rate environment is predicated on the historical relationship between the Japanese government and the Bank of Japan, where the BoJ has consistently cooperated with the government in monetary policy. Takaichi herself has expressed a highly negative view toward interest rate hikes, signaling a continuation of the dovish stance that has been the cornerstone of Abenomics.

This is the key assumption fueling Yen Carry Trade speculation. The carry trade involves borrowing in the low-interest rate currency (the yen) and investing in higher-yielding assets abroad, profiting from the interest rate differential. As long as the rate differential remains wide, and the yen remains weak, the trade is profitable.

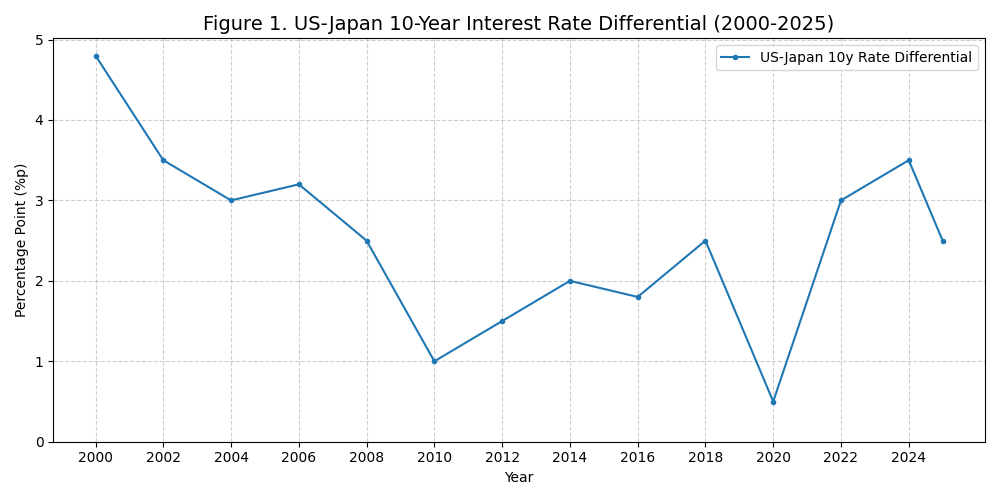

As illustrated in Figure 1, the US-Japan 10-year interest rate spread (US-Japan 10y Rate Differential) has recently narrowed, yet the structural difference remains considerable, tempting global investors. The market expects Takaichi’s administration to effectively delay any possibility of a BoJ exit from its easing policy.

The Swift Arrow: Fiscal Policy and Debt Expansion

Takaichi’s platform involves a swift and expansionary fiscal policy, which has further spooked the bond market and weakened the yen. Her campaign pledges include measures such as tax credits for vulnerable populations and direct cash handouts (coupons). The realization of these promises would require a significant increase in government borrowing and a further expansion of the fiscal deficit.

While these measures are designed to stimulate growth and help Japan “break away from low growth,” the bond market is reacting with heightened caution. This push for expanded government debt is a crucial counterpoint to the easy monetary policy, as it pushes up interest rates and introduces a new constraint on the Yen Carry Trade.

The New Constraints: Inflation and the Limits of Fiscal Health

The enthusiasm for a renewed Yen Carry Trade must be tempered by two structural shifts in the Japanese economy. The environment Takaichi inherits is fundamentally different, characterized by a higher level of inflation and a staggering load of government debt.

Constraint I: Stubbornly High Inflation and the Weak Yen Risk

The first major constraint is the persistent and excessively high level of inflation in Japan, which remains above the Bank of Japan’s target, even with a recent slowdown in price increases.

Current Inflation Level: Despite some stabilization (e.g., in rice prices), Japanese consumer prices are still excessively high compared to the past and remain above the BoJ’s target.

The Weak Yen Trap: A continuous depreciation of the yen (further Yen Carry Trade success) carries the significant risk of re-accelerating inflation. As a country heavily reliant on imports, a weaker yen directly translates into higher import costs.

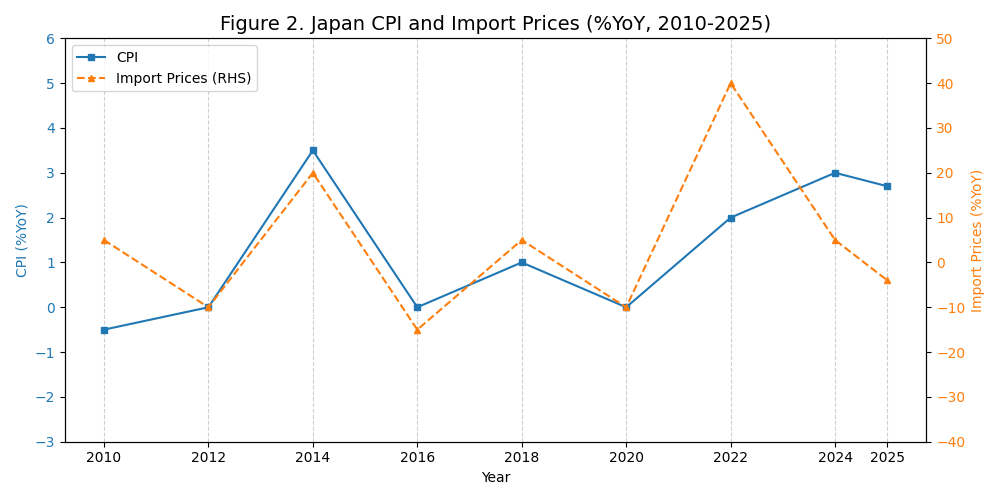

| Metric | Recent Trend (Figure 2, 2022-2025) | Implication |

| CPI | Rises sharply after 2022, sustaining above 2% | High initial inflation level increases sensitivity to further cost shocks. |

| Import Prices | Shows a sharp spike and rebound, closely preceding CPI rises | Demonstrates that a renewed weak yen (driving import prices) will inevitably lead to increased domestic price burdens. |

The core dilemma is that Japan lacks the substantial growth headroom to tolerate high inflation, unlike the United States. This requires greater caution regarding the exchange rate. If the yen’s depreciation becomes too rapid, the government may be forced to intervene or apply pressure on the BoJ, potentially limiting the expected lifespan of the Yen Carry Trade.

Constraint II: The Crushing Weight of Government Debt

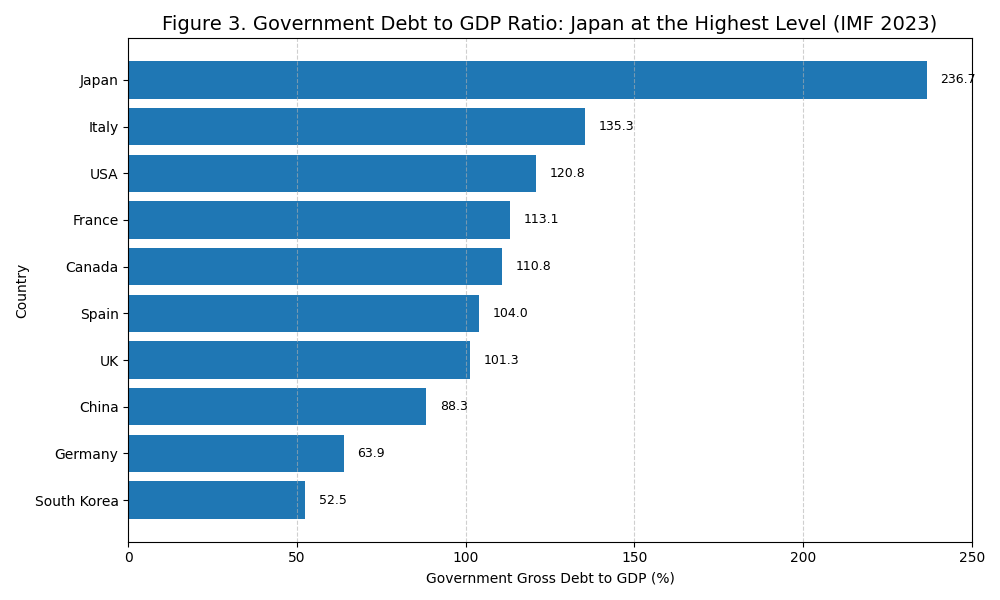

The second and perhaps more formidable constraint is Japan’s fiscal health. Japan’s government debt-to-GDP ratio is extraordinarily high, standing at approximately 250% of GDP.

Global Comparison: As shown in Figure 3, Japan’s debt-to-GDP ratio of 249.7% (as of 2023) is by far the highest among major countries listed, nearly double that of Italy (134.6%) and significantly exceeding the US (118.7%)

The policy priority of the new administration is to focus on escaping low growth over managing this massive debt. However, the commitment to expansionary fiscal measures will exacerbate the deficit, and the fear of debt expansion is already acting as an upward pressure on interest rates. If Takaichi’s ambitious spending plans materialize, the resulting higher long-term interest rates could significantly limit the profitability of the Yen Carry Trade. The market will increasingly view Japan’s policy as a high-stakes gamble.

The Global Implication: A Lowered Expectation for Liquidity

The market’s initial reaction, with the Dollar-Yen reaching ¥152 per dollar and JGB yields spiking, clearly indicates an anticipation of a significant restart of global liquidity through the Yen Carry Trade. However, the constraints of inflation and debt suggest that the “eyes should be lowered” on these expectations.

The new environment introduces a cap on the supply of cheap yen: the inflation risk puts a floor on how weak the yen can be, and the fiscal expansion pushes up long-term borrowing costs, eroding the carry. The Takaichi-era Yen Carry Trade will thus be more volatile and potentially shorter-lived, reflecting the high-wire act of the new “growth first” strategy.

Futuristic Projections: Japan’s Financial Structure in 2035

If the Takaichi administration successfully implements its Abenomics-inspired stimulus, the Japanese economy and its role in global finance could evolve into a radically different structure by 2035.

Prediction 1: Structural and Volatile Inflation

By 2035, Japan will have permanently shed its deflationary reputation. The massive, sustained fiscal and monetary stimulus will have successfully established an inflation floor. However, this inflation will be structural and volatile, constantly exposed to import price shocks due to the chronically weak yen. The government will have normalized the ¥150-170/USD range as “competitive” for exports, effectively accepting the inflationary cost to domestic consumers. The BoJ’s mandate will have informally shifted to prioritizing currency stability to manage import price inflation, leading to frequent, minor policy adjustments rather than a single, grand exit.

Prediction 2: The End of the Carry Trade as a Global Engine

The Japanese bond market (JGBs) will be fundamentally split into two segments by 2035:

- Short-Term Control: The BoJ will maintain an explicit or implicit cap on short-term JGB yields (2-year and below) to keep borrowing costs near zero, safeguarding the domestic banking system.

- Long-Term Liberalization: Long-term JGB yields (10-year and above) will trade at a high, structural premium. This premium will reflect the market’s assessment of Japan’s astronomical debt-to-GDP ratio (which may exceed 300% by 2035) and the relentless issuance of debt.

This high, structural yield on the long end will effectively kill the Yen Carry Trade as a dominant global liquidity engine. The rising cost of long-term yen borrowing will be too high to justify the carry, forcing global investors to seek funding elsewhere.

Prediction 3: Sovereign Debt Monetization and Financial Repression

By 2035, the government will avoid a formal default but will engineer a soft, domestic-focused restructuring through intensified financial repression. This will involve:

- Captive Buyers: Government pressure will ensure that domestic institutions (pension funds, postal savings, major banks) remain the captive buyers of long-term JGBs at rates below market risk.

- Wealth Transfer: The high inflation/low interest rate environment will continue to transfer wealth from the savings of older Japanese citizens to the government (via inflation eroding the real value of their holdings).

- Debt Monetization: The BoJ’s balance sheet, already massive, will continue to expand, essentially monetizing the government’s debt .

Japan will be viewed as a unique, highly advanced economy that successfully sustained an unprecedented level of domestic debt by relying on a closed financial system and a demographic profile that is rich in domestic savings.

https://www.japantimes.co.jp/news/2021/09/05/national/sanae-takaichi-ldp-contender

답글 남기기