In the complex world of credit risk management, aggregate debt figures often obscure the true financial health of individual borrowers.

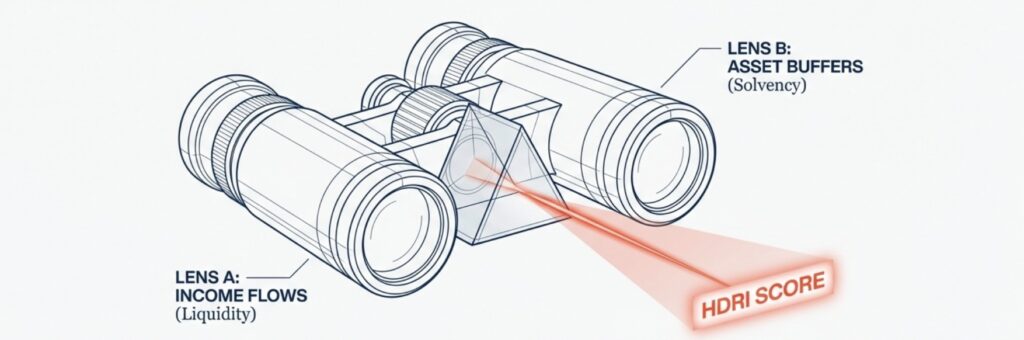

To address this analytical blind spot, financial experts utilize a composite metric known as the Household Debt Risk Index (HDRI). This sophisticated indicator moves beyond simple loan-to-value assessments, offering a dual-lens view of solvency by simultaneously stress-testing an entity’s income flows and asset buffers.

Defining the HDRI

The Household Debt Risk Index (HDRI) is designed to gauge the probability of household insolvency by synthesizing two critical financial ratios:

- Debt Service Ratio (DSR): Measures liquidity risk—the ability to service debt obligations from current income.

- Debt To Asset Ratio (DTA): Measures solvency risk—the ability to cover debts through asset liquidation.

Unlike single-dimensional metrics, the HDRI provides a holistic assessment, recognizing that a borrower might have high income but few assets, or substantial assets but poor cash flow.

The Mechanics of the Index

The HDRI operates on a standardized scoring model to identify potential weak points in a portfolio.

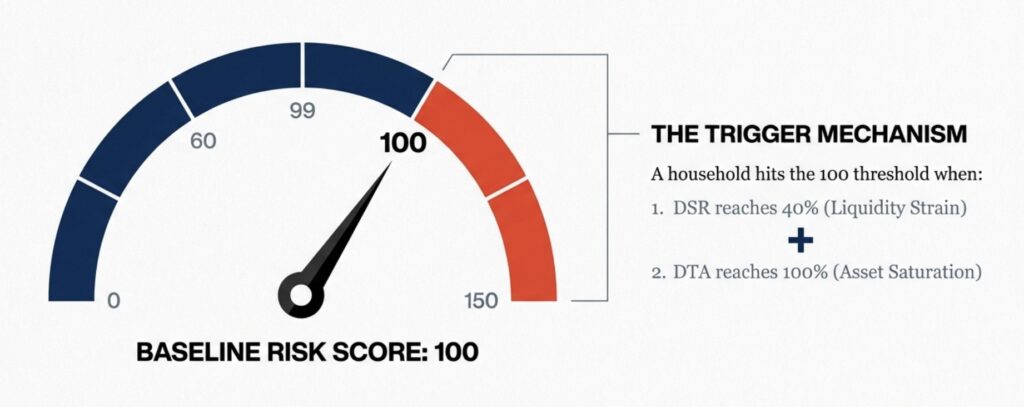

- The Critical Threshold (100): The index is calibrated so that a value of 100 represents the baseline for risk. This baseline is typically triggered when a household’s DSR reaches 40% and DTA reaches 100%.

- Risk Classification: Any household with an HDRI score exceeding 100 is classified as a “Risk Household.”

Segmentation of Risk Profiles

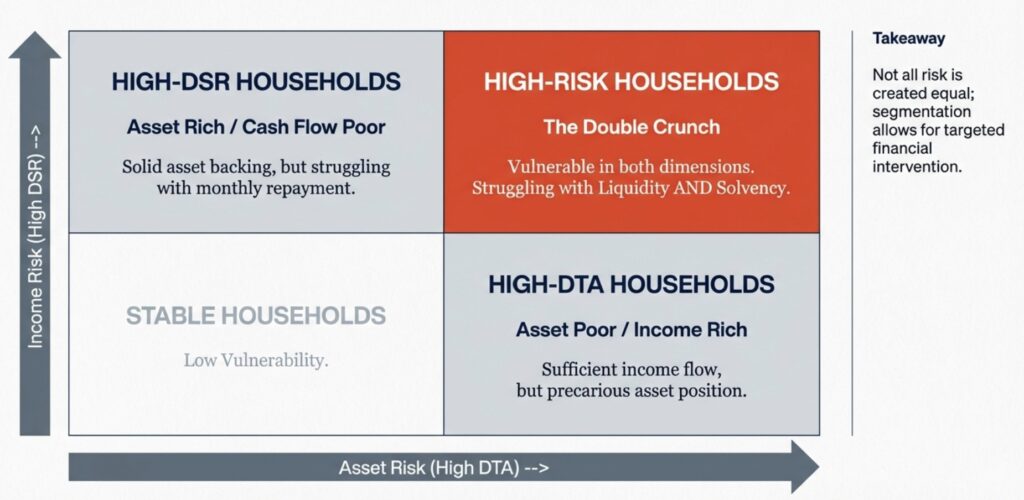

To facilitate targeted financial interventions, Risk Households are further segmented based on the nature of their vulnerability:

- High-Risk Households: Borrowers facing a “double crunch”—vulnerable in both income (liquidity) and asset (solvency) dimensions.

- High-DTA Households: Borrowers with sufficient income flow but a precarious asset position relative to their debt.

- High-DSR Households: Borrowers with solid asset backing but struggling with monthly repayment cash flows.

Interpreting the Signals

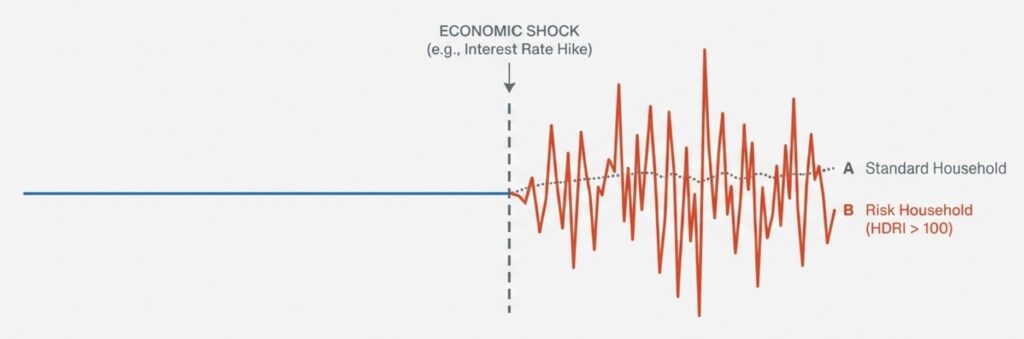

It is crucial to interpret the HDRI with nuance. Being categorized as a “Risk Household” (Index > 100) measures the structural vulnerability of a borrower’s repayment capacity.

It does not imply immediate default. Instead, a high HDRI serves as an early warning signal, indicating that these households are statistically more sensitive to economic shocks—such as interest rate hikes or asset price corrections—than the general population.

https://kdijep.org/v.32/4/1/Risk+Analysis+of+Household+Debt+in+Korea+Using+Micro+CB+Data

답글 남기기