Global SME Finance Trends 2025: Navigating Uncertainty with FinTech & Government Support – The global economic landscape is in a state of flux. Persistent inflationary pressures, coupled with a surge in geopolitical uncertainty, have cast a long shadow over growth prospects, leading to a discernible slowdown in the global economy.

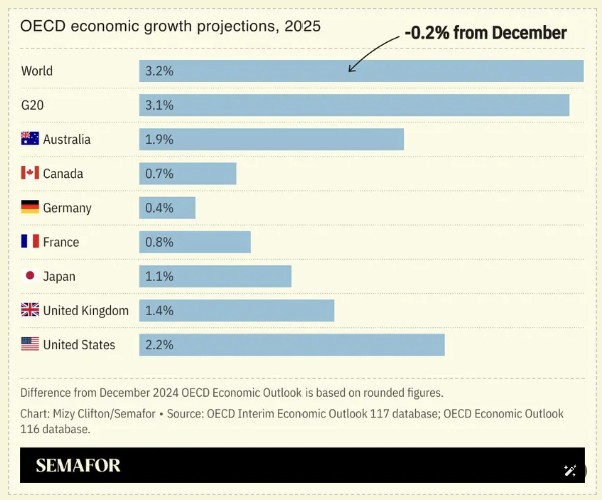

The OECD’s economic growth forecast reflects this reality, projecting a dip from 3.1% in 2025 to 3.0% in 2026. This challenging environment has disproportionately impacted the lifeblood of economies worldwide: small and medium-sized enterprises (SMEs). Often less resilient to external shocks than their larger counterparts, SMEs are finding themselves navigating increasingly restrictive financial conditions, a trend starkly highlighted in the recently released 2025 OECD SME Financing Scoreboard.

The Scoreboard, a crucial annualتقرير analyzing SME-related data and financial market trends across some 50 countries, paints a clear picture of the difficulties faced by these businesses in 2023 and the early outlook for 2024-2025. The headline figures are striking: a 4.1% decrease in outstanding SME loan balances and a more significant 9.0% drop in new SME loans in 2023, both based on median values. This contraction in lending is not merely a statistical anomaly; it is a critical indicator of the mounting pressure on SMEs and a potential harbinger of broader economic challenges.

Current Trends and Challenges

The reasons behind this tightening of the financial阀 for SMEs are multifaceted, stemming directly from the prevailing macroeconomic conditions. High interest rates, a primary tool used by central banks to combat inflation, have increased the cost of borrowing, making new loans less attractive and servicing existing debt more burdensome for businesses.

Simultaneously, the lingering effects of the cessation of COVID-19 related government guarantee schemes have removed a vital safety net that previously facilitated access to credit for many SMEs. Furthermore, in some regions, particularly in Latin American countries with a higher proportion of foreign currency-denominated debt like Brazil, Colombia, and Mexico, the depreciation of local currencies against the dollar has drastically increased the cost of servicing dollar-denominated loans, forcing businesses to reduce their existing debt burdens.

Beyond the aggregate decline in lending, the Scoreboard also reveals a concerning shift in the nature of SME financing. There is a noticeable move away from long-term investment financing towards a greater reliance on short-term funding. This pivot is a direct consequence of the economic uncertainty and high-interest rate environment, which erodes SMEs’ confidence and capacity for long-term strategic investments. Instead, businesses are prioritizing the 확보 of immediate liquidity to manage day-to-day operations and navigate unpredictable market conditions. The case of Spain, where the average maturity of new SME loans dropped below 11 months in 2023 for the first time since 2012, is a stark illustration of this trend.

This contraction in both the volume and maturity of SME lending has significant implications. For individual businesses, it can stifle growth, hinder innovation, and ultimately threaten viability. On a macroeconomic level, given that SMEs are major contributors to employment and GDP in most economies, a struggling SME sector can dampen overall economic growth, exacerbate unemployment, and impede productivity gains. The OECD highlights that restrictive financial conditions have already contributed to a decline in business investment in over half of its member countries in the second quarter of 2024.

Government and Policy Responses

Recognizing the critical role of SMEs and the challenges they face, governments worldwide are stepping up efforts to provide support. The anticipated persistence of difficult funding conditions for SMEs in 2023-2024 has prompted a renewed focus on policy interventions aimed at alleviating immediate liquidity constraints and stimulating investment in strategic sectors. The responses vary across countries but generally coalesce around several key pillars:

- Expanding Guarantee Loan Programs: Government-backed loan guarantee schemes remain a popular and effective tool to de-risk SME lending for financial institutions, thereby encouraging the flow of credit. Hungary, for instance, is supporting new guarantee loans through the European Investment Fund.

- Boosting Venture Capital Investment: To foster innovation and support high-growth potential SMEs, particularly in their early stages, governments are promoting venture capital initiatives. The UK’s British Growth Partnership and Germany’s Wachstumsfonds Deutschland are examples of programs designed to channel private and public funds into innovative SMEs. Germany’s fund alone is expected to exceed 1 billion Euros.

- Targeted Support for Strategic Industries: Governments are increasingly recognizing the importance of directing support towards sectors deemed crucial for future economic competitiveness and sustainability. This includes areas like green technologies and digital transformation. France, for example, has allocated funds to support early-stage generative AI companies and is establishing a specialized fund for quantum technology. Denmark is also creating a regional scale-up fund for renewable energy and sustainability.

- Promoting Regional Balanced Development: Efforts are also being made to ensure that financial support reaches SMEs in all regions, fostering balanced economic development. France’s public investment bank, Bpifrance, is expanding its regional office network to achieve this.

The Future of SME Financing: A New Era

These government initiatives are a crucial lifeline for many SMEs, but the challenges are significant and require a multi-pronged approach involving not just public sector intervention but also the active participation of the financial industry.

Looking ahead, the future of SME financing will likely be shaped by a confluence of technological advancements, evolving economic dynamics, and shifting business models. Several key trends are expected to dominate the landscape:

The Digital Transformation of SME Finance: The adoption of financial technology (FinTech) is set to accelerate, fundamentally altering how SMEs access funding and manage their finances. Online lending platforms are becoming increasingly prevalent, offering faster and more streamlined application processes compared to traditional banks. This trend is expected to continue, with some estimates suggesting a significant volume of SME lending could be transacted via lending platforms in the coming years.

The Rise of AI and Data Analytics: Artificial intelligence (AI) and advanced data analytics will play a transformative role in SME lending. By analyzing vast amounts of data, including alternative data sources beyond traditional credit scores (such as real-time business activity, mobile phone usage, and social media activity), AI can provide more accurate credit risk assessments, enabling lenders to make faster and more informed decisions and potentially expand access to funding for previously underserved SMEs. This move away from outdated, fixed-criteria models will be crucial in better understanding the true financial health and potential of diverse SMEs. AI can also streamline operational workflows, reduce the need for extensive documentation, and minimize operational costs for lenders, potentially leading to lower fees for borrowers.

Blockchain for Transparency and Security: Blockchain technology holds the potential to enhance security and transparency in SME financing. By creating a secure and tamper-proof record of transactions, blockchain can reduce fraud and build greater trust between lenders and borrowers. While still in relatively early stages of adoption in SME finance, its potential for creating more secure and transparent lending ecosystems is significant.

The Growing Importance of Alternative Financing: Beyond traditional bank loans, alternative financing methods will continue to gain prominence. This includes not only online lending platforms but also instruments like factoring, leasing, and potentially more innovative approaches like supply chain finance and peer-to-peer lending specifically tailored for SMEs. As SMEs become more aware of these alternatives, and as the ecosystem supporting them develops, their uptake is likely to increase.

Focus on Green and Sustainable Finance: With the increasing global focus on climate change and sustainability, there will be a greater emphasis on “green” finance for SMEs. This will involve financial products and incentives designed to support SMEs in adopting environmentally friendly practices, investing in renewable energy, and reducing their carbon footprint. Governments and financial institutions are likely to introduce more targeted funding and support mechanisms for green SME initiatives.

Personalized Financial Products: Leveraging data analytics and AI, financial institutions will be able to offer more personalized financial products and services tailored to the specific needs and risk profiles of individual SMEs. This could include flexible repayment terms, customized loan structures, and integrated financial management tools.

Collaboration between FinTech and Traditional Institutions: Rather than a complete replacement of traditional banking, the future of SME finance is more likely to involve increased collaboration between FinTech companies and established financial institutions. FinTech firms can provide innovative technology and agile platforms, while traditional banks offer a large customer base, regulatory expertise, and established infrastructure. These partnerships can lead to hybrid models that combine the strengths of both, offering SMEs a wider range of accessible and efficient financing options.

Addressing the Data Challenge: A significant hurdle in SME lending has traditionally been the lack of comprehensive and easily accessible data on businesses, making credit assessment challenging. The future will see continued efforts to address this “data challenge” through the development of unified data platforms, improved data sharing mechanisms (with appropriate privacy safeguards), and the use of AI to analyze diverse data sources.

The Evolving Role of Government Support: Government support will remain crucial, but the focus may shift. While direct financial aid and guarantees will still be necessary, there will likely be a greater emphasis on creating an enabling environment for SME finance. This includes investing in digital infrastructure, promoting financial literacy among SMEs, streamlining regulations, and incentivizing private sector investment in the SME ecosystem. Targeted support for strategic sectors and regional development will also continue to be important.

Increased Focus on Resilience and Digitalization: The recent global shocks have underscored the importance of SME resilience. Future financing solutions will likely incorporate elements that help SMEs build greater resilience to economic downturns and external shocks. This could include flexible financing options, access to risk management tools, and support for digitalization to improve operational efficiency and market reach. Digitalization, in particular, is no longer a luxury but a necessity for SMEs to remain competitive and access a wider range of financing options.

The Global Context and Interconnectedness: The future of SME finance will also be influenced by global economic trends and the increasing interconnectedness of economies. Geopolitical stability, trade policies, and global capital flows will all play a role in shaping the availability and cost of funding for SMEs. As SMEs become increasingly integrated into global value chains, their financing needs and options will also become more internationalized.

In conclusion

The global SME financial market is at a critical juncture. The current environment of high inflation and geopolitical uncertainty presents significant challenges, leading to a contraction in traditional lending and a shift towards shorter-term financing. However, these challenges are also acting as a catalyst for innovation and policy reform. Governments and the financial

industry are recognizing the need to adapt and develop new approaches to support SMEs.

The future of SME financing will be characterized by the increasing integration of technology, particularly FinTech and AI, leading to more efficient, data-driven, and personalized lending solutions. Alternative financing methods will become more mainstream, and there will be a growing focus on green and sustainable finance. While traditional banks will continue to play a role, collaboration with FinTech firms will be key to expanding access to credit and meeting the evolving needs of SMEs.

Navigating this complex landscape will require ongoing collaboration between policymakers, financial institutions, and SMEs themselves. By embracing technological advancements, fostering an enabling regulatory environment, and developing innovative financing solutions, the global community can help ensure that SMEs continue to thrive, contributing to economic growth, job creation, and a more prosperous future. The challenges are real, but the potential for transformation is equally significant, heralding the dawn of a new era for SME finance.

https://thedigitalbanker.com/sme-banking-insights

https://blogs.worldbank.org/en/psd/capital-markets–the-new-frontier-for-sme-financing

https://mgiedit.org/wp-admin/post.php?post=381&action=edit

답글 남기기