Subprime Auto Loan Defaults Ignite Liquidity Fears; Pressure Mounts on Federal Reserve – Following a series of “cockroach” bankruptcies in the high-risk lending sector, markets are bracing for a potential funding squeeze, even as analysts deem systemic banking risk low.

A troubling pattern is emerging from the depths of the U.S. credit market, sparking concerns that what JPMorgan CEO Jamie Dimon once called “cockroaches”—small, visible problems that hint at a much larger, hidden infestation—are surfacing in the subprime auto loan sector.

The recent Chapter 11 bankruptcy filing of PrimaLend Capital, a lender specializing in high-risk auto loans, has intensified these fears. This collapse is not an isolated incident, following closely on the heels of a similar failure by lender Tricolor.

From ‘Buy Here Pay Here’ to Bankruptcy: The Spreading Chill

Both PrimaLend and Tricolor were significant players in the “Buy Here Pay Here” (BHPH) segment. This high-risk model involves providing financing services to car dealerships that, in turn, extend high-interest loans directly to consumers with low credit scores—a group highly vulnerable to economic shocks.

On the surface, the immediate financial fallout from PrimaLend’s failure appears contained. The company’s court filings show both assets and liabilities below the $500 million mark. However, financial analysts argue that the trend of successive failures is the real cause for alarm. This drumbeat of defaults is raising red flags about a potential contraction in market liquidity and a short-term funding squeeze.

SOFR Volatility and Crypto Sell-Offs Signal Liquidity Strain

These emerging credit strains are already showing signs of rippling into broader asset classes. Recent price corrections in traditional safe-havens like gold, as well as in volatile assets like cryptocurrencies including Bitcoin, are seen as being linked to these tightening liquidity conditions.

More technically, volatility has spiked in the Secured Overnight Financing Rate (SOFR), a key benchmark for short-term borrowing. This instability is a direct signal of “temporary anxiety” in the short-term money markets, suggesting that it is becoming more difficult or expensive for financial institutions to secure overnight funding.

Is This Another 2008? The Systemic Risk Debate

Inevitably, a string of subprime defaults evokes the specter of the 2008 subprime mortgage crisis. However, most financial analysts currently assess the risk of a full-blown systemic crisis as low.

The primary difference lies in the exposure of the major banks. Unlike in 2008, the direct exposure of large, systemically important banking institutions to the subprime auto sector is not considered significant. Furthermore, data shows that U.S. bank loan charge-off rates remain at manageable, non-crisis levels.

The Securitization Risk: A New Vector for Contagion

But this does not mean the risk is non-existent. A critical, and often overlooked, danger lies in the practice of securitization. Just as mortgages were bundled into complex securities, these subprime auto loans have been packaged and sold to a wide array of non-bank investors. This practice can obscure the true level of risk and create a different path for contagion, hitting pension funds, insurance companies, and other asset managers.

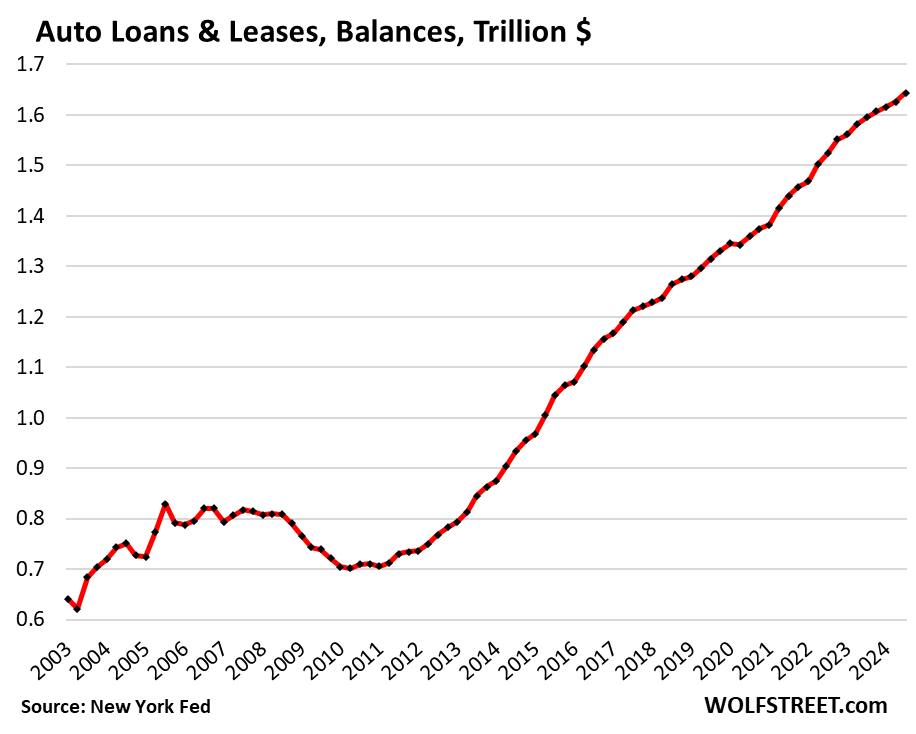

The $1.66 Trillion Problem: Scale of the Auto Loan Market

The underlying market is massive. The total outstanding balance of U.S. auto loans swelled to a staggering $1.66 trillion as of the second quarter of 2024. This represents a 2.26-fold increase from the level at the end of 2011, a period of rapid credit expansion fueled by low interest rates. This sheer volume means that even a small percentage of defaults can translate into billions of dollars in losses, sending shockwaves through the non-bank financial system.

All Eyes on the Federal Reserve as Policy Pressure Builds

This confluence of factors—failing lenders, a large leveraged market, and flickering warning signs in funding rates—has placed the Federal Reserve in a difficult position. The importance of a “preemptive monetary policy” response from the central bank has grown significantly.

A Forced Pivot? Rate Cuts and QT Tapering on the Table

To prevent these isolated defaults from spreading and metastasizing into a wider credit crunch, the Fed is now under pressure to act. Analysts are increasingly calling for aggressive measures, including faster-than-anticipated interest rate cuts and an early termination of its Quantitative Tightening (QT) program. Such moves would be designed to proactively inject liquidity back into the market before funding shortages can cascade.

Prioritizing the Labor Market to Prevent Delinquency

Furthermore, the Fed’s policy focus may be forced to shift. The central bank may have to pivot its primary attention to stabilizing the labor market. There is a direct and powerful link between employment levels and loan delinquency rates; people with jobs pay their car loans. Acknowledging this, the Fed may be compelled to prioritize its full-employment mandate to keep a floor under the credit markets.

Market participants will now be parsing every word from Fed Chair Jerome Powell at the upcoming FOMC press conference, listening for any acknowledgment of these emerging risks and any hints of a policy shift.

Navigating the Fallout: A Market on Edge

While the consensus remains that this is a manageable cooldown for an overheated asset market, the risk of a policy misstep is high. If the defaults spread faster than anticipated, concerns over a funding squeeze will “amplify,” and the downward pressure on asset prices could become severe.

https://www.newyorkfed.org/markets/reference-rates/sofr

https://mgiedit.org/ai-bubble-vs-dot-com-bubble-a-data-driven-2025/

답글 남기기