AI Bubble vs. Dot-Com Bubble: A Data-Driven 2025 Market Analysis – The atmosphere on Wall Street is electric, charged with a familiar blend of groundbreaking innovation, soaring ambition, and the dizzying climb of technology stocks. The artificial intelligence (AI) revolution is in full force, creating fortunes and redefining entire industries. Yet, with each new peak, the ghost of markets past poses a critical question: Is history repeating itself? Are we on the precipice of a dot-com-style collapse that could erase trillions in value?

While the term “AI bubble” is gaining traction, a granular comparison to the conditions of late 1999 and early 2000 reveals that today’s market stands on a fundamentally more stable foundation. This deep dive will explore the parallels, the crucial differences, and the key indicators that will define the path forward in this transformative era.

Investment Surge: A Parallel with a Critical Difference

The most obvious similarity between the two eras is the engine of growth: a massive wave of private sector investment. Today, capital is flooding into AI hardware, software, and R&D at a scale that actually surpasses the dot-com peak. In Q2 2025, this investment reached 7.16% of U.S. nominal GDP, higher than the 6.25% seen in Q1 2000.

However, the context of this spending is paramount. Technology’s economic footprint has grown consistently for over 70 years, from 1% of GDP in the 1950s to over 7% today. Crucially, today’s 7.16% investment level lies almost perfectly on its long-term historical trend line. In contrast, the spending in 1999 represented a sharp, unsustainable spike above its historical trend, signaling speculative overheating. Today’s investment appears less like a speculative frenzy and more like a sustained, structural shift in the economy.

Beyond the Averages: A Deeper Look at Market Valuations

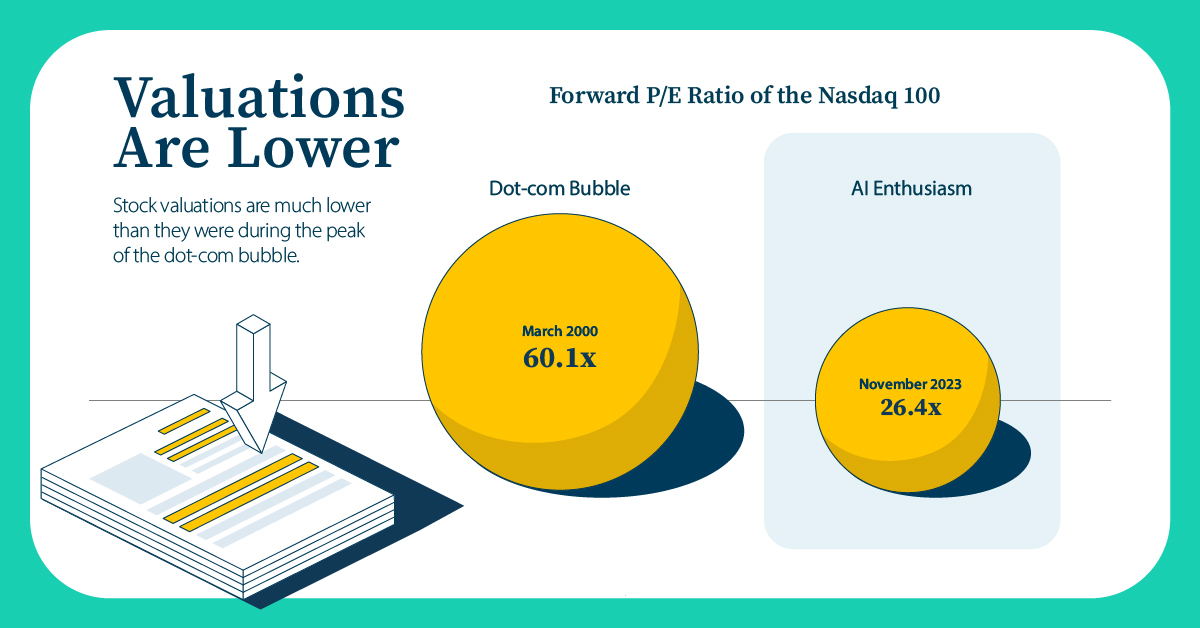

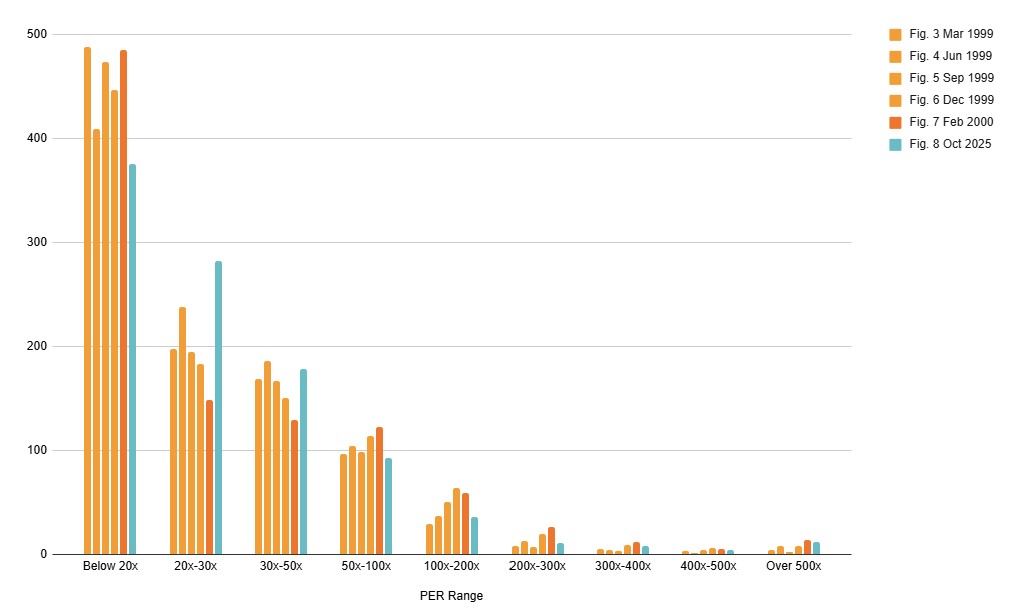

On the surface, valuations also look alarming. The average Price-to-Earnings (PER) ratio for the top 1,000 U.S. companies recently hit 27.1x, exceeding the 26.2x seen just before the 2000 crash.

But this is a classic “trap of the average”. The health of a market lies not in its average valuation, but in the distribution of those valuations. The telltale sign of a late-stage bubble is extreme market polarization: investors assign irrational multiples to “growth” stories while aggressively selling off everything else, hollowing out the sensible middle ground.

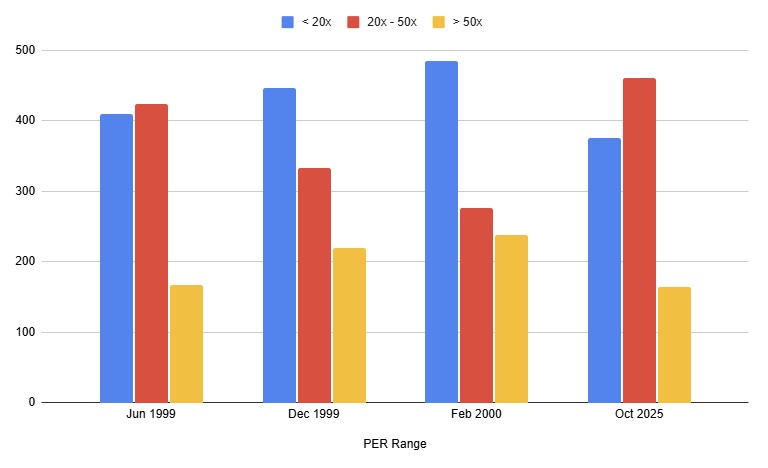

This is exactly what happened in 1999. From Q2 1999, the proportion of reasonably valued stocks (defined as having a 20x-50x PER) began to shrink rapidly as investors chased high-fliers. It was at this exact point that the Nasdaq began its final, vertical ascent.

Today, the situation is reversed. A healthy 46% of companies reside in that 20x-50x PER range, a figure higher even than the 42% seen in mid-1999, before the real mania began. This suggests that while enthusiasm is high, a broad-based discipline on valuations remains intact.

The Fed Factor: Why 2025’s Monetary Policy Is a Game-Changer

Perhaps the most significant differentiator is the macroeconomic climate. The dot-com bubble was ultimately burst by the Federal Reserve’s interest rate hikes, which increased the cost of capital and choked off investment.

Today’s environment is the polar opposite. The market is anticipating multiple interest rate cuts over the next year. With tight credit spreads and a favorable financing environment, companies have the fuel to continue executing their long-term AI strategies. As long as this supportive monetary policy remains, a key catalyst for the 2000 crash is absent.

The Path Forward: A Neutral Outlook for the AI-Driven Market

While the data suggests we are not at a 1999-style peak, the future is never certain. A neutral, forward-looking analysis requires weighing the bull case against potential headwinds.

The Bull Case: A Productivity Revolution

The optimistic scenario is that we are in the early innings of a multi-decade productivity boom driven by AI. In this view, current investments are rational and will lead to unprecedented efficiency gains across the economy. The market will continue to climb, albeit with periods of volatility, as these gains are realized and reflected in corporate earnings. Valuations, which seem high today, may be justified in retrospect.

The Bear Case: Potential Risks on the Horizon

However, several credible risks could derail the current trajectory:

- Sticky Inflation: If inflation proves more persistent than expected, it could force the Fed to reverse its course on rate cuts, reintroducing the very risk that ended the last tech bubble.

- Execution and Monetization Risk: The promise of AI is vast, but the path from potential to profit is not guaranteed. If companies struggle to effectively monetize their AI investments, investor sentiment could sour quickly.

- Regulatory Headwinds: Governments worldwide are grappling with how to regulate AI. Aggressive or poorly designed regulations could stifle innovation and create significant uncertainty for the industry.

- Geopolitical Shocks: Global instability remains a constant threat that could trigger a market-wide flight to safety, regardless of technological progress.

A More Likely Scenario: The “Rolling Correction”

Rather than a single, market-wide crash, a more probable future involves a series of “rolling corrections.” Specific sub-sectors within the AI ecosystem that become over-hyped (e.g., a particular type of AI chipmaker or a niche software vertical) may experience sharp, painful downturns. However, the broader AI trend will persist, with capital rotating from overvalued areas to more promising ones. This creates a volatile but ultimately upward-trending market, punishing speculation while rewarding a focus on fundamental value.

The Final Verdict: Learn from History, Don’t Be Ruled by It

The current AI boom is not a simple echo of 1999. It is powered by a more mature, better-capitalized industry and supported by a favorable macroeconomic backdrop. The structure of market valuations, a key internal indicator, shows a degree of health and balance that was absent at the peak of the dot-com mania.

The prudent path forward is one of cautious optimism. Investors should maintain exposure to this generational technological shift but remain vigilant. The key is to monitor the signals: a rapid polarization of valuations, a sudden reversal in monetary policy, or a failure to translate AI hype into tangible profits would all be signs that the climate is changing.

The ghost of 1999 is a valuable teacher of how bubbles end, but it is not a prophet that can predict when the next one will begin. Today’s market is writing its own unique story.

https://www.derekthompson.org/p/why-ai-is-not-a-bubble

https://mgiedit.org/a-cautious-outlook-the-u-s-economy-in-2025-navigates-a-demand-slowdown/

답글 남기기