Navigating the Shifting Sands of East Asian Consumption: A Deep Dive into China and Japan’s Gen Z – The global economic landscape is in a state of flux. As traditional growth engines face headwinds and trade dynamics evolve, the focus is increasingly shifting towards domestic consumption as a driver of economic stability and expansion. In East Asia, two economic powerhouses, China and Japan, are actively pursuing strategies to bolster internal demand, and a critical demographic in this push is the younger generation – Generation Z. This report, drawing insights from recent economic analysis, delves into the evolving consumption trends of Gen Z in these nations, exploring their commonalities, divergences, and the potential implications for regional economies and international trade.

The macroeconomic environments of China and Japan present a fascinating contrast. China, grappling with the risk of deflation, is implementing policies aimed at stimulating domestic spending to counteract external pressures such as reduced import demand from the United States following strengthened tariff measures. Japan, on the other hand, is navigating an environment of increasing inflation after decades of battling deflation, with efforts focused on creating a virtuous cycle of rising wages and prices. Despite these differing backdrops, both nations recognize the potential for significant policy impact on their younger populations, who tend to have less accumulated wealth and income and are thus more responsive to changes in economic conditions and policy support.

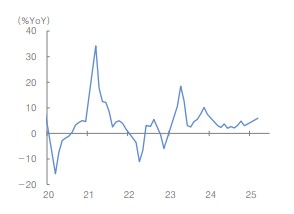

Recent data suggests promising signs of domestic demand recovery in both countries. China’s retail sales showed a surprise increase in the first quarter, indicating a potential bottoming out of domestic demand. While headline CPI has fallen due to lower energy prices, core CPI has continued to rise, further signaling an improvement in internal consumption. In Japan, despite considerable inflationary pressure, real household expenditure has begun to increase again, indicating a gradual recovery in domestic spending.

Both governments are actively implementing measures to encourage this trend. China is prioritizing domestic expansion, with monetary policy easing aimed at stabilizing the stock and real estate markets. The People’s Bank of China (PBOC) announced a financial support package, including cuts to the reserve requirement ratio and reverse repo rates, along with reductions in provident fund loan rates and interest rates for first-time homebuyers. Structural monetary policy tools are also being utilized to support areas such as technology, capital market stabilization, small and medium-sized enterprises (SMEs), service consumption, pensions, and trade.

Notably, subsidies for replacing old consumer goods with new ones have been doubled this year, with consideration being given to expanding their use to services like travel. Efforts to boost the technology sector and ease regulations on platform companies are also expected to improve labor demand and enhance the purchasing power of young people, particularly when combined with increased liquidity and lower housing loan rates. These policies underscore China’s commitment to shifting towards a growth model driven by internal consumption.

Japan, in its bid to escape decades of deflation, continues to pursue a strategy centered on a positive feedback loop between prices and wages. Following significant wage hikes last year, this year’s “Shunto” (spring labor negotiations) are targeting similar increases, with large companies already agreeing to raises exceeding 5.4%. This trend is expected to extend to SMEs, and efforts are underway to improve conditions for non-regular workers as well. Addressing labor shortages, particularly in entry-level positions, is also contributing to rising starting salaries.

Furthermore, the government has raised the tax-exempt threshold for earned income, addressing the long-standing “1.03 million yen wall” that discouraged part-time workers from increasing their hours due to the imposition of resident and income taxes. These measures are expected to boost the consumption capacity of low-income households and encourage greater labor participation. The combination of rising wages and government efforts to stimulate personal consumption is likely to lead to a more significant increase in spending among the younger generation, who demonstrate a higher propensity to consume compared to older demographics.

The Rise of Experience Consumption: A Shared Priority

A striking commonality in the consumption patterns of Chinese and Japanese Gen Z is the prioritization of “experience consumption”. This trend, which accelerated globally after the COVID-19 pandemic, sees young people in both countries valuing experiences over material goods, even in the face of limited consumer power.

In China, this manifests as a growing emphasis on lifestyle, health, and wellness. The “Outdoor Plus” trend, which blends daily life with outdoor sports, exemplifies this shift. Surveys indicate a high prioritization of wellness among Chinese consumers, exceeding levels seen in the United States and the United Kingdom. This focus is reflected in the growth of the health food market, with a significant portion of consumers being under 40, and a rising preference for low-alcohol beverages and low-calorie or additive-free foods.

The preference for experiences is also transforming the tourism landscape. As Chinese outbound tourism is expected to recover to pre-pandemic levels, the lifestyle-focused trend is likely to accelerate this recovery. Despite persistent youth unemployment impacting spending power, travel remains a high priority for young Chinese consumers.

This is evident in the changing demographics of Chinese tourists visiting South Korea, with a noticeable increase in the proportion of those in their 20s and 30s and a decrease in the average age. The purpose of travel is also shifting away from shopping, which has declined in importance, towards food and gourmet tourism. While overall tourism expenditure has increased, spending on shopping has decreased, while spending on accommodation, food, transportation, medical treatment, and cultural services/entertainment has risen significantly. This suggests a move towards longer stays and a greater focus on immersive experiences rather than purely transactional retail therapy.

In Japan, “Oshikatsu” (推し活) culture stands out as a prominent example of experience consumption. This activity involves actively supporting and promoting a favorite person (like an idol), character, or even an object. Oshikatsu extends beyond online engagement to include offline gatherings and events.

The market for Oshikatsu is substantial, with the majority of consumers being in their teens, twenties, and thirties. Significant monthly expenditures are reported by a large percentage of participants. The economic impact of Oshikatsu among Gen Z has even been noted by the Bank of Japan, with strong demand for related goods like trading cards and character merchandise despite price increases. This trend also fuels service consumption, with dedicated establishments like “Oshikatsu bars” offering spaces for fans to enjoy content and connect.

Diverging Paths: Price Perception and Value

While experience consumption is a shared passion, the approach to price and value differs between Chinese and Japanese Gen Z, reflecting their distinct macroeconomic environments.

Chinese Gen Z, influenced by the risk of deflation and a challenging job market characterized by high youth unemployment, exhibits a strong preference for ” Gasungbi(가성비)” or value for money, embodied by the “Pingti” (平替) trend. Pingti, similar to the concept of “dupes” or affordable alternatives, involves choosing high-quality, low-cost substitutes for expensive brands. This trend goes beyond simple imitation, emphasizing that the alternative may share the same manufacturers or materials as the premium product, effectively removing the “brand premium” from the price.

The popularity of Pingti is evident in the massive increase in related online content and interactions. Examples span various sectors, from coffee chains strategically opening near competitors and offering similar popular items at lower prices to fast-food alternatives targeting lower-tier cities and surpassing the store counts of established global brands. The trend is also prominent in cosmetics and apparel, with Chinese brands offering products comparable in quality to international luxury brands but at significantly lower price points.

In contrast, Japanese Gen Z’s approach to value, while still seeking cost-effectiveness, is more aligned with ” Gasimbi,” focusing on emotional satisfaction and prioritizing spending on items or experiences that are personally significant, a concept related to “Merihari” (メリハリ), which involves balancing overall spending by splurging on meaningful purchases. The “Generic ㅇㅇ” trend in Japan, while also referring to affordable alternatives, emphasizes the ability to discern and find good quality products at low prices rather than simply seeking low-cost replicas of luxury goods.

This reflects a generation more accustomed to inflation and therefore more willing to pay a certain price for quality, prioritizing a satisfying purchase over simply maximizing savings. This trend is observed in cosmetics, where affordable alternatives to high-end brands are popular, and in household goods, with budget-friendly stores offering products comparable to those from popular mid-range brands. Even in the food sector, “generic” recipes for popular restaurant dishes gain significant traction. The preference for value in Japan is also contributing to the success of South Korean cosmetic brands, which are favored for their good quality and affordability.

Implications for Regional Trade and the Future

The consumption trends of Chinese and Japanese Gen Z have significant implications for regional trade, particularly for countries like South Korea. While the growth rate of South Korean consumer goods exports to the United States has slowed, exports to non-US destinations are increasing. The expanding consumption of Chinese and Japanese youth, driven by both experience seeking and evolving value perceptions, presents opportunities for South Korean consumer goods and services.

South Korea’s competitive edge in areas like cosmetics, known for their quality and value, and in the production of character and idol merchandise, positions it well to benefit from the spending habits of Gen Z in both countries. Recent data shows robust growth in exports of agricultural and fishery products and cosmetics, reflecting the global popularity of K-Food and K-Beauty trends. The increasing preference for experiences and the rising interest in Korean culture among Japanese youth, exemplified by the strong demand for K-pop in the Oshikatsu market, also bode well for South Korea’s tourism service balance.

Looking ahead, several futuristic predictions can be made based on these evolving trends:

- Personalization and Niche Experiences will Dominate: As Gen Z continues to prioritize experiences, the demand for highly personalized and niche offerings will surge. This could manifest in bespoke travel itineraries tailored to specific interests, exclusive fan events with limited attendance, or customized wellness programs integrating technology and individual preferences. Businesses that can effectively cater to these individualized desires will gain a significant edge.

- The Blurring Lines Between Physical and Digital Consumption: The digital fluency of Gen Z suggests a future where the lines between online and offline consumption will become increasingly blurred. Experiences may begin in the metaverse or through augmented reality, seamlessly transitioning to physical interactions. Retail spaces might transform into experiential hubs, offering more than just products but also immersive brand engagements.

- Sustainability and Ethical Consumption will Grow in Importance: While not explicitly detailed in the provided text, global trends indicate that Gen Z is increasingly concerned with sustainability and ethical practices. As their purchasing power grows, their demand for eco-friendly products, responsible sourcing, and socially conscious brands will likely influence consumption patterns in China and Japan. Businesses will need to integrate these values into their core operations and marketing strategies.

- Cross-Cultural Influence Through Experience Exports: The popularity of K-Culture in Japan highlights the potential for “experience exports.” We could see more countries leveraging their cultural assets – music, art, cuisine, and lifestyle – to attract young consumers seeking authentic and engaging experiences abroad. This could lead to new avenues for international trade and cultural exchange.

- Data-Driven Insights will be Crucial for Businesses: Understanding the complex and rapidly changing preferences of Gen Z will require sophisticated data analysis. Businesses will need to invest in tools and expertise to track, analyze, and predict consumer behavior, enabling them to tailor their offerings and marketing efforts effectively.

In conclusion, the younger generations in China and Japan are reshaping the consumption landscape. Their shared emphasis on experience, coupled with their distinct approaches to value and price, presents both challenges and opportunities for businesses and economies in the region and beyond. By understanding these trends and adapting their strategies accordingly, companies can tap into the significant potential of this dynamic demographic and contribute to the future growth of the East Asian economy.

The policies implemented by China and Japan to stimulate domestic demand, particularly those targeting youth, are likely to further amplify these trends, making the consumption patterns of Gen Z a critical area of focus for anyone looking to navigate the future of the global market.

https://www.globaltimes.cn/page/202412/1325689.shtml

https://mgiedit.org/the-trump-eras-economic-report-card-q1-2025-gdp/

답글 남기기