2025 American Anomaly: Navigating Fiscal Strain and Economic Resilience – Our baseline scenario is a continued but fragile soft landing through the second half of 2025. This outlook is predicated on three key assumptions: (1) the U.S. labor market, the bedrock of consumer spending, remains solid and avoids a sharp contraction; (2) the Artificial Intelligence-led technology investment cycle maintains its powerful momentum, driving both capital expenditure and productivity gains; and (3) the Federal Reserve successfully navigates a rate-cutting cycle, beginning in late 2025, without reigniting stubborn inflationary pressures. This path, however, is narrow and fraught with peril.

The future trajectory of the U.S. economy and its financial markets hinges on the battle between two opposing forces, which can be monitored through key indicators. The primary indicator of fiscal strain is the 10-year Treasury term premium, which reflects the market’s evolving price for sovereign risk and inflation uncertainty. A sharp, sustained rise in this premium would signal a dangerous loss of confidence. The primary indicator of economic resilience is the capital expenditure and earnings trajectory of the “Magnificent Seven” technology companies. A sudden faltering in their investment or profitability would remove the main engine of current growth. The interplay between these two variables will define the next economic chapter.

The analysis concludes that the U.S. is undergoing a fundamental regime shift where fiscal policy has supplanted monetary policy as the primary driver of market volatility and long-term interest rates. The post-2008 playbook, centered on the Federal Reserve’s omnipotence, is now obsolete. Investors and policymakers must adapt to an environment where the government’s borrowing needs and fiscal credibility are paramount, introducing a new and unpredictable dimension of risk into the global financial system.

A Soft Landing on a Bumpy Runway

In the face of persistent inflation, an aggressive monetary tightening cycle, and escalating geopolitical tensions, the U.S. economy has demonstrated a degree of resilience that has defied conventional forecasts. This section deconstructs the key pillars supporting this remarkable performance: a robust labor market, a transformative technology investment cycle, and the surprisingly contained impact of a global trade shock.

The Labor Market as Bedrock

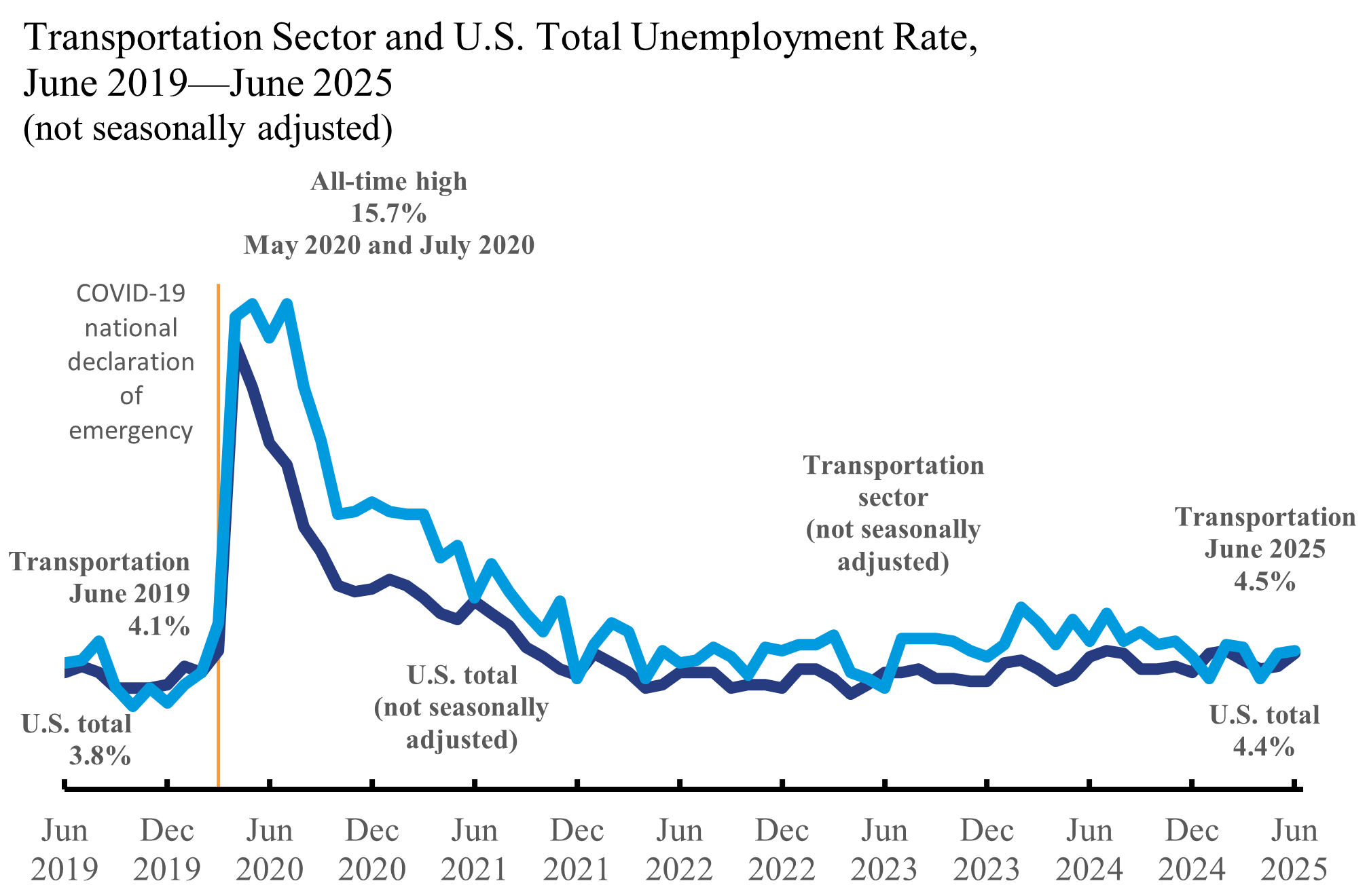

The foundation of U.S. economic stability and the primary bulwark against recession remains its surprisingly tight and durable labor market. While some leading indicators point to a gradual cooling, core metrics continue to defy recessionary signals, providing a crucial buffer for household balance sheets and, by extension, consumer spending.

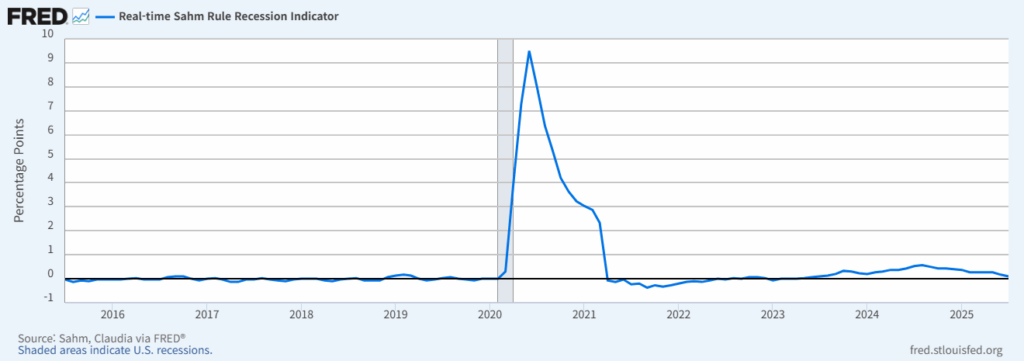

Data through mid-2025 shows that key labor market stress indicators are well within healthy territory. Weekly initial jobless claims have remained low, and the “Sahm Rule,” a reliable real-time recession indicator that triggers when the three-month moving average of the unemployment rate rises by 0.50 percentage points or more relative to its low during the previous 12 months, has not been breached. This suggests that the labor market is normalizing from its overheated post-pandemic state rather than contracting sharply.

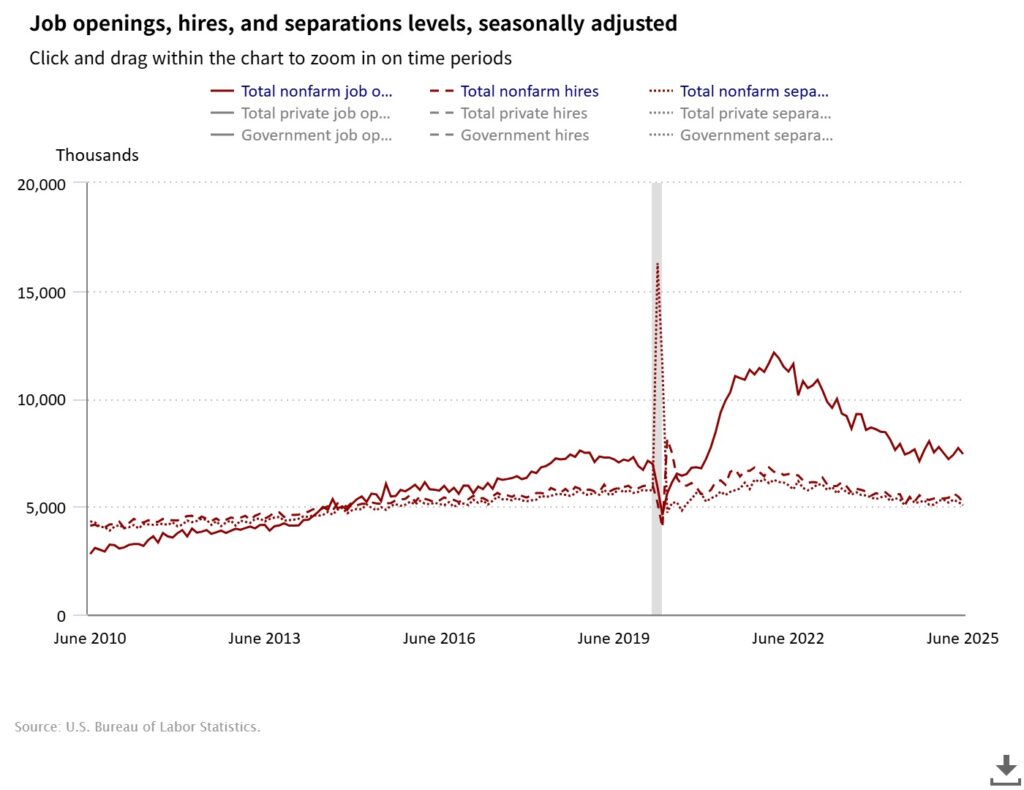

Beneath the headline numbers, the supply and demand dynamics confirm this narrative of a gradual rebalancing. Data from the Job Openings and Labor Turnover Survey (JOLTS) shows that the ratio of job openings to unemployed persons, while down from its peak, remains elevated by historical standards. Concurrently, layoff and discharge rates are low, indicating that companies are holding onto workers rather than shedding them in anticipation of a downturn. This structural tightness is being further influenced by evolving policy; the current administration’s stricter stance on immigration is acting as a constraint on labor supply, contributing to wage pressures in certain sectors and making it harder for the market to loosen significantly.

The direct consequence of this employment stability is the continued health of the American consumer. With jobs secure and wages growing, households have been able to service their debts. As a result, consumer credit delinquency rates, while ticking up from historic lows, remain contained and far from levels that would signal widespread distress. Furthermore, the “Misery Index”—the sum of the inflation and unemployment rates—has fallen from its 2022 peak to more manageable levels. This has prevented a severe, broad-based collapse in consumer confidence, allowing spending to continue powering the economy forward.

The AI Investment Supercycle

A powerful narrative has emerged questioning whether the current rally in technology stocks, centered on Artificial Intelligence, is a speculative bubble reminiscent of the dot-com era. Our analysis suggests this view is premature. The current boom is fundamentally different, as it is underpinned by a tangible, capital-intensive investment cycle in AI infrastructure that is already driving productivity and real economic output.

A comparison with the late 1990s is instructive. The dot-com bubble was characterized by soaring valuations for companies with little to no revenue or tangible production. In contrast, the current cycle exhibits a strong correlation between rising tech valuations, exemplified by firms like Nvidia, and a robust, measurable increase in real production within the high-tech industrial sector. This is not just a story about future promises; it is a story about current capital expenditure and output.

The financial firepower behind this cycle is immense. The “Magnificent Seven” technology giants are not merely valued highly; they are extraordinarily cash-rich. As of the end of 2023, their combined cash holdings exceeded $350 billion, a figure that has grown exponentially over the past decade. This massive war chest creates a self-sustaining cycle of research, development, and capital expenditure that is largely insulated from the tighter credit conditions affecting the rest of the economy. These companies can fund their ambitious expansion plans internally, ensuring the AI investment boom continues even as the Federal Reserve maintains a restrictive policy stance.

This investment is clearly visible in macroeconomic data. Orders for non-defense capital goods, a key proxy for business investment, have remained strong. While the explosive growth in manufacturing-related construction seen immediately after the pandemic has moderated, a new wave of investment is poised to begin. The immense energy demands of AI data centers will necessitate a significant build-out of the nation’s power generation and grid infrastructure, representing the next phase of this durable investment cycle. This suggests that the tech boom is not just a market phenomenon but a genuine driver of broad economic activity.

Containing the Tariff Shock

One of the most significant risks to the U.S. economy in 2025 was the inflationary impact of the administration’s broad-based tariff policy. Standard economic models predicted that these levies would be passed on directly to U.S. consumers, leading to higher prices, reduced purchasing power, and a potential stagflationary shock. Thus far, this risk has been surprisingly contained. The primary reason is that foreign producers and exporters, desperate to maintain their foothold in the lucrative U.S. market, have absorbed the majority of the cost.

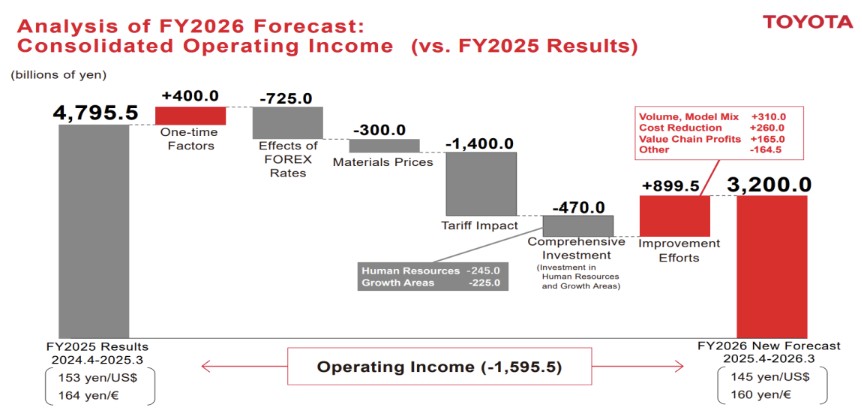

This dynamic is evident in corporate disclosures and pricing data. Analysis of earnings forecasts from major global exporters, such as Toyota, reveals a significant hit to projected operating income directly attributed to tariff impacts. These companies are choosing to sacrifice profit margins rather than risk losing market share. This is corroborated by U.S. pricing data; for example, average transaction prices for new vehicles in the U.S. have remained stable, and even declined in some segments, despite the imposition of tariffs on imported cars and parts. This absorption of costs by foreign firms has acted as a crucial, if temporary, shield for the U.S. consumer, preventing the full inflationary blow from landing.

The economy also appears to have successfully navigated the initial logistical disruption caused by the tariffs. In the months leading up to their implementation, there was a noticeable surge in imports as businesses front-loaded orders to build inventory ahead of the price hikes. This created a risk of a subsequent “inventory recession,” where a glut of goods would lead to a sharp drop in new orders. However, data on inventory-to-sales ratios across the manufacturing, wholesale, and retail sectors show that these levels have remained stable and well-balanced. This indicates that the economy has digested the initial shock without creating a major overhang, smoothing the path for more stable growth ahead.

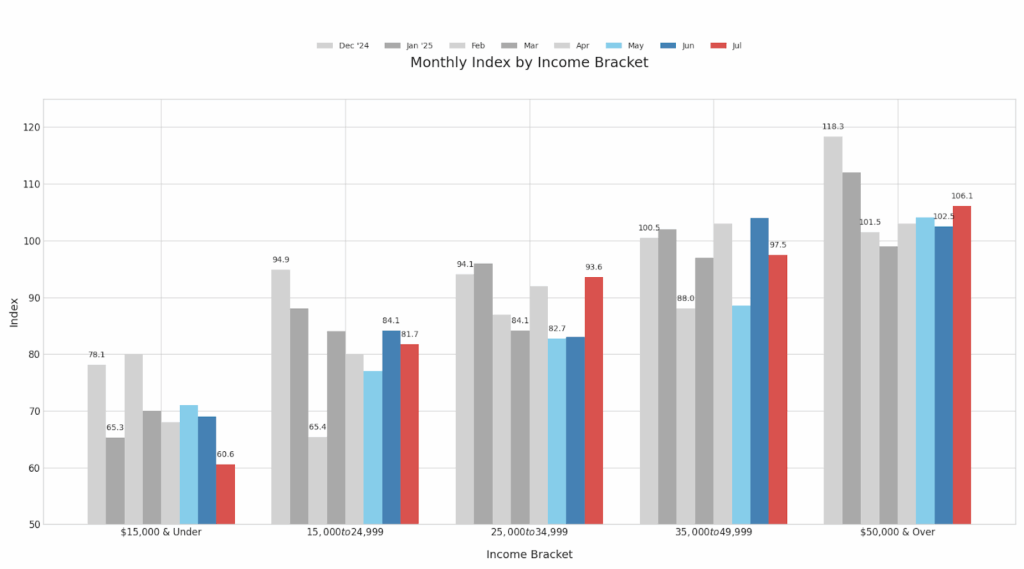

The resilience of the U.S. economy is not uniform; it is a story of divergence. A closer look at consumer data reveals a bifurcated reality. While aggregate spending remains robust, the underlying health of households differs starkly by income level. Consumer confidence among low-income households has been severely damaged by persistent inflation and the regressive nature of tariffs, which act as a consumption tax on essential goods. In stark contrast, confidence among high-income households, after a dip during the tariff negotiations, has rebounded sharply.

This divergence is the key to understanding the economy’s paradoxical strength. The bulk of discretionary spending in the United States is driven by the upper-middle and high-income brackets. This demographic is benefiting disproportionately from strong asset markets—namely, equities and real estate—and is far less sensitive to price increases on everyday goods. As long as stock portfolios remain elevated and high-end employment is stable, aggregate consumption can continue to grow even as a significant portion of the population faces acute financial strain. This creates a fragile but currently functional economic dynamic, where the strength of the top 40% of consumers is sufficient to keep the entire economy out of recession.

https://www.bls.gov/jlt

https://mgiedit.org/a-cautious-outlook-the-u-s-economy-in-2025-navigates-a-demand-slowdown/

답글 남기기