1. The Paradox of 2024 : Aggregate Rebound vs. American Retreat

In the high-stakes theater of U.S.-China relations, trade fragmentation often dominates the headlines, yet the silent migration of capital offers a far more potent barometer of geopolitical risk. The bilateral financial relationship serves as the foundational architecture of the international monetary system; tracking these flows provides a real-time ledger of how institutional trust is being radically repriced.

Looking back at 2024, a striking paradox has emerged that marks a violent reversal of a decade of institutional courtship. While China’s domestic bond market experienced a renewed influx of global capital, American institutional investors—once the vanguard of the market’s “private sector” era—decisively headed for the exits.

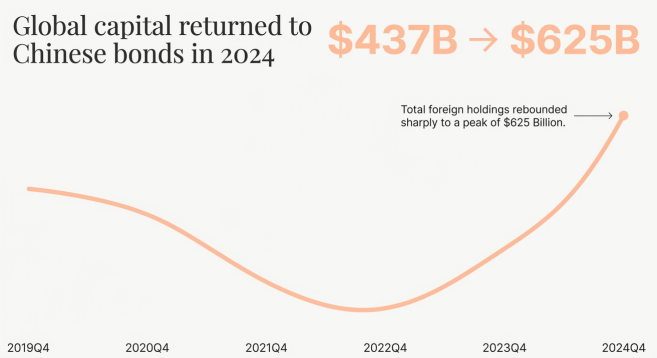

This divergence reveals a fundamental shift in the composition of China’s foreign investor base. According to official Chinese data, total foreign holdings of Renminbi (RMB) bonds surged from a low of $437 billion to a record $625 billion in 2024, a rebound that mirrors the recovery witnessed following the 2015 financial turmoil.

However, U.S. mutual fund holdings moved in the opposite direction, failing to participate in this recovery. This gap signifies that the “internationalization” of the RMB is accelerating, but its participants are increasingly non-American. The result is a fragmentation of global capital where the RMB continues to circulate within a “de-Americanized” circuit, signaling a deep structural decoupling.

Key Figures in the U.S. Institutional Retreat:

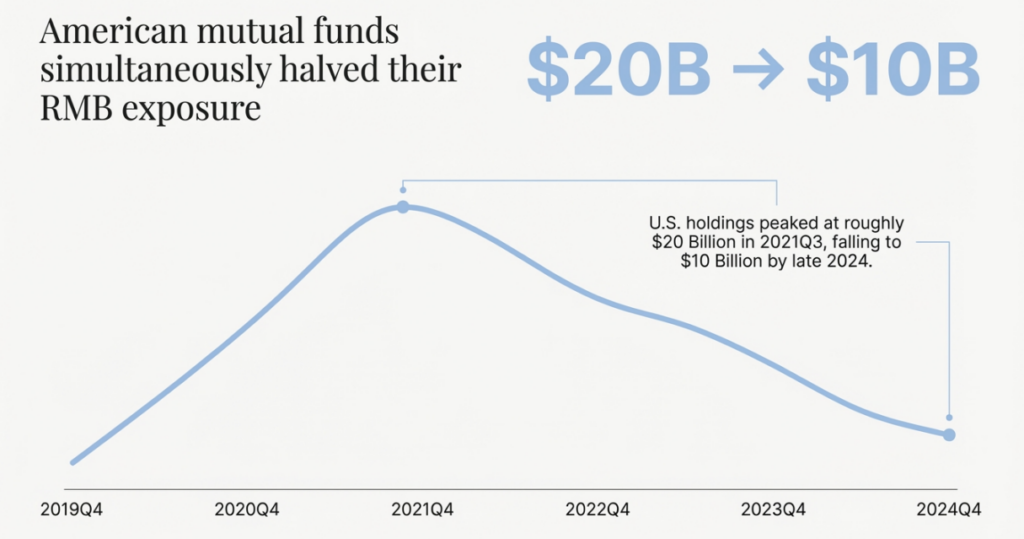

- Peak U.S. Institutional Holdings: ~$20 billion (Recorded in 2021Q3)

- Current U.S. Institutional Holdings: ~$10 billion (Recorded in 2024Q4)

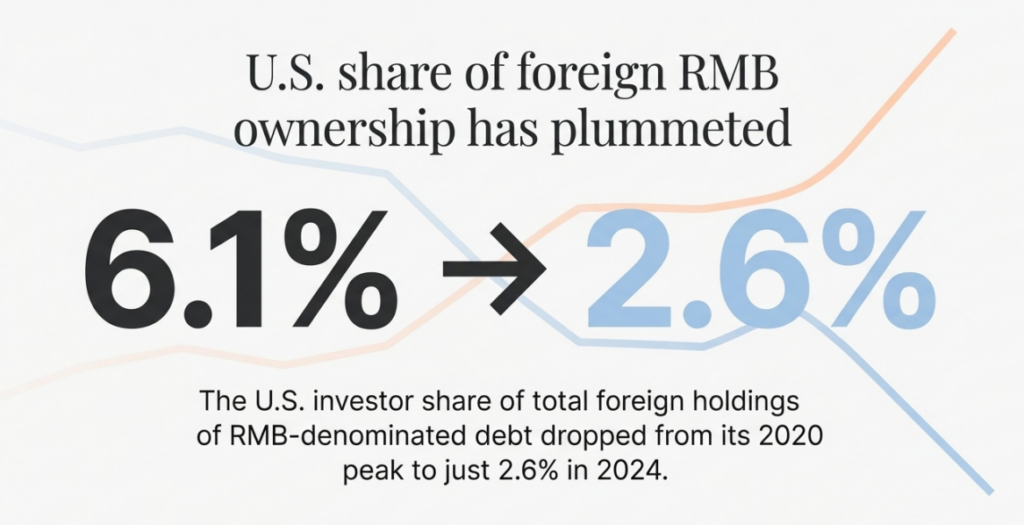

- Market Share Erosion: The U.S. share of total foreign ownership of RMB debt collapsed from 6.1% in 2020 to a mere 2.6% in 2024.

To understand the mechanics of this retreat, we must look beyond aggregate headlines and into the granular microdata that captures the specific movements of American fund managers.

2. The N-PORT Revelation: Precision in Macroeconomic Surveillance

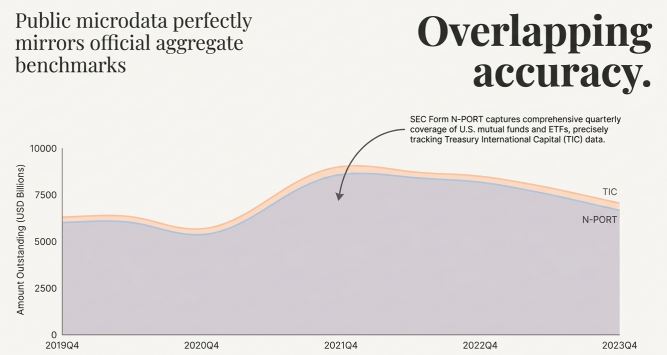

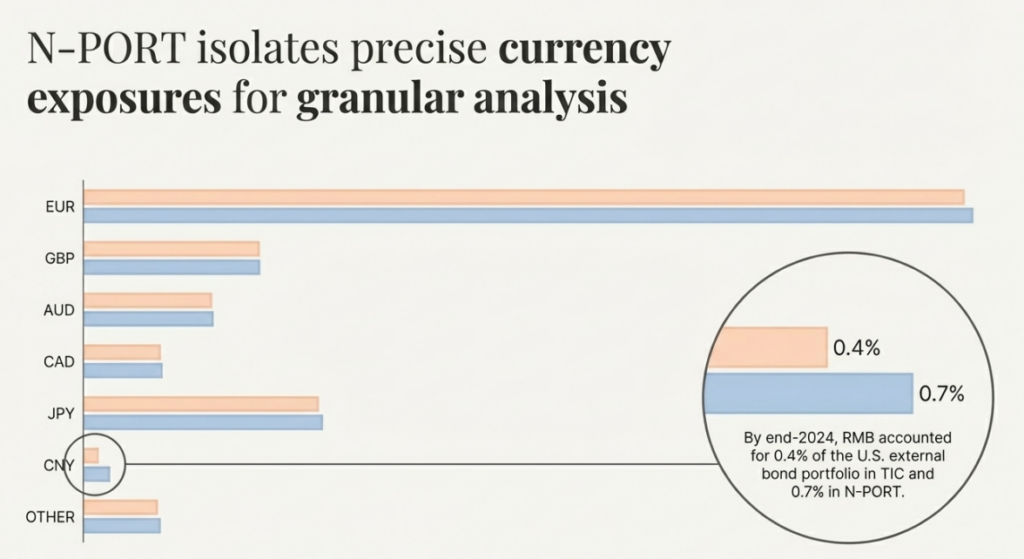

For decades, macro-strategists relied on Treasury International Capital (TIC) data to track cross-border flows. However, the inherent lag and lack of granularity in TIC data often obscured the specific behavior of the investment fund sector. The emergence of high-frequency microdata—specifically SEC Form N-PORT—has become the gold standard for tracking international currency use. By treating N-PORT filings as a “quarterly census,” researchers can now observe the security-level movements of U.S. mutual funds and ETFs with the precision required for institutional surveillance.

The methodology utilized by the Global Capital Allocation Project (GCAP) transforms raw SEC filings into a research-ready panel. This allows for the tracking of specific security identifiers (CUSIP, ISIN) and currency denominations across the entire universe of U.S.-registered funds. The credibility of these findings is bolstered by a near-perfect alignment with official benchmarks. For instance, at the end of 2024, the RMB accounted for 0.4% of the U.S. external bond portfolio in TIC and 0.7% in N-PORT—a level of precision that grants these findings significant institutional weight.

“The close alignment between currency decomposition in TIC and N-PORT data reflects the fact that mutual funds account for a large share of U.S. foreign portfolio investment and that fund holdings are largely representative of the other sectors… N-PORT replicates not only the aggregate level… but also the cross-sectional currency composition.”

This institutional-grade data confirms that the decline in RMB exposure is not a statistical anomaly, but a documented strategic withdrawal by American fund managers.

3. The Anatomy of an Exit: Analyzing the Extensive Margin

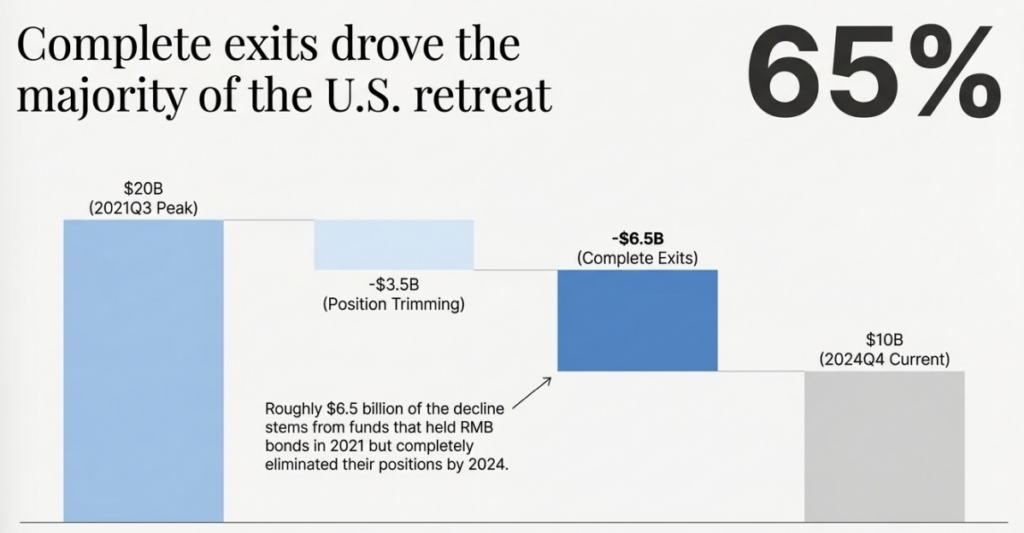

In portfolio management, institutional “appetite” is measured through two lenses: the intensive margin (investors staying in the market but scaling back positions) and the extensive margin (investors liquidating their positions entirely). The $10 billion decline in U.S. RMB bond holdings is particularly significant because it was driven primarily by the latter.

Of the $10 billion drop since the 2021 peak, approximately $6.5 billion—roughly 65%—resulted from funds exiting their RMB positions entirely. This 65% exit rate suggests that China is becoming “uninvestable” for mainstream U.S. funds, moving beyond simple yield-seeking behavior or portfolio rebalancing. The share of U.S. bond funds holding any RMB-denominated debt has plummeted, indicating a systemic reassessment of China-related risk.

U.S. Fund Participation and Conviction Thresholds (2021–2024):

| Threshold (Portfolio Allocation) | 2021Q3 Share of Funds | 2024Q4 Share of Funds |

|---|---|---|

| Any Positive Holding (>0%) | 5.3% | 2.1% |

| Institutional Conviction (>1%) | ~1.8% | ~0.5% |

The collapse in the >1% allocation threshold—the “conviction” holdings—underscores that the retreat is most pronounced among those who previously viewed the RMB as a core strategic asset.

4. A Staggered Liberalization Meets Geopolitical Friction

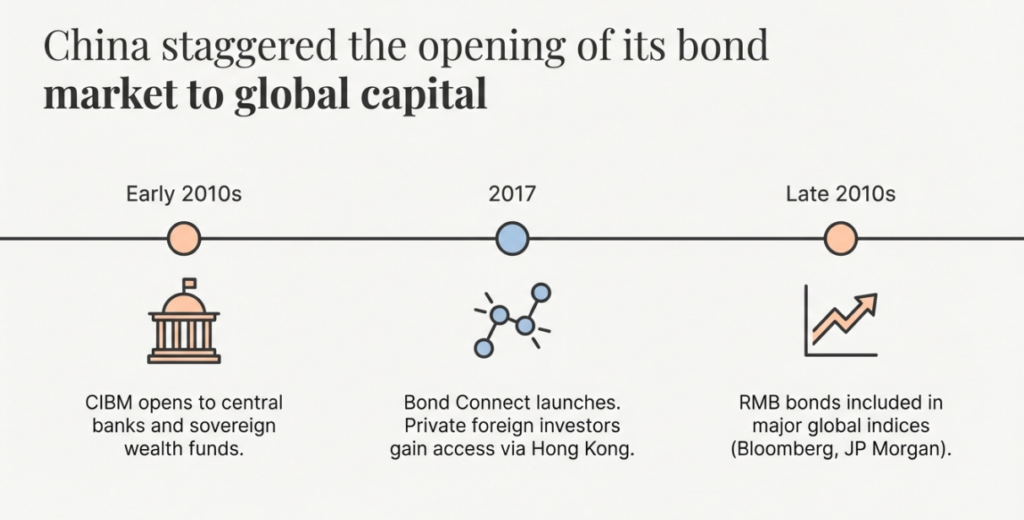

The current exodus stands in stark contrast to the optimism of the previous decade. China’s path to RMB internationalization was defined by a “staggered liberalization” designed to attract stable capital while preventing flight.

- CIBM Access (Early 2010s): Opened the China Interbank Bond Market primarily to “official” investors like central banks.

- Bond Connect (2017): A watershed moment that allowed private foreign investors to trade onshore bonds via Hong Kong using global infrastructure.

- Index Inclusion: Major benchmarks (JP Morgan, Bloomberg) added RMB bonds, forcing a wave of institutional inflows.

While this process successfully transitioned the market from official dominance to private participation, that momentum was broken by the “Zero-Covid” era and escalating geoeconomic tensions. This retreat appears as a unique geopolitical outlier for the United States. While European investment in Chinese bonds also declined (as noted by Beck et al. 2024), Europeans still hold a larger share than their American counterparts. The U.S. withdrawal, occurring alongside a rebound in total foreign holdings, suggests that the internationalization of the RMB is bifurcating along geopolitical lines.

5. Conclusion: The Realignment of the Global Financial Order

The U.S.-China bilateral financial relationship remains the core of the international system, but it is undergoing a profound fragmentation. The GCAP findings suggest that we have entered a “new normal” where the Renminbi may continue to internationalize, but will do so increasingly without the participation of the American mutual fund industry.

The compositional shift away from U.S. institutional investors carries long-term implications for market transparency. As U.S. capital exits, it is being replaced by entities—potentially official or non-U.S. private actors—that operate outside the rigorous SEC reporting requirements of Form N-PORT. This “Transparency Gap” means that the next phase of RMB internationalization will be characterized by less oversight and a shift toward less-regulated global entities. The world’s second-largest economy is becoming increasingly decoupled from the world’s largest pool of institutional capital, leaving U.S. policymakers and investors partially blind to the evolving structure of the international monetary system.

Strategic Takeaways

The Transparency Gap: The retreat of U.S. funds, which are subject to high-frequency SEC monitoring, creates a surveillance vacuum. The future of China’s foreign investor base will be characterized by less transparency and a shift toward potentially less-regulated global entities.

The Exit is Structural and Extensive: 65% of the U.S. pullback is driven by total liquidation rather than position trimming, suggesting a permanent shift in risk assessment regarding Chinese “uninvestability.”

Institutional Bifurcation: While total foreign investment in China rebounded to a record $625 billion in 2024, U.S. participation hit multi-year lows, indicating that the RMB is internationalizing through a non-Western, or “de-Americanized,” circuit.

답글 남기기