OBBBA: The US Economy’s New Path in 2025 – A Deep Dive : The recently enacted One Big Beautiful Bill Act (OBBBA), signed by President Trump on July 4, 2025, signals a profound reorientation of American economic policy. Far from a mere fiscal stimulus, the legislation, at its core, embodies a Trumpian vision for growth, prioritizing supply-side incentives and a recalibration of national priorities.

This sweeping legislative overhaul is poised to unleash a complex interplay of short-term gains and significant long-term challenges, potentially ushering in an era of amplified economic divergence.

A Policy Pivot: Three Pillars of Change

The OBBBA’s architecture rests on three foundational pillars, each reflecting a stark departure from previous administrations.

Massive Tax Reductions: The OBBBA primarily focuses on making the provisions of the Tax Cuts and Jobs Act (TCJA) permanent, thereby reducing the tax burden across individuals and corporations.

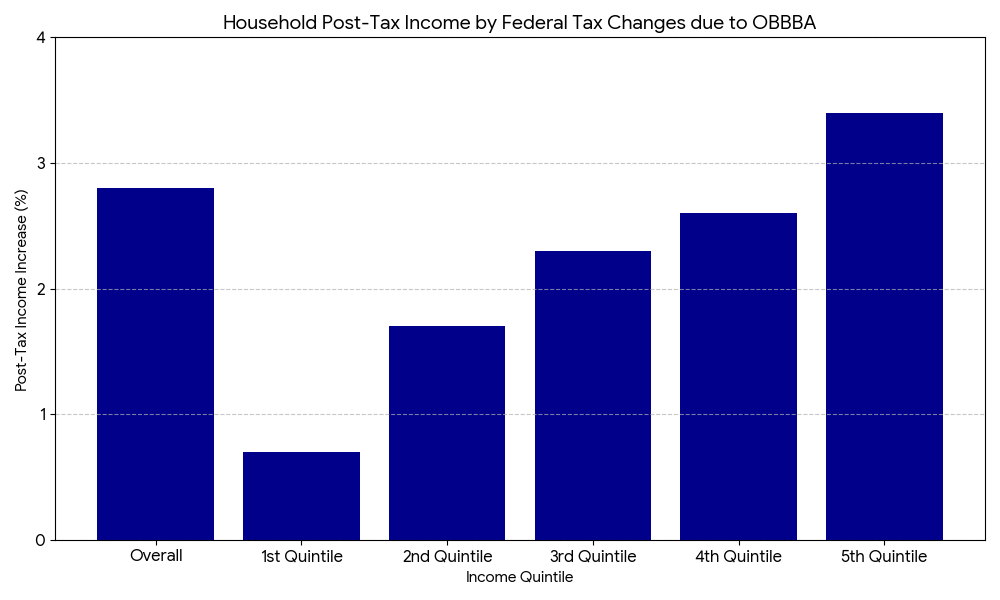

For Individuals: While benefiting most taxpayers, the tax cuts are disproportionately larger for higher-income households, with those in the top 1-5% seeing over 4% post-tax income increase. Notably, the basic deduction for inheritance and gift taxes has been dramatically increased to $15 million and made permanent, a significant boon for the wealthiest asset holders. State and Local Tax (SALT) deduction limits are also temporarily raised from $10,000 to $40,000, benefiting high-income homeowners.

For Corporations: The act includes permanent 100% bonus depreciation, allowing immediate deduction of costs for machinery and equipment, and even manufacturing real estate, to encourage domestic supply chain restructuring. R&D expenses incurred within the US are now immediately deductible instead of being amortized over five years. These measures, while designed to stimulate investment, are projected to swell the fiscal deficit by over $4 trillion over the next decade.

Increased Defense and Security Spending : The OBBBA substantially boosts budgets for national defense and border security, aligning with a “strong America” philosophy.

Over $100 billion in new funds are earmarked for defense modernization, including advanced weaponry and naval capabilities.

The Department of Homeland Security (DHS) also sees substantial increases, with over $46.5 billion for border wall construction, $45 billion for immigrant detention facilities, and over $10 billion for Border Patrol (CBP) personnel and equipment. This allocation reflects a strategic shift towards national security as a key economic driver.

Rollback of Green and Welfare Policies : To secure funding and shift policy direction, key Biden administration initiatives are being eliminated or significantly curtailed.

The Inflation Reduction Act (IRA)’s green energy policies are particularly affected, with electric vehicle purchase tax credits, residential clean energy installation tax credits, and clean electricity production tax credits immediately terminated or phased out, saving an estimated $271 billion over 10 years.

Social safety nets for low-income individuals are also being tightened. Medicaid will require physically able adult recipients to work or engage in related activities for at least 80 hours per month, reducing expenditure by $317 billion over 10 years. Food Stamps (SNAP) will also see spending cuts through stricter eligibility criteria, such as raising the work requirement age to 65. This element highlights a deliberate trade-off, securing fiscal space for tax cuts and defense at the expense of social and environmental initiatives.

The Fiscal Paradox: Short-Term Buoyancy, Long-Term Strain

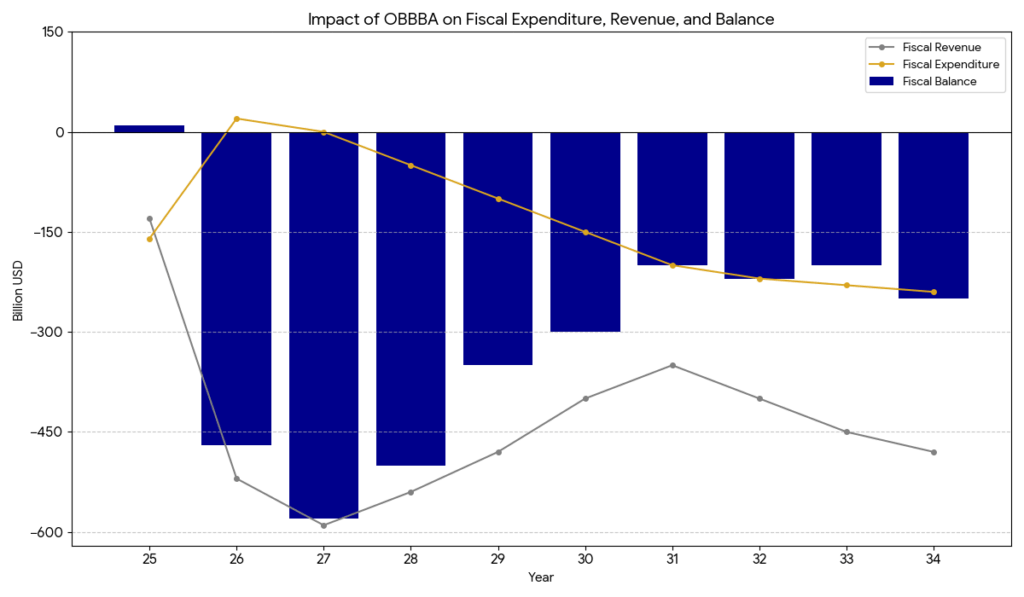

The OBBBA’s immediate economic effect is likely to be a transient surge in activity, fueled by the substantial injection of fiscal capital. However, this impetus comes at a cost, as the legislation simultaneously threatens long-term fiscal stability and risks significant crowding-out effects from rising market interest rates, potentially limiting potential growth. Projections from the Committee for a Responsible Federal Budget (CRFB) indicate an additional $4.1 trillion expansion of the fiscal deficit over the next decade due to the OBBBA.

Fiscal Deficit Concentration: A critical characteristic of this fiscal impact is its temporal concentration. The brunt of the deficit expansion is front-loaded, heavily impacting the Trump administration’s tenure until 2028. While 2025 might see a minor deficit reduction of about $40 billion due to specific spending cuts like reduced student loan support , the subsequent years — 2026 and 2027 — are forecast to witness increases of $0.5 trillion and $0.6 trillion, respectively, as the tax cuts fully manifest.

This immediate fiscal deterioration is largely a consequence of the accelerated implementation of tax reductions, most of which begin at the end of 2025, while the more gradual nature of spending cuts takes longer to materialize, mostly from 2028

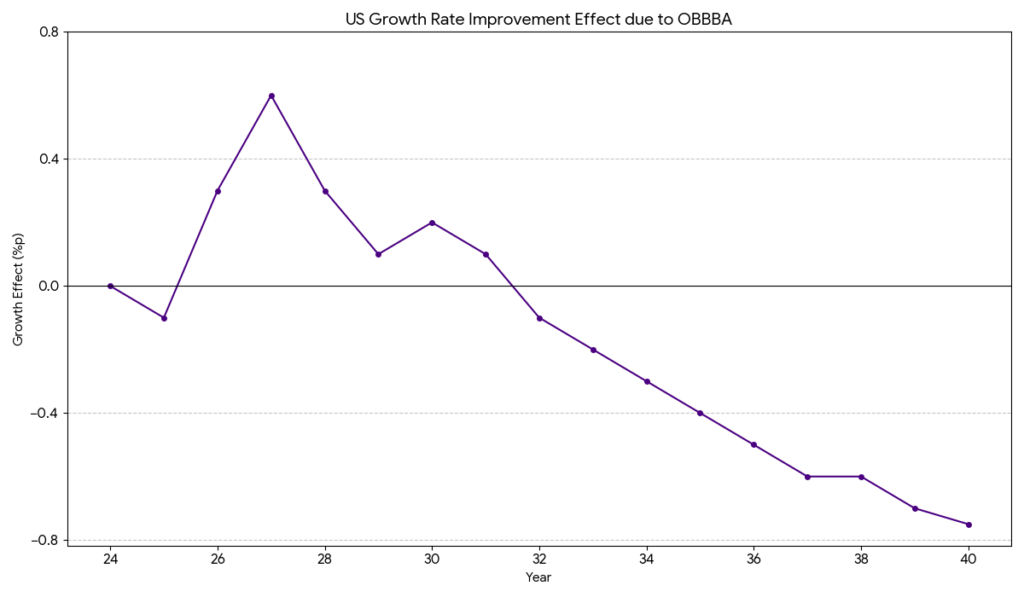

Limited Growth Impact: Despite the magnitude of the fiscal intervention, the anticipated boost to average annual growth for 2025-2027 is a modest 0.2%p. This limited multiplier effect can be attributed to the OBBBA’s focus on corporate and high-income tax cuts, which historically exhibit lower fiscal multipliers (0.0x-0.4x and 0.1x-0.6x respectively) compared to broader public investments (average >1.0x) or support for lower-income segments.

The Yale Budget Lab’s macroeconomic simulations corroborate this, forecasting a temporary growth acceleration until 2027, followed by a deceleration as the weight of accumulated debt, rising interest rates, and the subsequent crowding-out effects begin to bite from 2028. This suggests a fundamental disjunction: significant fiscal expansion without a proportional boost to broad-based economic activity.

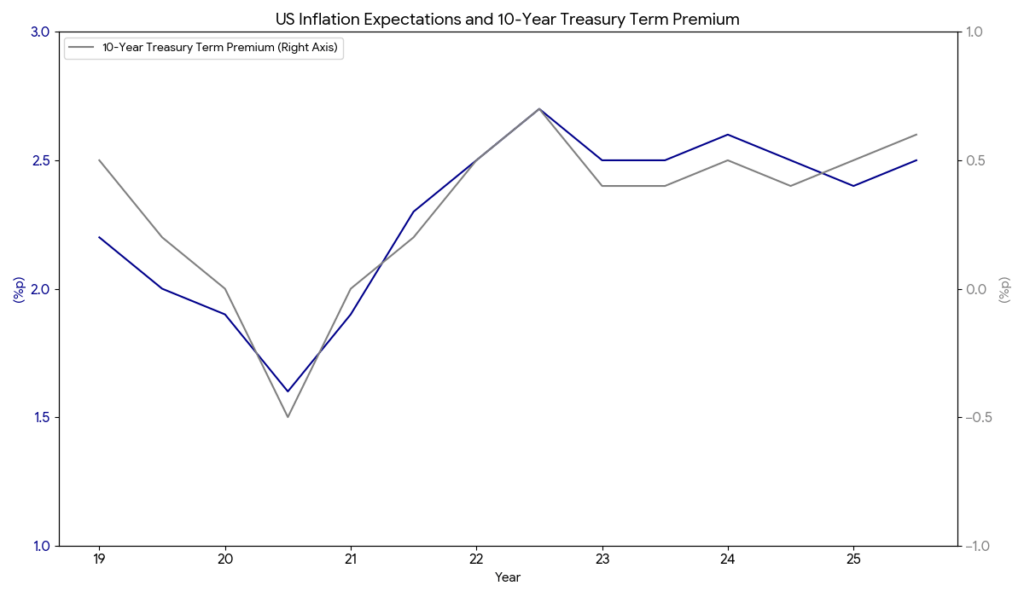

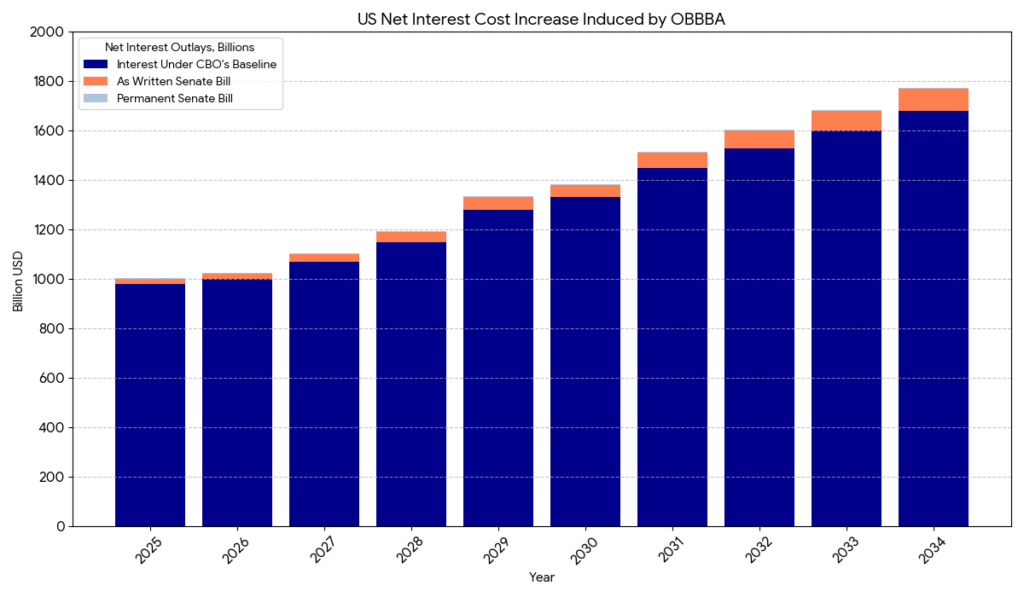

Interest Rate Pressure: The substantial annual fiscal deficits expected until 2029 will impact the bond market. The financial market anticipates these increased borrowing needs, leading to upward pressure on long-term Treasury yields. The Congressional Budget Office (CBO) estimates an $800 billion increase in net interest costs alone over the next 10 years due to the OBBBA.

Moreover, the inflationary potential of expansionary fiscal policy, coupled with a lagging unemployment rate that is expected to further decrease until 2028 , could compel the Federal Reserve to maintain a tighter monetary stance or defer interest rate cuts beyond market expectations. The Yale Budget Lab projects a 0.56%p increase in the 10-year Treasury yield by 2028 relative to its baseline , reflecting not only sustained inflation but also heightened term premiums due to supply pressures.

The K-Shaped Trajectory: Deepening Divides

The OBBBA’s impact extends beyond macroeconomic aggregates, threatening to entrench and exacerbate existing inequalities within the American economy, thereby accelerating a distinct K-shaped economic trajectory.

Deepening Inequality and Limited Consumption: The pronounced bias of the tax cuts towards high-income households and asset owners is undeniable. Data from the Tax Policy Center (TPC) suggests that while average post-tax income will increase by 2.8%, the top 20% of households will see a 3.4% rise, with the wealthiest 1-5% experiencing over 4% growth. This, combined with the scaling back of low-income support programs, is poised to deepen intra-household income inequality.

The critical insight here is that higher-income individuals typically exhibit lower propensities to consume (as shown in the consumption propensity by income quintile) , meaning a significant portion of their tax savings is unlikely to translate into immediate, broad-based consumption-driven growth.

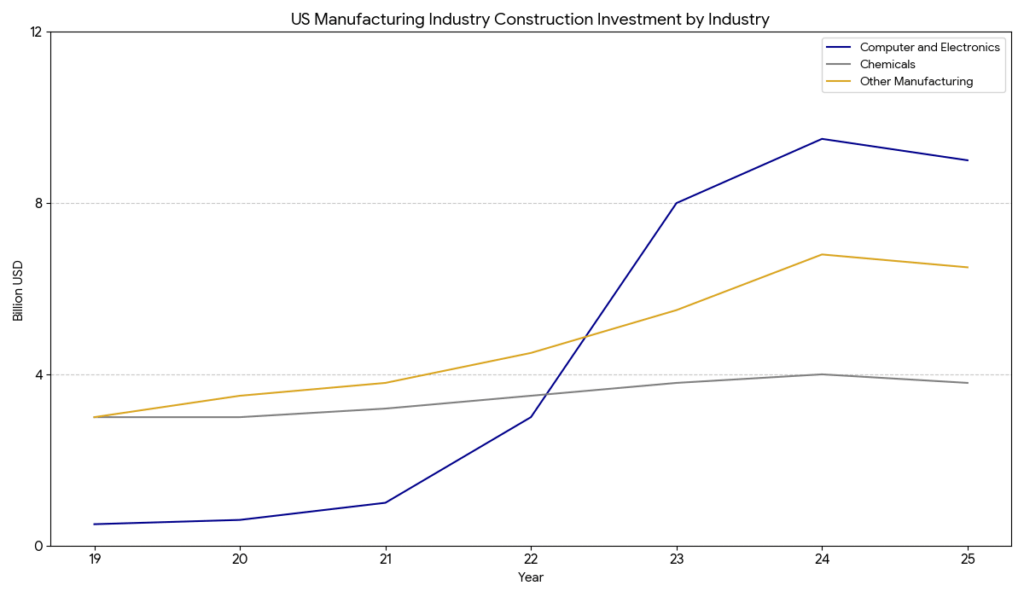

Investment Over Consumption: The OBBBA prioritizes investment over consumption, particularly in high-tech manufacturing. The permanent 100% bonus depreciation and the significant increase in tax credits for advanced manufacturing from 25% to 35% underscore a powerful policy commitment to industrial re-shoring.

Notably, the legislation also provides a degree of protection for existing and planned renewable energy investments by tying tax credit eligibility to the project’s start date rather than completion, removing a key source of uncertainty and potentially spurring short-term investment. This targeted approach is expected to revive investment momentum, especially in the computer and electronics sectors, which saw a slump following prior policy uncertainties.

Real Economy vs. Financial Markets Disparity: The substantial liquidity generated by tax cuts for high-income earners and corporations is highly probable to seek returns in asset markets – stocks, bonds, and real estate – rather than immediate consumption or employment in the real economy. This dynamic creates a “financial market rally” even amidst concerns of a decelerating real economy, a classic manifestation of the K-shaped phenomenon where financial assets decouple from underlying economic fundamentals.

The Specter of Stagflation and Financial Volatility

The most pressing long-term concern emanating from the OBBBA is the potential for a confluence of rising interest rates, inflationary pressures, and persistent crowding-out effects. This could lead to a significant deterioration of financial conditions and heightened market volatility. The anticipated surge in long-term Treasury yields, projected to be 1.2%p, could significantly dampen corporate investment and household durable goods consumption.

Critically, the destructive potential of crowding-out effects amplifies when combined with escalating inflation expectations. While current market expectations for inflation remain relatively stable despite tariff threats , historical precedents suggest that periods of rising inflation expectations often coincide with a sharp increase in the term premium component of long-term bond yields. The OBBBA’s expansionary fiscal stance inherently creates demand-pull inflationary pressures. Should this combine with supply shocks from ongoing high tariffs, the stability of inflation expectations could rapidly erode. In such a scenario, investors would demand a higher term premium, risking a sharp spike in long-term Treasury yields.

In essence, the US economy has become acutely vulnerable to potential price shocks. A policy disconnect, where expansionary fiscal measures compel the Federal Reserve to maintain a tighter monetary stance, could, if coupled with a resurgence in inflation expectations, inevitably lead to a tightening of financial conditions. This, in turn, risks weakening the real economic recovery and propagating volatility throughout the financial system. Close monitoring of how OBBBA’s fiscal impact interacts with inflation indicators will be paramount in navigating this intricate economic landscape.

The OBBBA, therefore, represents a bold, yet risky, experiment in American economic governance. Its success hinges not merely on the short-term stimulus it provides, but on its ability to genuinely transform the US economic structure and enhance industrial competitiveness before the inevitable headwinds of fiscal strain and rising interest rates become overwhelming.

https://mgiedit.org/the-trump-eras-economic-report-card-q1-2025-gdp/

답글 남기기